Councillors on Merseyside Fire and Rescue Authority agreed to nearly 2% rise in fire element of council tax (from April 2022) for residents in Wirral, Liverpool, St Helens, Knowsley and Sefton

Councillors on Merseyside Fire and Rescue Authority agreed to nearly 2% rise in fire element of council tax (from April 2022) for residents in Wirral, Liverpool, St Helens, Knowsley and Sefton

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

Merseyside Fire and Rescue Authority (Budget) 24th February 2022 Left to Right Phil Garrigan (Chief Fire Officer (Merseyside Fire and Rescue Service) and Chief Executive (Merseyside Fire and Rescue Authority)), Councillor Leslie T Byrom (Chair, Merseyside Fire and Rescue Authority), Ria Groves (Monitoring Officer (Merseyside Fire and Rescue Authority)) and Shauna Healey (Democratic Services Manager (Merseyside Fire and Rescue Service))

By John Brace (Editor)

First publication date: Friday 25th February 2022, 2:44 (GMT).

What are the changes to citizen audit for 2015/16?

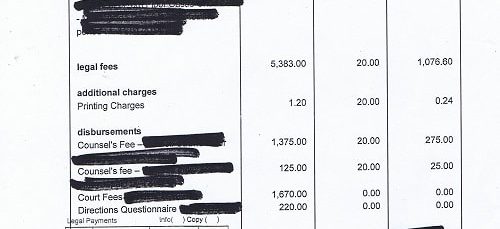

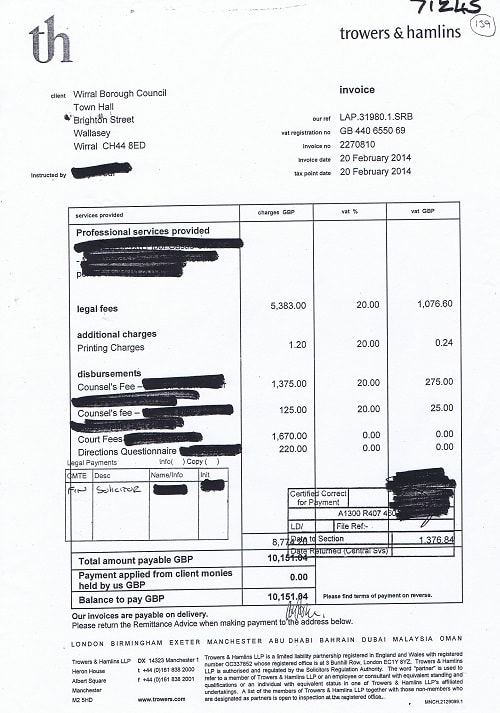

An example of an invoice supplied by Wirral Council during a previous audit

This year citizen audit changes. No longer are citizen audit rights covered by part II of the Audit Commission Act 1998 and the underlying regulations as this is no longer in force.

Previously during citizen audit, public bodies could redact information about the names of their own staff, but if it was information about anyone else they had to get their auditor’s approval.

Now, public bodies can redact parts of documents or whole documents on grounds of commercial confidentiality (although a public interest test has to be carried out) and information about the names of their own staff. They are also allowed to redact information that is the name of other individuals but not if it’s the name of a sole trader.

Previously the auditor had to consider all objections (as long as a copy was sent to the public body) made by local government electors for a declaration that an item of account is unlawful, recovery of an amount not accounted, a public interest report or an immediate report.

Now, an objection can only be about a matter that the auditor could write a public interest report about or declare that an item of account is unlawful but the auditor can decide not to consider the objection if:

(a) the auditor thinks it is frivolous or vexatious, or

(b) the cost to the auditor investigating is disproportionate to the sums involved or

(c) it repeats an objection already made and considered by the auditor whether in that financial year or a previous financial year.

However the auditor won’t be able to decide not to consider an objection if it is "an objection which the auditor thinks might disclose serious concerns about how the relevant authority is managed or led".

Even if the auditor rejects an objection for one or more of the reasons above the auditor can still make a recommendation to the public body.

Previously the Audit and Account Regulations 2011 required the inspection period was 20 working days regulation 9 and also that an advertisement was published (as well as a notice on its website) 14 days before this inspection period started regulation 10.

Under the new regime, this changes. There will be a longer inspection period of thirty working days, but this period will now also be the time during which objections and questions to the auditor must be made.