What are the changes to citizen audit for 2015/16? This year citizen audit changes. No longer are citizen audit rights covered by part II of the Audit Commission Act 1998 and the underlying regulations as this is no longer in force. For this year (2015/16 financial year) such rights are covered by part 5 … Continue reading “What are the changes to citizen audit for 2015/16?”

What are the changes to citizen audit for 2015/16?

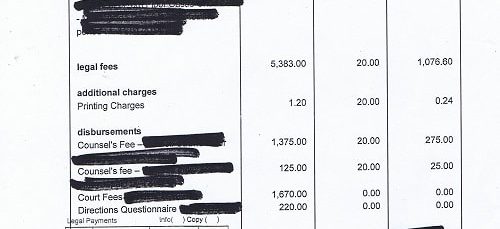

An example of an invoice supplied by Wirral Council during a previous audit

This year citizen audit changes. No longer are citizen audit rights covered by part II of the Audit Commission Act 1998 and the underlying regulations as this is no longer in force.

Previously during citizen audit, public bodies could redact information about the names of their own staff, but if it was information about anyone else they had to get their auditor’s approval.

Now, public bodies can redact parts of documents or whole documents on grounds of commercial confidentiality (although a public interest test has to be carried out) and information about the names of their own staff. They are also allowed to redact information that is the name of other individuals but not if it’s the name of a sole trader.

Previously the auditor had to consider all objections (as long as a copy was sent to the public body) made by local government electors for a declaration that an item of account is unlawful, recovery of an amount not accounted, a public interest report or an immediate report.

Now, an objection can only be about a matter that the auditor could write a public interest report about or declare that an item of account is unlawful but the auditor can decide not to consider the objection if:

(a) the auditor thinks it is frivolous or vexatious, or

(b) the cost to the auditor investigating is disproportionate to the sums involved or

(c) it repeats an objection already made and considered by the auditor whether in that financial year or a previous financial year.

However the auditor won’t be able to decide not to consider an objection if it is "an objection which the auditor thinks might disclose serious concerns about how the relevant authority is managed or led".

Even if the auditor rejects an objection for one or more of the reasons above the auditor can still make a recommendation to the public body.

Previously the Audit and Account Regulations 2011 required the inspection period was 20 working days regulation 9 and also that an advertisement was published (as well as a notice on its website) 14 days before this inspection period started regulation 10.

Under the new regime, this changes. There will be a longer inspection period of thirty working days, but this period will now also be the time during which objections and questions to the auditor must be made.

£110,000 Community Fund grants scheme now open for expressions of interest from groups for waste prevention, reuse, recycling or carbon benefits projects in Merseyside and/or Halton

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

Merseyside Recycling and Waste Authority public meeting of 5th February 2016 (where councillors agreed to continue the Community Fund for 2016/17)

Merseyside Recycling and Waste Authority 5th February 2016 agenda item 11 Community Fund 2016 17 L to R Unknown, Mandy Valentine (Assistant Director of Governance and Performance), Cllr Graham Morgan (Chair), Carl Beer (Chief Executive) and Peter Williams (Director of Finance)

The author of this piece declares an interest as a customer of his business is employed by one of the Wirral organisations that received a grant from Merseyside Recycling and Waste Authority in 2014/15 mentioned below.

Last Friday afternoon councillors on the Merseyside Recycling and Waste Authority agreed to continue the Community Fund for 2016/17 with an allocation of £110,000.

£57,000 has been set aside for regional (Merseyside and Halton) projects with a maximum award of £25,000 per a project in this category.

£48,000 has been set aside for district level projects (districts are Wirral, Liverpool, Sefton, St. Helens, Knowsley and Halton) with a maximum grant award of £8,000 per a project in this category.

Any unspent monies at the regional level will be reallocated to projects at a district level.

Tomorrow’s Women Wirral received £10,000 for their Inspiration Hall project. Community Action Wirral received £19,982 for their Donate and Create Change project. Wirral Change received £9,064 for their Too Good To Waste project.

This year the Community Fund is open again for applications from registered charities, not-for-profit organisations (including social enterprises), community, neighbourhood or voluntary groups, faith groups delivering community work, schools, colleges or universities.

It is a two stage grant application process with the first stage being an expressions of interest stage.

Applications are sought for projects that can deliver waste prevention, reuse, recycling and carbon benefits.

A farce at Wirral Council’s public question time (Act 2, Scene 1) Is Wirral Council “open and transparent”?

A farce at Wirral Council’s public question time (Act 2, Scene 1) Is Wirral Council “open and transparent”?

A question on councillors expenses to Cllr Adrian Jones Wirral Council 14th December 2015

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

Wirral Council’s Public Question Time 14th December 2015

Before I write about the question I asked of Councillor Adrian Jones at public question time, I am going to explain some of the legal background, what’s happened so far and why there are echoes of the extreme lengths that the former Speaker of the House of Commons Michael Martin went to over MPs’ expenses.

There are a number of different laws (and a bit of history) here that apply to this, so I am going to start by explaining my understanding of them and explain why Cllr Adrian Jones has unfortunately fallen into the trap of believing things officers tell him and also getting bamboozled by some of the legal jargon. Here is a link to a transcript of a previous answer he gave.

I’m a local government elector here on the Wirral (basically that means I get to vote in elections to Wirral Council).

Each year, during the audit there is a period of about three weeks when local government electors have a legal right to inspect and receive free copies of accounts to be audited and copies of all books, deeds, contracts, bills, vouchers and receipts relating to them.

Wirral Council can remove any details of employees, but has to seek the external auditor’s permission (in this case Grant Thornton) to remove anything else.

Once the inspection period ends, there is then a period when questions can be asked of the auditor followed by a period when formal objections can be raised or requests for a public interest report.

In case Wirral Council thinks I’m picking on it, this year I made requests to Merseytravel (part of the Liverpool City Region Combined Authority), Merseyside Waste Disposal Authority (also called Merseyside Recycling and Waste Authority), Merseyside Fire and Rescue Authority and Liverpool City Council.

Each of those other bodies managed to respond and provide the information for inspection more or less within the inspection period.

Two of these authorities (Merseyside Fire and Rescue Authority and Merseyside Waste Disposal Authority) provided some of what I requested in electronic format.

Wirral Council however decided that providing me with what I’d estimate at 10% of what I asked for was reasonable. It’s not!

These other public bodies I refer to are much smaller (in terms of staff and budget) than Wirral Council, yet by being flexible saved to give the example as outlined above the internal costs of copying a contract of over 11,000 pages in length. Had I requested such a contract from Wirral Council I would still be waiting as they would insist on supplying it in paper format!

In addition to this I requested various invoices and to inspect the councillors’ expenses (I haven’t seen any of the latter and received about one in ten of the former).

By reversing this decision Wirral Council saved ’thousands in the costs of perhaps adding an extra hour to the next Highways and Traffic Representation Panel public meeting, the cost of it then going on the agenda of the next Regeneration and Environment Policy and Performance Committee public meeting and the cost of a Cabinet Member finally making a decision (along with the associated costs of officers trying to persuade objectors to drop their objections).

I might point out that as I put this information in the public domain had Cabinet reversed their decision at an earlier stage the costs of consultation on the proposed traffic regulation order (an expensive public notice in the local newspaper etc) would have been saved too.

I would suspect that councillors’ use of taxis would be broadly comparable from year to year. So let’s test Cllr Adrian Jones’ assertion.

In response to this FOI request the taxi bill in 13/14 was ~£3k and Cllr Adrian Jones confirmed in answer to my question that for the 14/15 financial year the total cost was roughly the same.

Here are three councillors that got taxis in 13/14 and the costs:

Cllr Moira McLaughlin £755.30 Cllr Pat Hackett £700 Cllr Steve Niblock £493.90

Had anyone of those stopped getting taxis at Wirral Council’s expense the total amount for 14/15 would’ve dropped dramatically.

Yet here are the relevant amounts from the 2014/15 published list:

Cllr Moira McLaughlin £NIL Cllr Pat Hackett £NIL Cllr Steve Niblock £NIL

If these three councillors had all decided to give up getting taxis and the £NIL amounts were correct (the latter point Cllr Adrian Jones states in answer to my question) then the total amount would drop by ~£2k (the combined total of all three). However it hasn’t!

You can see the full exchange between myself and Cllr Adrian Jones below.

Cllr Ron Abbey (who is a member of Wirral Council’s Audit and Risk Management Committee) makes the point before Cllr Adrian Jones that it is implied that this is unlawful and isn’t that terrible to imply such a thing?

Clearly as clearly outlined above, had Wirral Council not flouted a number of its other legal responsibilities I would be able to answer that question and Wirral Council’s cultural attitudes towards its legal responsibilities continue to have the effect of interfering with the freedom of the press and triggering the Streisand effect.

Councillor Adrian Jones makes the point that councillors are trusted not to misuse the public purse paying for their taxis.

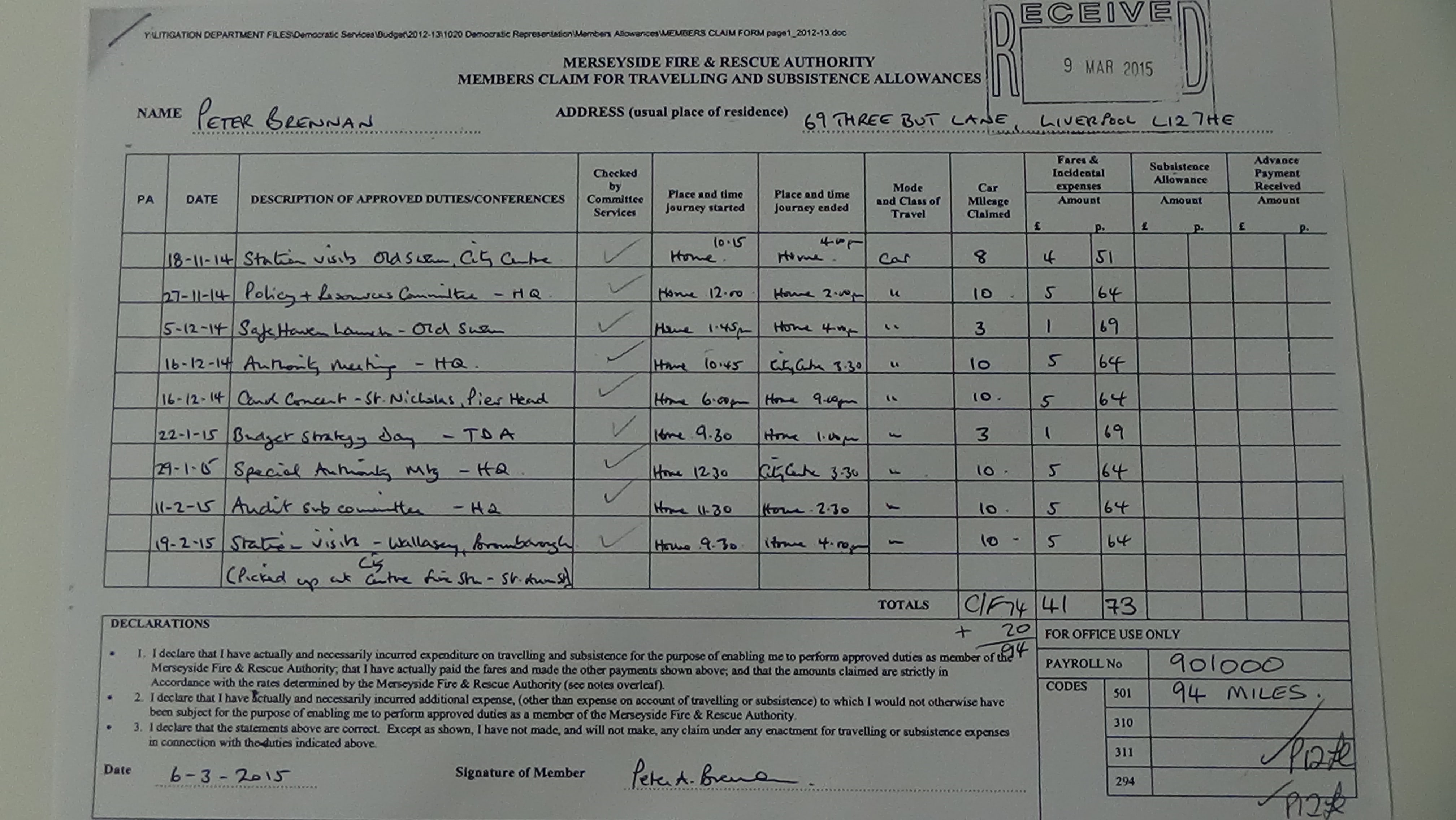

Below is a claim form (as I’m being seasonal) from one of Cllr Adrian Jones’ party colleagues, a Councillor Peter Brennan (a councillor at Liverpool City Council) who claimed from Merseyside Fire and Rescue Authority (and was paid for) £5.64 for car mileage expenses to and from a carol concert at St Nicholas’ Church. In the grand scheme of things you may point out that £5.64 doesn’t matter and at least he didn’t get a taxi! However it’s the cumulative cost to the public purse of these matters and the excessive secrecy at Wirral Council that is leading to suspicion as to why despite Cllr Adrian Jones’ claims about openness and transparency that at Wirral Council they are being anything but on this politically sensitive topic!

Cllr Peter Brennan car mileage claim November 2014 to February 2015 page 1 of 2 thumbnail

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

What was in the “strictly confidential” report on Merseyside Recycling and Waste Authority that cost over £14000?

What was in the “strictly confidential” report on Merseyside Recycling and Waste Authority that cost over £14,000?

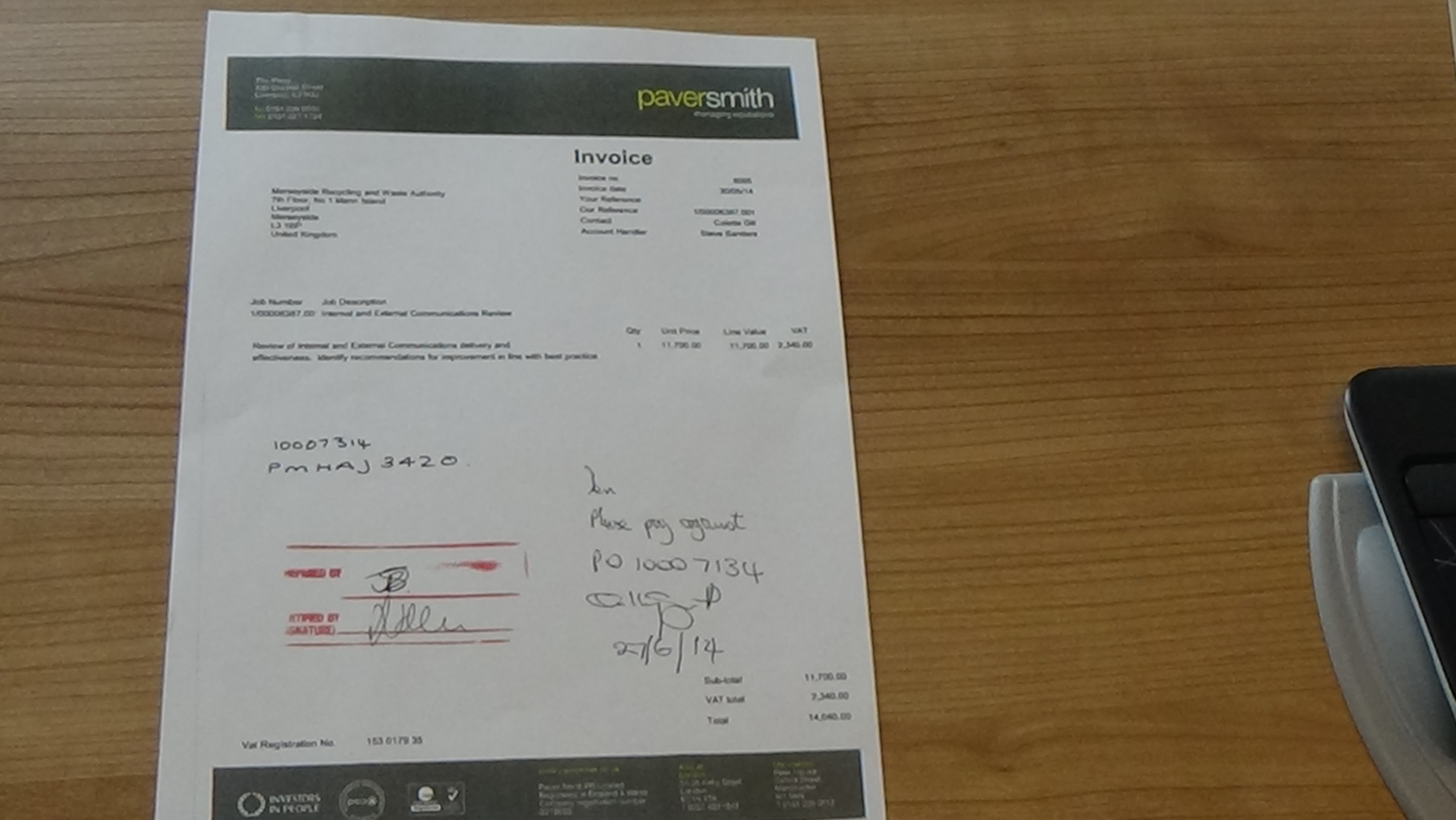

Last year Merseyside Waste and Recycling Authority paid Paver Smith (a PR agency which has since changed its name to Influential) £11,700 + VAT for 18 days work (at a rate of £650 + VAT) for an internal and external communications review. You can see the invoice for that work below.

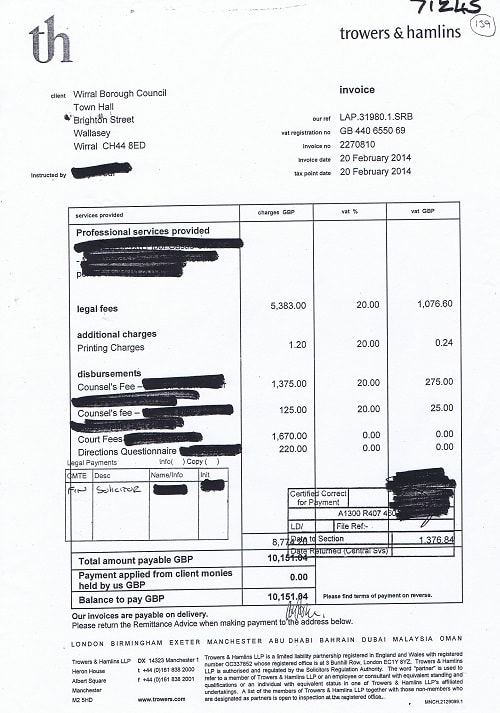

Merseyside Recycling and Waste Authority invoice Paver Smith

The internal communication review involved ‘discovery’ sessions with MRWA staff, an online questionnaire and focus groups. Below is the internal communications bit of the report (with my comments under each page).

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 1

This is just the cover page for the report.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 2

This report is “strictly confidential”. Why do I know this? Why I know because this page tells me so in red letters.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 3

This is a contents page.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 4

A whole page on “introductory remarks” that contains a lot of phrases such as:

“employees and management must communicate in order for an organisation to function effectively”, “there is real value in staff being clear on and understanding the forward mission and objectives of MWRA” and “Staff also carry an organisation’s brand out to the market, with clients, stakeholders and the public. Having them “on message” and carrying a unified and coordinated message can have great benefits”.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 5

This page deals with “Objectives and methodology” including this section on confidentiality:

It is crucial to the process on an internal communications review that all feedback is supplied in strictest confidence and handled with great care.

For the results to be helpful for an organisation feedback needs to be given openly and without concern.

Therefore all focus group interviews were undertaken in the strictest confidence under Chatham House rules with no attributing of specific statements to individuals.

The internal survey was structured also in a way to preserve anonymity.

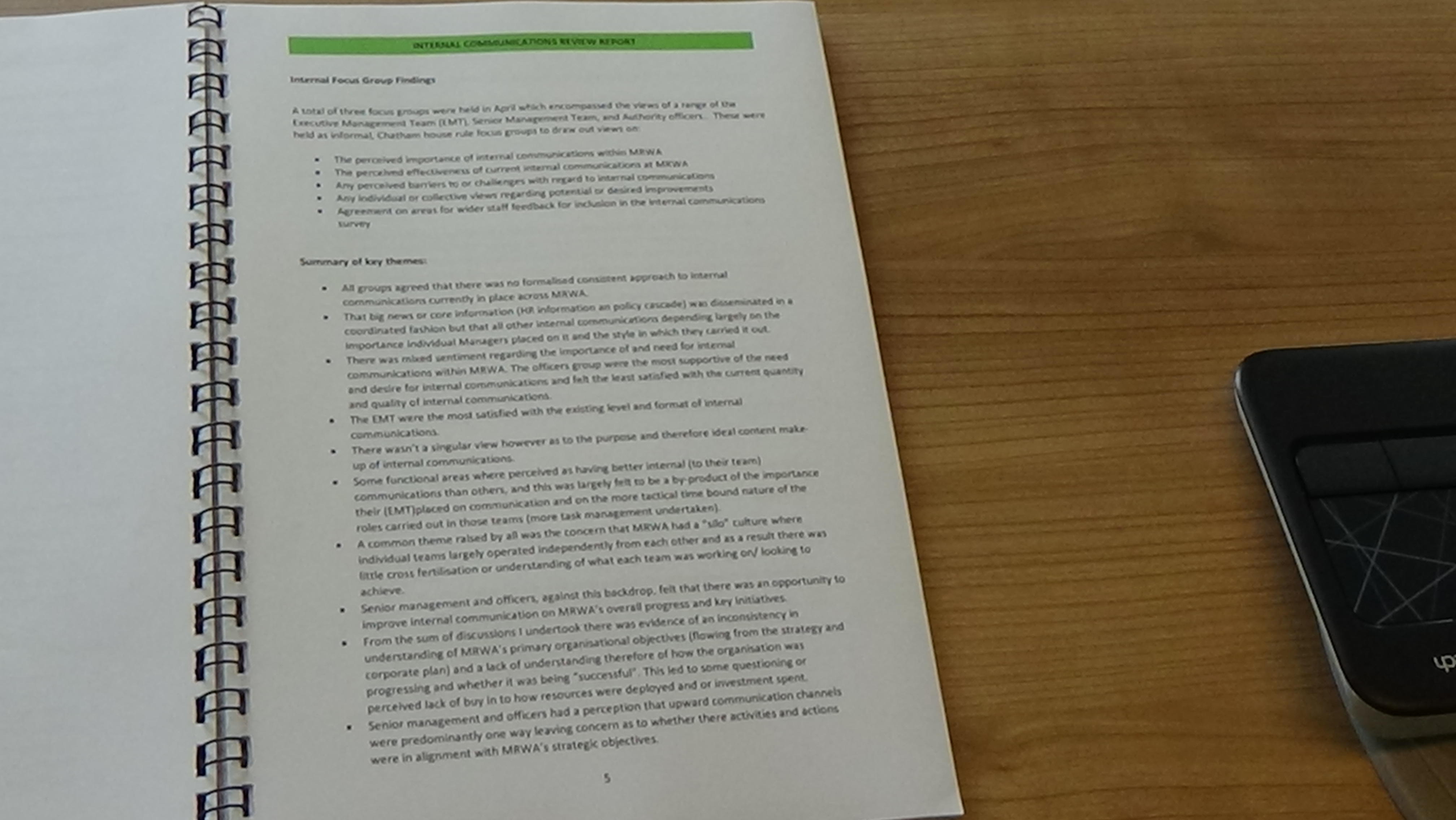

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 6

This next page goes into detail about the three focus groups (Executive Management Team, Senior Management Team and Authority officers).

One of the more interesting comments on this page is “A common theme raised by all was the concern that MRWA had a “silo” culture where individual teams largely operated independently from each other and as a result there was little cross fertilisation or understanding what each team was working on/ looking to achieve.”

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 7

This page has the rather telling comment at the top (EMT stands for Executive Management Team) “There was a staff perception that the EMT didn’t wish to engage in two way communication and discussion.” followed by “All expressed a concern that the intranet was used passively to disseminate information that staff were then assumed to seek out, but that active use of the intranet was however very low.”

Then it moves on to themes from the Executive Management Team focus group. Here are some quotes from that focus group:

“Concern was express that some of the staff had unrealistic expectations as to what they should be communicated to about.”

and

“The intranet was raised as a tool that wasn’t effective and not proactively used to access information.”

The senior management focus group also commented on the intranet and the silo culture.

“It was felt by some that too much reliance was placed on people proactively seeking out information on the intranet and that generally people didn’t do this. “

“A major concern for this group was what was described as a “silo” culture in MRWA with individual teams and functions working in isolation from each other and not enough interaction nor understanding of each other’s objectives, activity, challenges and successes. “

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 8

The staff focus group found internal communications was “poor”, apart from HR related matters. This focus group also felt “that generally the quality of management communication was poor and that there was a lack of interest (from the organisation) in seeking and listening to staff’s views and ideas.”.

Also commented on by the staff focus group was that this had led to a “‘what’s the point’ culture with some staff and a sense of negativity and scepticism”. The staff group expressed a “strong desire that the outcomes from the internal communications review should be shared”.

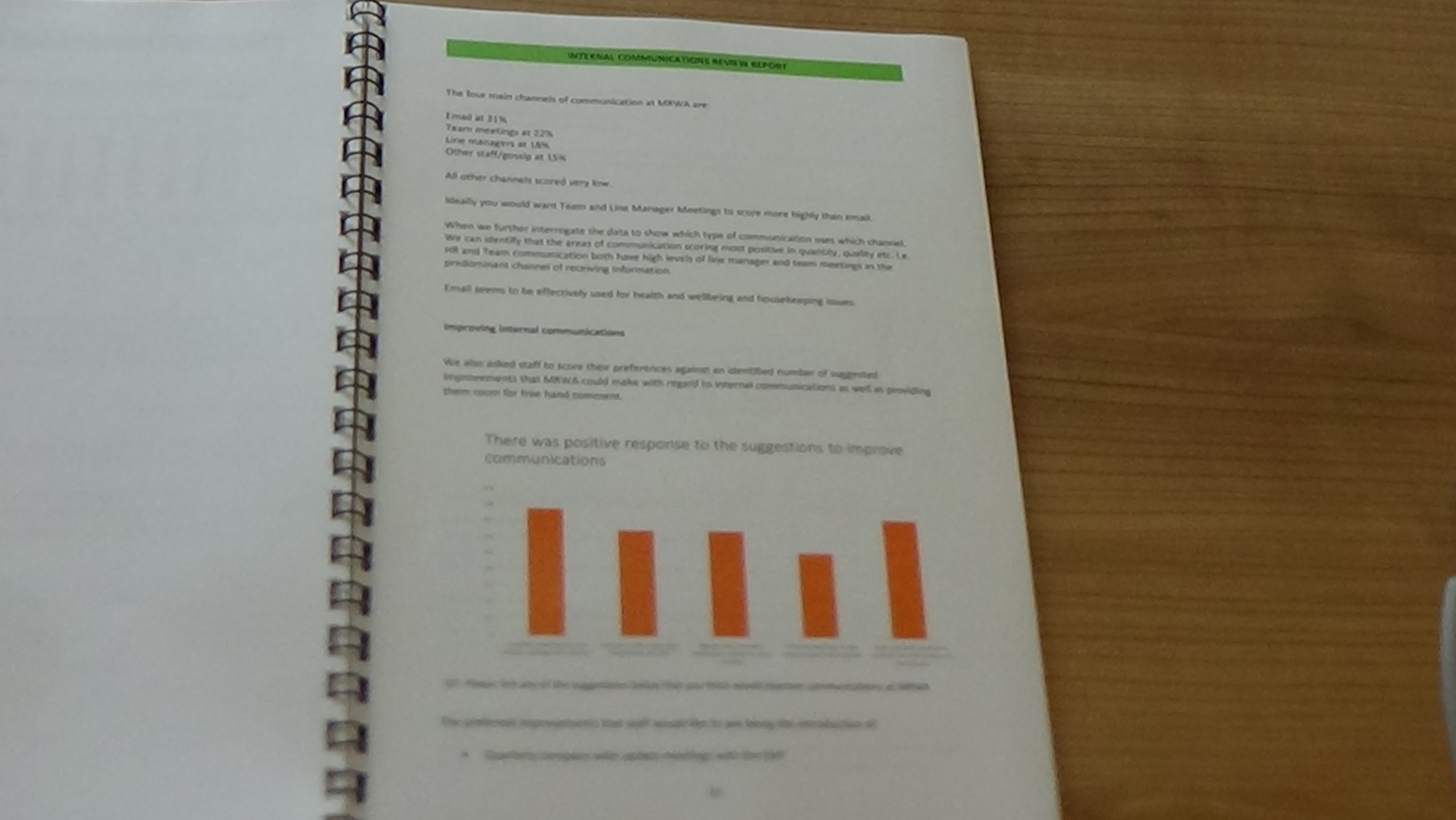

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 9

This page deals with the results of the questionnaire, there’s a pretty even split between people who think internal communications are poor and those that think it is satisfactory.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 10

This is another page going into the results of the survey and has the line “Good internal communications are seen generally by staff as of crucial importance to their sense of satisfaction and general wellbeing an an employee.”

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 11

This page details the results to the question “How important do you think internal communication is?”.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 12

This page is about the frequency of internal communications and information that people should receive monthly.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 13

This page is about the frequency of internal communications and information that people should receive quarterly or bi-annually.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 14

This page is about the quality of internal communication.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 15

This page is about satisfaction with the quality of internal communication and how it happens.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 16

This page deals with improving internal communications.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 17

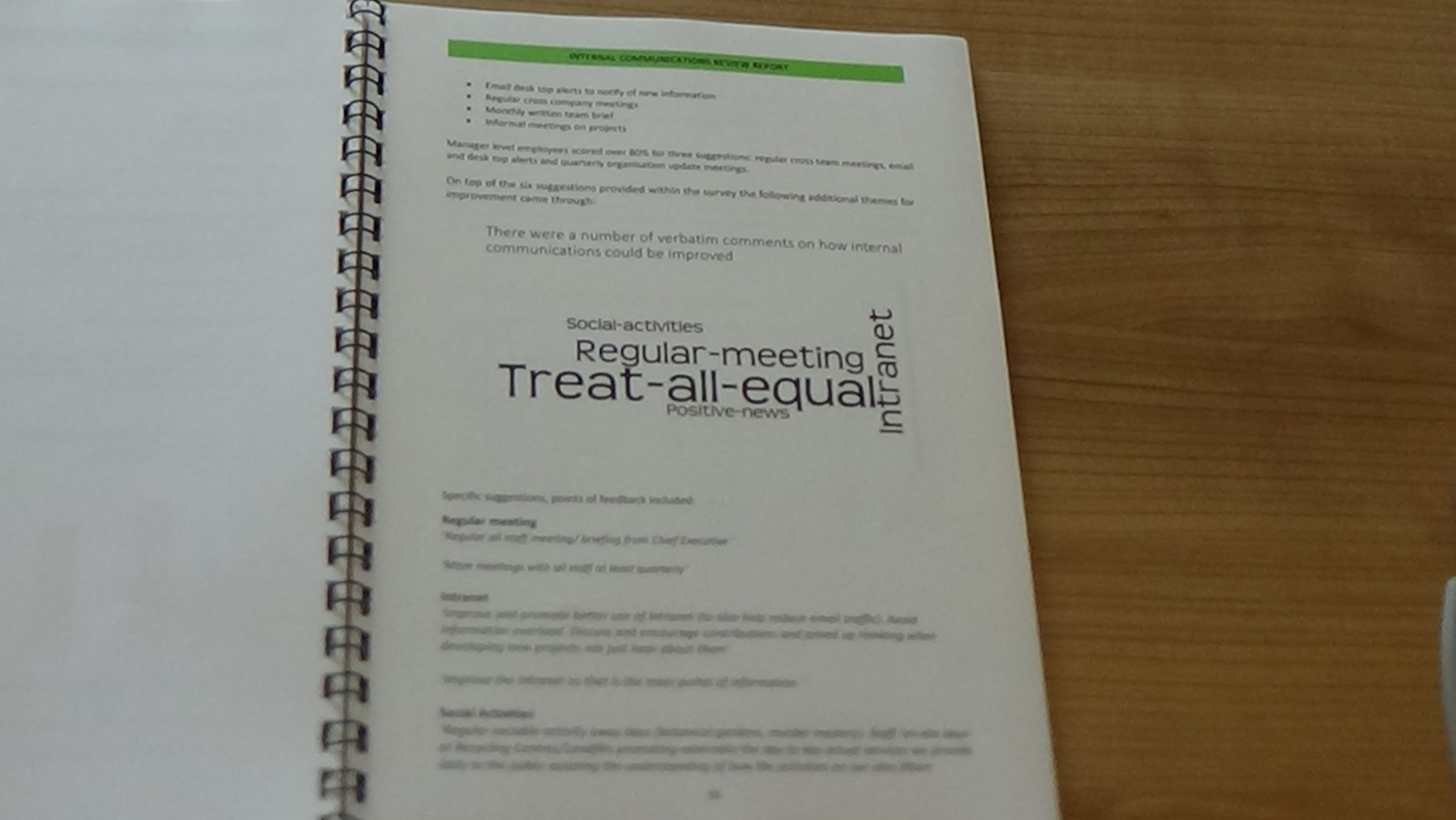

This page deals with verbatim comments on how to improve internal communications.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 18

This page states expands on the heading “treat all equal” which is clarified as meaning “Reduce the secret meetings and promote total inclusion”.

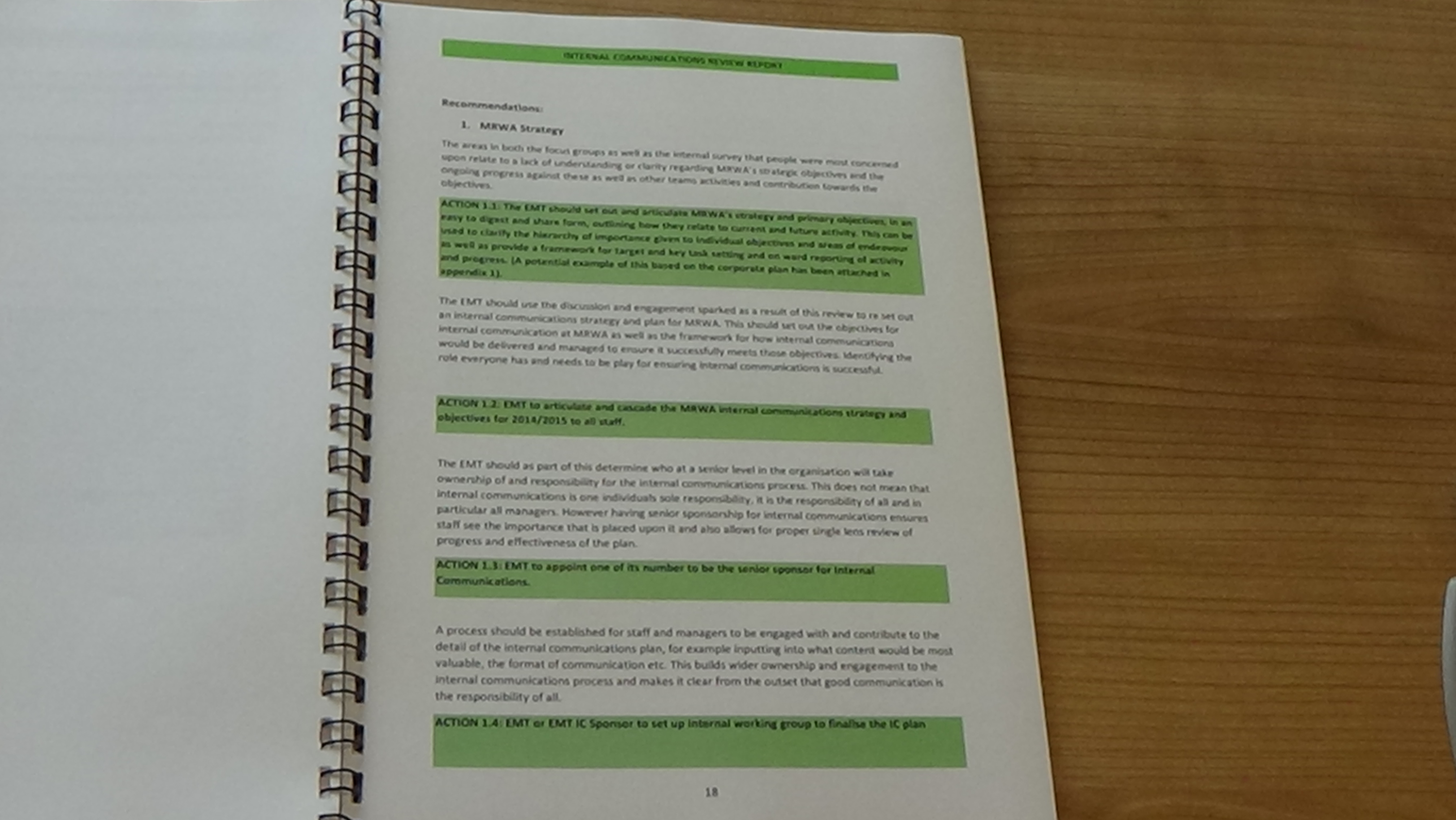

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 19

This page starts the recommendations, the first four are for the Executive Management Team (abbreviated to EMT).

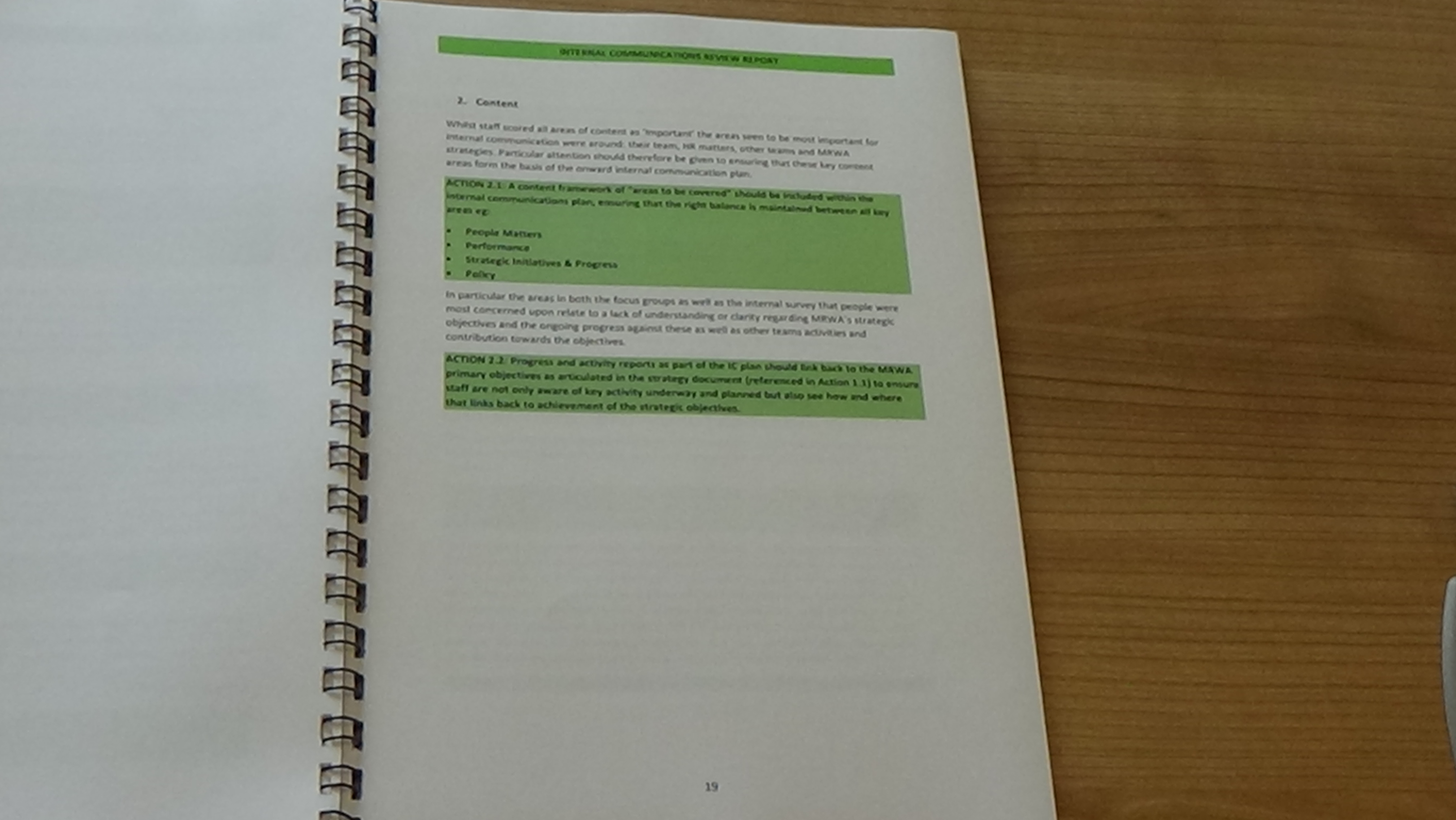

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 20

This page has two more general recommendations on content of internal communications.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 21

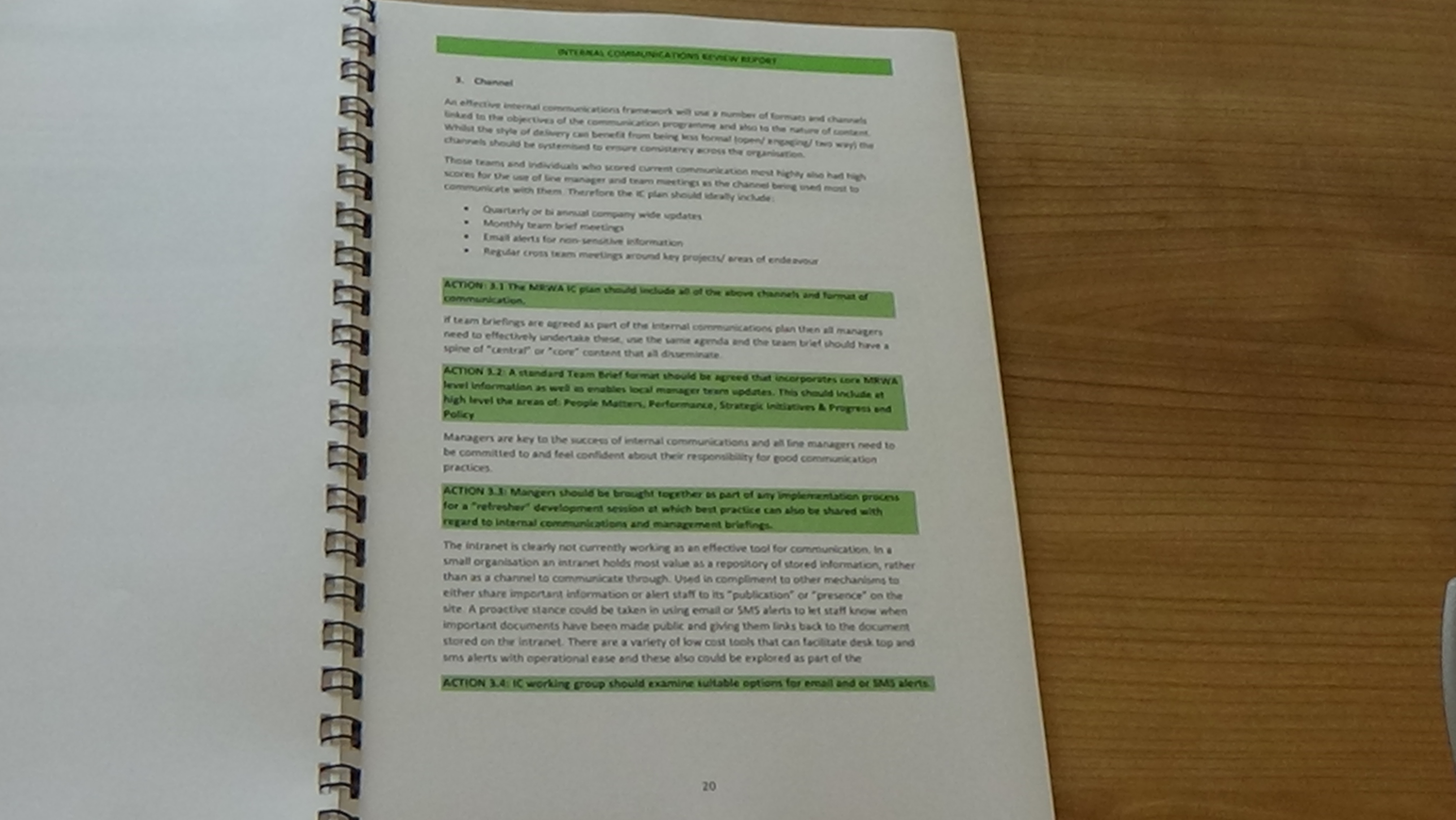

This page has recommendations on the channel used for communication.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 22

This page suggests that positive external PR news should be circulated internally to staff.

Paver Smith report on internal communications to Merseyside Recycling and Waste Authority page 23

Finally, in the concluding remarks and next steps it recommends that the reports findings and recommendations are presented to the Executive Management Team and to the wider management and staff cohort.

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.

Why was I “gagged” from writing about a £1.2 billion contract?

Why was I “gagged” from writing about a £1.2 billion contract?

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

A few weeks ago as part of the public’s rights under the audit when the public can inspect various invoices and contracts for three weeks each year I requested this particular contract, although as there weren’t any payments made on this contract under the last financial year, they first of all classed it as a freedom of information request, then they got back to me and said now it’s an Environmental Information Regulations request.

Now if you look up what these definitions actually mean in the Communications Act 2003, right, body means any body or association of persons, whether corporate or unincorporate, including a firm; so that could just mean me and Leonora, now the definition of programme services is a bit more complicated but the definition of programme services means a television programme service, the public teletext service, an additional television service, a digital additional television service, a radio programme service or a sound service provided by the BBC and then it goes on to define “television programme” means any programme (with or without sounds) which is produced wholly or partly to be seen on television and consists of moving or still images or of legible text or of a combination of those things.

Now I’ve checked whether videos on this Youtube channel are being watched on TVs and I’ll just have a quick look on my laptop and see. Yes, over the last year there have been 189 views on smart TVs and set top boxes for TV. So therefore strangely enough I come under the definition of, this comes under the definition of television programme and therefore the regulations do not apply to this particular document so I don’t have to ask their permission to publish it because it’s to do with this programme service and that’s why I’m recording this.

However on a final note I’d like to point out that the, shall we say the principle that every time somebody in the media makes a freedom of information request or an environmental information regulations request, before they use that information they’ve got to ask for permission from the public body to reuse it and state what purpose it’s for is well for anybody in the media who makes a freedom of information request and then writes stories on them is not the way it’s done.

Err, I don’t know if anybody else has heard of these regulations or whether they’re going to crop up in future FOI requests even though I think Wirral Council would quite like to send a boilerplate text at the end of each reply they send to me saying that I can’t use them unless I get their permission under the Re-Use of Public Sector Information Regulations 2015 in which case I’ll just make another video like this and then it doesn’t apply.

Anyway going back to the £1.2 billion contract between Merseyside Waste Disposal Authority or now Merseyside Recycling and Waste Authority and SITA Sembcorp UK Limited. This is an 864 page contract that over the lifetime of the contract they will pay out £1.2 billion for and relates to for years and years and years basically putting Merseyside’s rubbish on a train, sending it up to somewhere in the North-East of England, burning it and generating electricity from the rubbish.

I’m not sure what happens to the rubbish after they’ve burnt it but perhaps I need to read the contract better but I will be publishing the contract along with this video on my website so you can have a look for yourself. On the subject of the information that is blacked out, I’ll be looking into whether I’ll make a whatever the, I think it’s a reconsideration under the Environmental Information Regulations request for that information to be revealed but I’ll have to look into the detail and unfortunately basically the way the contract is worded it’s very unlikely that I’ll get access to the financial information in it but I’ll publish the rest of it on my blog, so you can have a read to see what your money will be spent on from 2017.

Now the two other places that were affected by this decision decided to take the government to judicial review, I don’t know what happened as a result of that and finally the only other thing to point out about this contract is that there were, in the end two bidders for this contract one of whom was obviously the successful contractor SITA Sembcorp UK Limited.

Now the court case was eventually settled out of court, the second placed contractor basically asked for Merseyside Waste Disposal Authority to pay all the profit they would have got if they’d been awarded the contract and of course Merseyside Waste Disposal Authority doesn’t have that kind of money because it would be over £100 million. I can’t remember what the estimate was, I think it was something between £100 million and £200 million. So anyway that’s the last thing I wanted to say about this and I hope you enjoyed this video and the contract is on my blog.

“(2) These Regulations do not apply to a document unless it—

(a) has been identified by the public sector body as being available for re-use;

(b) has been provided to the applicant; or

(c) is accessible by means other than by making a request for it within the meaning of the 1998 Act, the 2000 Act (or where appropriate the 2002 Act) or the 2004 Regulations (or where appropriate the 2004 Scottish Regulations).”

and whether this means:

(a) the regulations don’t apply to FOI requests, EIR requests or data protection act requests or

(b) the regulations apply to everything but FOI requests, EIR requests or data protection act requests

and leave a comment it would be appreciated.

UPDATED 17:45 28/7/15 Merseyside Waste and Recycling Authority have today stated "the Authority is aware of its obligations in relation to transparency, and the publication of public sector information. We are more than happy that members of the public can access this material, and are free to question, query and publish aspects of the Authority’s work."

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.