Accountability failures by local government highlighted in report by Research for Action and High Court Judge

Accountability failures by local government highlighted in report by Research for Action and High Court Judge

By John Brace (Editor) and Leonora Brace (Co-Editor)

First publication date: 28th April 2021, 05:48 (BST).

The three boxes on the left comprise the PFI fire stations contract

A 40 A4 page report published today (28th April 2021) by Research for Action titled Democracy Denied: Audit and Accountability Failure in Local Government looked at the experience of those who have tried (during a 30 working day period each year) to inspect the financial records of councils, as well as the experience of those who have asked questions of auditors or made objections using rights in the Local Audit and Accountability Act 2014 (in England) or the Local Authority Accounts (Scotland) Regulations 2014 (in Scotland). The report concentrates on requests to inspect, as well as related rights to ask questions to the auditor and/or object to the auditor. The report is mainly about requests in relation to PFI (Private Finance Initiative) schemes or LOBO (Lender Option Borrower Option) loans. Continue reading “Accountability failures by local government highlighted in report by Research for Action and High Court Judge”

What will Cllr Phil Davies answer to a question about the financial risks of Hoylake Golf Resort?

What will Cllr Phil Davies answer to a question about the financial risks of Hoylake Golf Resort?

Photo 4 – Cllr Phil Davies answering questions at the Birkenhead Constituency Committee public meeting (1st March 2018)

Ed – this was edited on 20th March 2018 at 9:33 pm to include video of the questions to Cllr Phil Davies and answers given on the 19th March 2018

Tonight (19th March 2018) I will be asking at a public meeting of Wirral Council’s councillors the following question of Cllr Phil Davies about Hoylake Golf Resort:

Cllr Phil Davies has explained at a number of public meetings what he thinks the benefits of the Hoylake Golf Resort project are, could he further please explain how the financial risks (including the financial risk of Wirral Council lending the developer millions of pounds if planning permission is granted) will be both managed and mitigated please?

What are the changes to citizen audit for 2015/16?

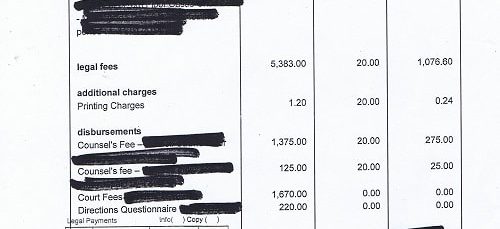

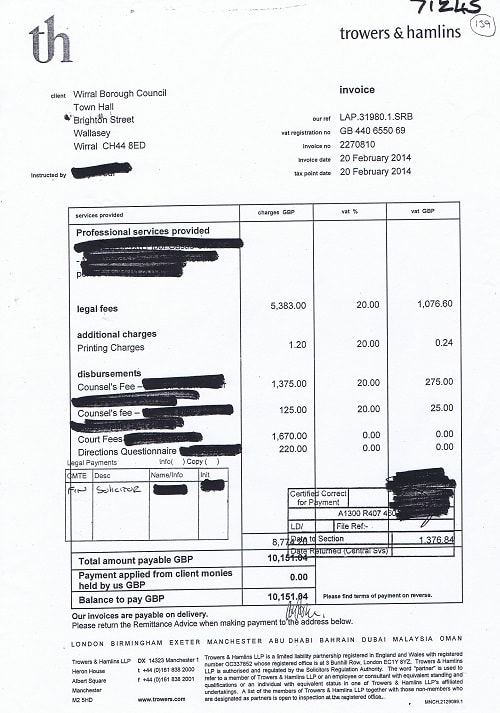

An example of an invoice supplied by Wirral Council during a previous audit

This year citizen audit changes. No longer are citizen audit rights covered by part II of the Audit Commission Act 1998 and the underlying regulations as this is no longer in force.

Previously during citizen audit, public bodies could redact information about the names of their own staff, but if it was information about anyone else they had to get their auditor’s approval.

Now, public bodies can redact parts of documents or whole documents on grounds of commercial confidentiality (although a public interest test has to be carried out) and information about the names of their own staff. They are also allowed to redact information that is the name of other individuals but not if it’s the name of a sole trader.

Previously the auditor had to consider all objections (as long as a copy was sent to the public body) made by local government electors for a declaration that an item of account is unlawful, recovery of an amount not accounted, a public interest report or an immediate report.

Now, an objection can only be about a matter that the auditor could write a public interest report about or declare that an item of account is unlawful but the auditor can decide not to consider the objection if:

(a) the auditor thinks it is frivolous or vexatious, or

(b) the cost to the auditor investigating is disproportionate to the sums involved or

(c) it repeats an objection already made and considered by the auditor whether in that financial year or a previous financial year.

However the auditor won’t be able to decide not to consider an objection if it is "an objection which the auditor thinks might disclose serious concerns about how the relevant authority is managed or led".

Even if the auditor rejects an objection for one or more of the reasons above the auditor can still make a recommendation to the public body.

Previously the Audit and Account Regulations 2011 required the inspection period was 20 working days regulation 9 and also that an advertisement was published (as well as a notice on its website) 14 days before this inspection period started regulation 10.

Under the new regime, this changes. There will be a longer inspection period of thirty working days, but this period will now also be the time during which objections and questions to the auditor must be made.

In March I asked the Cabinet Member Councillor Adrian Jones about this. The video of that question and Councillor Adrian Jones’ reply is below (although the link in the previous sentence also has a transcript of the question and answer).

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

Here are two quotes from what I asked Councillor Adrian Jones back in March:

JOHN BRACE: For the taxi journeys made by councillors that were not included in the annual published lists for 2013/14 and those made since can you confirm:

…..

(b) what changes will be made so that the expenses for such journeys made in 2014/15 will be included next time the annual lists are published? Thank you. “

COUNCILLOR ADRIAN JONES (CABINET MEMBER FOR SUPPORT SERVICES): The Council has negotiated competitive prices and entered into contracts with a local taxi company to provide transport for Members in accordance with the Members Allowances Scheme. The taxi company submits its invoices and the details of the Members that used the taxis each month directly to the Council for payment. The advantage of this arrangement is that the cost of transport by taxis is always at the negotiated rate and is a more efficient way to manage the service.

Now these costs have not been published on that basis previously, however in future the cost of Member’s taxi journeys undertaken pertinent to these taxi contracts will be published on the Council’s website as soon as practicable after the end of each financial year.

So I’d estimate the total for the year would be around £2,400. The Members Allowances 2014-15 has a column for car mileage (which is for when councillors claim money for using their own cars to travel to meetings) and not for taxis.

The only other column taxi expenses could fall into is “Re-imbursement of expenses” , which only totals £836.60 and is lower than the part-year figures for taxis of £1,829.65 provided in response to the Freedom of Information request.

I recently asked a person who regularly comments on this blog, what should the media do in response to whistleblowing? The answer I was given was “The right thing by the tax paying public”.

I don’t think there’s much further or anything more I can go with this topic though. Wirral Council is proud of its recent "Most Improved" award. When a Wirral Council employee writes an answer for a Cabinet Member to read out at a public meeting that has a specific promise that something will be changed, but it isn’t there has been a betrayal of trust. Someone has to be accountable and apologise (whether in public or private) for this and Wirral Council has to learn to take its legal obligations seriously.

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.

{kind=link}