Grant Thornton accepts as “eligible” objection to the 2020-21 accounts for Merseyside Police and the Office of the Police and Crime Commissioner for Merseyside

Grant Thornton accepts as “eligible” objection to the 2020-21 accounts for Merseyside Police and the Office of the Police and Crime Commissioner for Merseyside

By John Brace (Editor) and Leonora Brace (Co-Editor)

First publication date: Monday 13th September 2021, 4:13 PM (BST).

Why is Wirral Council’s draft 2015/16 statement of accounts to be amended following concerns by myself and their external auditor?

Why is Wirral Council’s draft 2015/16 statement of accounts to be amended following concerns by myself and their external auditor?

Tom Sault (Acting Section 151 Officer) Wirral Council at the Audit and Risk Management Committee on the 13th June 2016

I’d perhaps better start by declaring the interest that I’m the person the letter below is to, in response to a letter I wrote to Robin Baker.

In an update to Why am I objecting to Wirral Council’s draft statement of accounts for the 2015/16 financial year? published on the 11th July 2016, I have today received a further reply (that you can read below) from Wirral Council’s auditors Grant Thornton dated 19th July 2016 which I quote from below. I’ve linked to the legislation referred to and the page of the statement of accounts that’s the issue. It seems they agree with me (although curiously don’t address the issue of bonuses too in their letter). I’ve left out some of the bits of their headed notepaper which I summarise in brackets ().

Please note the below letter I quote from was written by Robin Baker of Grant Thornton UK LLP (not myself).

I note from your letter that you wish to raise an objection to the accounts of Wirral Metropolitan Borough Council. You identify that the draft accounts included on the Council”s website does not comply with the requirements contained within the Accounts and Audit Regulations 2015. Specifically for Category 1 authorities there is a requirements under Regulation 2(1)(a) that for employees who salary is more than £150,000 per year, that the name of the employee is included within the Senior employee remuneration table. You highlight the Council’s Chief Executive is on a salary in excess of £150,000 yet he is not named in the table at note 32 of the draft accounts. You ask us to let you know whether we will consider this objection.

As part of our audit process I have reviewed the draft financial statements prepared by the Council. My review also highlighted the omission of the name of the Chief Executive from note 32 to the draft financial statements and I asked my team to raise the matter with the Council. The Council has acknowledged that the failure to name the Chief Executive in the draft financial statements is an oversight that will be corrected in the revised financial statements that will be published before 30 September 2016.

Thank you for raising this matter with me. Given the Council acknowledges the failure to name the Chief Executive is an oversight and will be corrected, we do not consider there is a need to treat this matter as a formal objection to the accounts. The failure to comply with the regulations will be corrected and there will be no continuing breach that would require us to consider whether the accounts are contrary to law.

If you do not agree with this view, please let me know as soon as possible.

Yours sincerely,

(signature)

Robin Baker

Director

For Grant Thornton UK LLP

(bit at the bottom about how they’re Chartered Accounts, a LLP registered in England and Wales, registered office details, list of members available, regulated by the Financial Conduct Authority, member firm of Grant Thornton International (GTIL) etc)

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.

What are the changes to citizen audit for 2015/16?

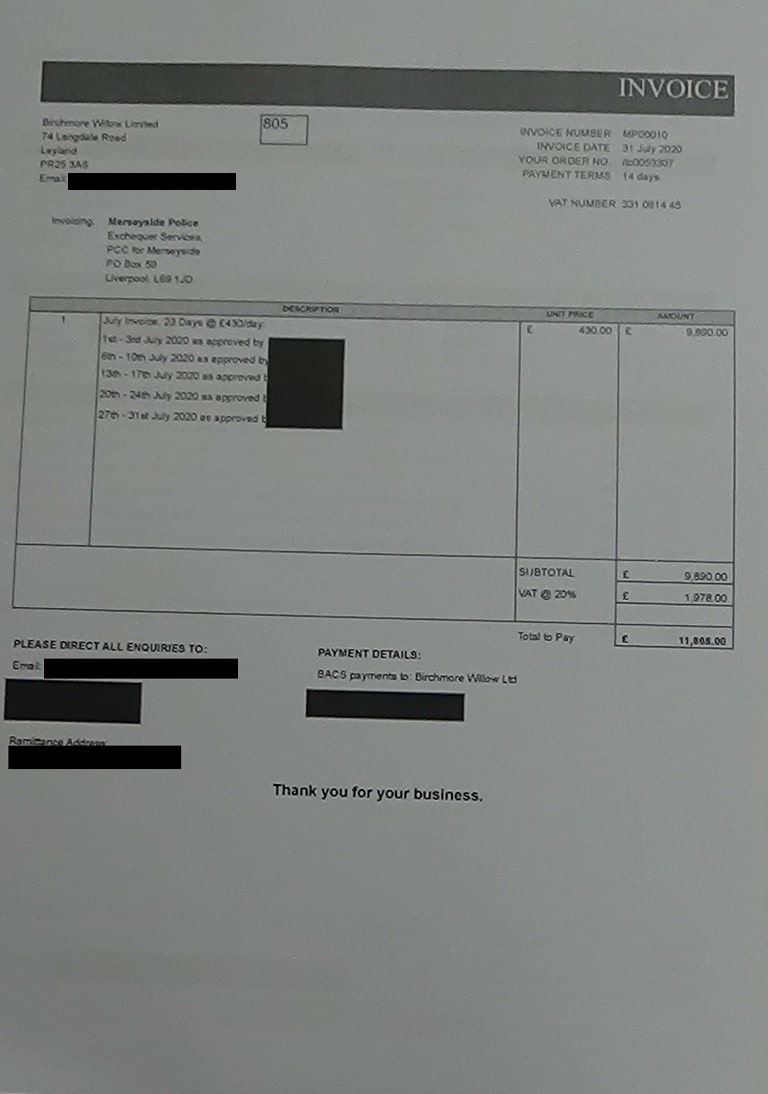

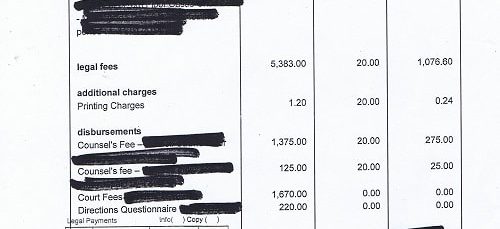

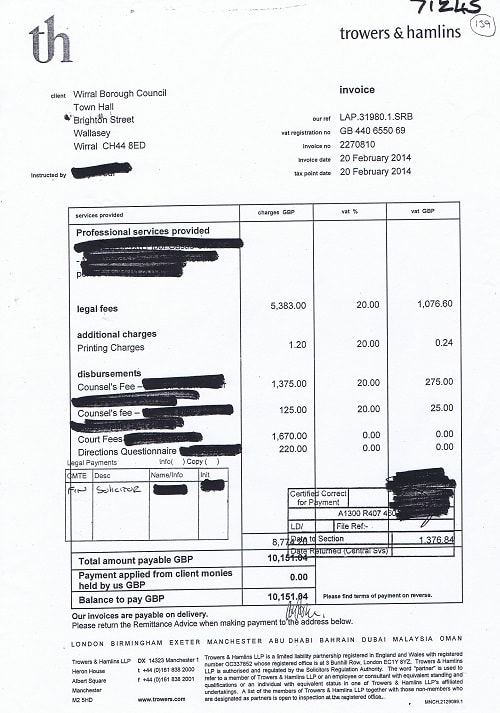

An example of an invoice supplied by Wirral Council during a previous audit

This year citizen audit changes. No longer are citizen audit rights covered by part II of the Audit Commission Act 1998 and the underlying regulations as this is no longer in force.

Previously during citizen audit, public bodies could redact information about the names of their own staff, but if it was information about anyone else they had to get their auditor’s approval.

Now, public bodies can redact parts of documents or whole documents on grounds of commercial confidentiality (although a public interest test has to be carried out) and information about the names of their own staff. They are also allowed to redact information that is the name of other individuals but not if it’s the name of a sole trader.

Previously the auditor had to consider all objections (as long as a copy was sent to the public body) made by local government electors for a declaration that an item of account is unlawful, recovery of an amount not accounted, a public interest report or an immediate report.

Now, an objection can only be about a matter that the auditor could write a public interest report about or declare that an item of account is unlawful but the auditor can decide not to consider the objection if:

(a) the auditor thinks it is frivolous or vexatious, or

(b) the cost to the auditor investigating is disproportionate to the sums involved or

(c) it repeats an objection already made and considered by the auditor whether in that financial year or a previous financial year.

However the auditor won’t be able to decide not to consider an objection if it is "an objection which the auditor thinks might disclose serious concerns about how the relevant authority is managed or led".

Even if the auditor rejects an objection for one or more of the reasons above the auditor can still make a recommendation to the public body.

Previously the Audit and Account Regulations 2011 required the inspection period was 20 working days regulation 9 and also that an advertisement was published (as well as a notice on its website) 14 days before this inspection period started regulation 10.

Under the new regime, this changes. There will be a longer inspection period of thirty working days, but this period will now also be the time during which objections and questions to the auditor must be made.