What is in 13 Merseytravel/Liverpool City Region Combined Authority contracts and hundreds of pages of invoices relating to the 15/16 financial year?

What is in 13 Merseytravel/Liverpool City Region Combined Authority contracts and hundreds of pages of invoices relating to the 15/16 financial year?

Councillor Steve Foulkes (Labour) (right) speaking at a recent meeting of the Birkenhead Constituency Committee (28th July 2016) | Councillor Pat Cleary (Green) (left) listens. Cllr Steve Foulkes is Merseytravel’s Lead Councillor for Finance and Strategy.

Merseytravel and the Liverpool City Region Combined Authority were the last public body to respond to my request to inspect and receive copies during the 30 working day period which was originally supposed to run starting on the 1st July 2016.

This was interesting as the 30 working day period isn’t allowed to start until the public notice is published!

However the FOI request went to an internal review and Julie Watling of Merseytravel responded on the 11th August stating that, “However I had been mistakenly informed that the information was not on the website, when in fact it was available at the following links:-”

But then, is it reasonable to expect an organisation to know what’s published on its own website and to answer Freedom of Information Act requests accurately or am I asking too much?

Which is the correct answer?

However the information (or to be more accurate part of the information) I requested arrived in the post yesterday (postage around £6.20 as it was special delivery guaranteed by 1pm) with a covering letter from a trainee solicitor and DVD.

Below is what was on the DVD. I did get a further email yesterday with a contract that had been mistakenly left off the DVD too.

Although the internal review clears up the issue about the public notice on Merseytravel’s website, for the Liverpool City Region Combined Authority it should’ve been published on the Liverpool City Region Combined Authority’s website, not Merseytravel’s.

So part of my objection I sent to the auditors yesterday still stands.

The invoices are split by the thirteen accounting periods that Merseytravel used during the 2015 2016 financial year, although why spoil the surprise when you can read for yourself below?

There are some interesting matters to be gleaned from the invoices and contracts, however I don’t have the time at present to blog about them in detail.

Invoices 2015 to 2016 financial year (Merseytravel and Liverpool City Region Combined Authority).

Did Wirral Council’s Pensions Committee really approve the accounts of the £6.9 billion Merseyside Pension Fund?

Did Wirral Council’s Pensions Committee really approve the accounts of the £6.9 billion Merseyside Pension Fund?

Pensions Committee (Merseyside Pension Fund) 15th September 2015 Left Peter Wallach Head of Pensions Right Cllr Paul Doughty Chair of the Pensions Committee

Below is a copy of my statutory objection to the approval of the accounts of the Merseyside Pension Fund (a £6.9 billion pension fund that form part of Wirral Council’s accounts) which go to Wirral Council and its auditors Grant Thornton.

It’s rather dull and technical, but in the interests of openness and transparency I am publishing it below. It relates to yesterday’s meeting of the Pensions Committee that can be viewed below. I was so cheesed off I made two spelling mistakes in the email (a corrected version is below).

Plus ça change, plus c’est la même chose!

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

Wirral Council’s Pension Committee public meeting of the 15th September 2015 Part 1 of 2 (Merseyside Pension Fund)

I reckon receiving this email will probably be about as welcome at Wirral Council as someone breaking wind in an open plan office. However such is life! The press are independent for a reason!

Subject: Statutory objection to Pensions Committee approval of Merseyside Pension Fund Accounts for 2014/15

CC: Pat Philips

CC: Colin Hughes

CC: Surjit Tour

CC: Peter Wallach

CC: Joe Blott

CC: Tom Sault

CC: Cllr Paul Doughty

CC: Cllr Ann McLachlan

CC: Cllr George Davies

CC: Cllr Treena Johnson (email address unknown)

CC: Cllr Adrian Jones

CC: Cllr Brian Kenny

CC: Cllr Geoffrey Watt

CC: Cllr Kathy Hodson

CC: Cllr Cherry Povall

CC: Cllr Pat Cleary

CC: Cllr Anita Leech

CC: Cllr Nick Crofts (Liverpool City Council)

CC: Cllr John Fulham (St Helens Council)

CC: Cllr William Weightman (Knowsley Council)

CC: Paulette Lappin (Sefton Council)

CC: Cllr Jim Crabtree

CC: Cllr Ron Abbey

CC: Cllr Chris Blakeley

CC: Cllr Angela Davies

CC: Cllr David Elderton

CC: Cllr Phil Gilchrist

CC: Cllr John Hale

CC: Cllr Matthew Patrick

CC: Fiona Blatcher

CC: Heather Green

CC: Chris Blakemore

Dear all,

I am a local government elector in the Wirral Metropolitan Borough Council area and make this statutory objection to the Pensions Committee approval of the the Merseyside Pension Fund Accounts for 2014/15 (see Audit Commission Act 1998, s.16).

For the purposes of clarity to the auditor this is a statutory objection to a matter not in relation to a matter covered by Audit Commission Act 1998, s.17-18 but Audit Commission Act 1998, s.8.

As required I am sending a copy of this objection to the auditor, those I have contact details for on Wirral Council’s Pensions Committee (I do not have an email address for Cllr Treena Johnson), Wirral Council’s Audit and Risk Management Committee and those tasked with corporate governance at Wirral Council such as the Monitoring Officer Mr. Tour, the Head of Pensions Peter Wallach, the Strategic Director for Transformation and Resources Joe Blott and Tom Sault the Acting 151 Officer as well as other relevant people.

I do not have contact details for some on the Pensions Committee. I am sending this to the officer who took the minutes of the Pensions Committee meeting on the 14th September 2015 in the hope that it can be forwarded to those I do not have contact details for (the non-councillor members and Cllr Treena Johnson).

As this is a rather technical objection, I provide below a summary of the key points.

However I first need to declare an interest. I have a close family relative who is currently paid a pension by Merseyside Pension Fund, therefore a close interest in the corporate governance of the Fund being done properly.

On the 14th September 2015, I and three other members of the public (two of whom were employed by Grant Thornton and are Wirral Council’s auditors) attended a public meeting of Wirral Council’s Pensions Committee.

This meeting was filmed by myself and published shortly after, see

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

and

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

.

One of the functions of the Pensions Committee as detailed in Wirral Council’s constitution is to approve the statement of accounts and financial statements of the Merseyside Pension Fund and recommend these to the Audit and Risk Management Committee.

This is because the Merseyside Pension Fund forms part of Wirral Council’s accounts. There is a statutory deadline to approve the statement of accounts for the 2014/15 financial year by the 30th September 2015.

As mentioned at the Pensions Committee itself by one of the councillors this Fund is valued at ~£6.9 billion.

Item 4 and 5 on the agenda of that meeting were the pension fund accounts 2014/15 and draft annual report.

As the Pensions Committee is a public meeting of a local authority, legislation that governs public meetings applies to it. The statement of accounts formed part of a document known as the “Report & Accounts 2014/15” which was given to those on the Pensions Committee present on the afternoon of the meeting itself.

Please note the reference below to principal council, by virtue of Local Government Act 1972, s.100E also apply to committees and sub-committees of a principal council. The Pensions Committee is a committee of a principal council.

Local Government Act 1972, s.100B(4), is quite clear on the procedure that should be followed in the case of agenda items that are not open to inspection by members of the public five clear days before the meeting.

(4) An item of business may not be considered at a meeting of a principal council unless either—

(a) a copy of the agenda including the item (or a copy of the item) is open to inspection by members of the public in pursuance of subsection (1) above for at least [five clear days] before the meeting or, where the meeting is convened at shorter notice, from the time the meeting is convened; or

(b) by reason of special circumstances, which shall be specified in the minutes, the chairman of the meeting is of the opinion that the item should be considered at the meeting as a matter of urgency.

It is clear that the Report & Accounts 2014/15 for the Merseyside Pension Fund did not fall under the description in s. 100B (4)(a) and therefore the procedure in 100B(4)(b) applies. The Chairman of the Pensions Committee Cllr Paul Doughty did not specify at the meeting itself his opinion that the item should be considered as a matter of urgency, nor would the reasons for this be specified in the minutes.

This is an important corporate governance safeguard written into legislation.

Firstly, if the documents are not made available to the public five clear days before the meeting, the public and press cannot scrutinise them. Secondly (as was mentioned at the meeting itself) at least one councillor expressed the view that half an hour was insufficient to scrutinise a highly technical 46 page document.

This is not a one off occurrence. Officers in previous years have frankly played these games of brinkmanship with accounts routinely handed to those tasked with corporate governance to approve on the evening of the meeting itself. The safeguard above in s.100(4)(b) above, details a procedure to be followed if the matter is urgent.

Therefore my objection is that because of what I have detailed above, the Pensions Committee did not approve the statement of accounts for the Merseyside Pension Fund because:

(a) the report was late and

(b) it is clear from the legislation that a procedural step was missed making the decision ultra vires.

I am however not an unreasonable person and suggest the following course of corrective action. If this is followed I will happily withdraw my objection.

i) That the Pensions Committee holds a further meeting between now and 30th September 2015.

ii) The Audit and Risk Management Committee recommendation is altered (agenda item 12 meeting of the 22nd September 2015) to be conditional on the meeting outlined in i) and the same for any Cabinet meeting that has to approve the same item

iii) That at this special meeting it considers the items referred to in this objection in a way that is not open to legal challenge or perceived to be ultra vires and that the information for this meeting is published on Wirral Council’s website five clear days before the meeting.

As Wirral Council’s auditors Grant Thornton will no doubt make clear, the matter that forms this objections needs to be resolved before the accounts are signed off. I look forward to reading and hearing responses to this objection.

However as this is a perceived serious corporate governance failing, I am making this objection public.

Yours sincerely,

John Brace

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.

What connects “persons interested”, Tharmathevy Thanabalasingam and Liverpool City Council?

What connects "persons interested", Tharmathevy Thanabalasingam and Liverpool City Council?

As regular readers of this blog will know, I exercised my Audit Commission Act 1998, s.15(1) right to inspect invoices and contracts at Merseytravel (now part of the Liverpool City Region Combined Authority), Merseyside Fire and Rescue Authority, Merseyside Waste Disposal Authority (who go by the public name of Merseyside Recycling & Waste Authority) and Wirral Council for the 2014/15 financial year.

It’s well established that "persons interested" in Audit Commission Act 1998, s.15(1) means local government electors for the public body concerned.

The problem however came with my request to Liverpool City Council, as I’m not a local government elector in the Liverpool City Council area. Case law has determined that “interested person” (a term sadly not defined in the legislation itself) is a wider group than just local government electors.

R (HTV Ltd) v Bristol City Council [2004] 1 WLR 2717 is an interesting case that as far as I know isn’t available online so I looked it up in the university law library. I’ll refer to R (HTV Ltd) v Bristol City Council [2004] 1 WLR 2717 [24], [25], [39], [49] and [50] as it goes into the legislative history of who is considered an “interested person”.

"The authorities

24. The concept of “persons interested” has received very little consideration by the courts. In Marginson v Tildsley (1963) 67 JP 226 the appellant was a member of the Fleetwood urban authority for 20 years before he became bankrupt and was disqualified from the council. He sought the right to inspect the accounts under the Public Health Act 1875. He preferred an information against the clerk of the council alleging that the clerk had wrongly refused him access to the accounts. The justices dismissed the information but their decision was overturned on appeal. Lord Alvertstone CJ held that he was a person interested because although no longer a member of the council, the possibility that his estate could be liable for any surcharge rendered him a person interested.

25. In the later case of R v Bedwellty Urban District Council, Ex p Price [1934] 1 KB 333 the court held that a person interested was entitled to inspect the accounts by an agent, who in that case was his accountant. It was argued that the accountant was a person interested in his own right, but the point did not have to be determined and Avory J expressly left it open.

39. He also referred me to a passage in Jones, Local Government Audit Law, 2nd ed (1985), ch 8. The last edition of this valuable book was sadly in 1985. But in a discussion on the meaning of the concept of a “person interested”, the author expressed the view that the right was attached to any person who had a financial interest in the accounts, as well as somebody with a legal interest, such as a local government elector who has the legal right of objection.

49. I think it is somewhat artificial to say that non-domestic ratepayers do not contribute to the local authority’s budget. Although their contributions are channelled through, and will be subject to, redistribution by central government – the income will be received indirectly by the authority as a grant from central government – nevertheless I think this gives them a sufficient interest in inspecting the accounts and satisfying themselves as far as they can that they are in order. In my view, this is reinforced by the fact that they had the right for their representatives to be consulted on expenditure decisions.

50. I consider that these factors together give them a real and close interest in the council’s activities sufficient to confer these rights upon them. I would, moreover, be reluctant to think that this right, which undoubtedly existed until the Local Government Finance Act 1988, had been removed as a consequence of the restructuring of local government finances in that year. It follows that in my view the claimant is a "person interested" within the section."

So from the above I can gather that the concept of "interested person" means:

local government electors (which for Liverpool City Council at the last election I estimate at around ~320,000 local government electors)

former politicians of that public body (although as I think the ability to surcharge councillors has been repealed this may not apply in most circumstances)

those assisting local government electors such as accountants

as the R (HTV Ltd) v Bristol City Council [2004] 1 WLR 2717 case above established a company or business based in the area covered by the public body that pays business rates (or by its more formal term of non-domestic rates)

However according to Liverpool City Council my request was refused because as far as they see it, I don’t fall into one of the above categories.

I do however have a legal interest in 22 of the invoices I requested as I made a FOI request for them on the 14th May 2015. Liverpool City Council refused to supply a copy of the invoices and also refused at internal review. I exercised my right under the Freedom of Information Act 2000, s.50 to complain to the regulator (the Information Commissioner’s Office about this) on the 31st July 2015 and a decision by ICO is awaited.

Some ICO decision notices take a much wider view as to the definition of “interested person”. This decision notice (FS50582149) at part of paragraph 62 states (ACA 1998 refers to the Audit Commission Act 1998):

"As stated in paragraphs 24 and 25 above, the ACA 1998 provides a right of access to inspect accounting information for their local authority to any local government elector and ‘any persons interested’. Although the term ‘interested person’ is not defined within the ACA 1998, the Audit Commission suggest the term must refer to an individual who has a legal or financial interest in the accounts which would include local government electors, non-domestic rate payers and those with a financial or contractual relationship with the Council or those in receipt of services from the Council."

Keen followers of local government will know that the Audit Commission doesn’t exist any more, however if the Liverpool City Council shared the view of the now defunct Audit Commission that an "interested person" as was someone "in receipt of services from the Council" then I certainly fall into that category!

However, this is going off the point a little and the next point will sound like an arcane legal point. I can’t request permission from a High Court Judge for judicial review of Liverpool City Council’s decision to refuse inspection/copies of the invoices under the audit legislation that relate to the FOI request. Why is that? That’s because it would be refused due to the existing right of appeal to ICO (Information Commissioner’s Office).

I would guess that if permission for judicial review was applied for, a High Court Judge would refuse permission to the part of the request to Liverpool City Council under the audit legislation that relates to the 22 invoices that pertain to the earlier FOI request on those grounds. This is because part 5 of the Pre-Application Protocol for Judicial Review makes it clear that "Judicial review should only be used where no adequate alternative remedy, such as a right of appeal, is available."

It is far better to establish the principle of whether the invoices are able to requested through FOI requests through an ICO decision notice. However before Liverpool City Council did a U-turn and realised I wasn’t a local government elector I did get copies of 7 invoices for its legal costs (the first of which is at the end of this article).

There will be a delay getting editorial approval with the other six as Liverpool City Council have done an extremely bad job at redacting some of the information. One of the invoices relates to a Family Court matter that it probably be unlawful for me to publish in its present form as the names of the parents and a child are clearly visible. Those more well versed in data protection law could perhaps leave a well-informed comment on why giving out such detail to a member of the public ain’t a good idea.

As usual the thumbnails are linked to higher resolution images for each page.

There’s a right of appeal of decisions of such committees (a Licensing and Gambling Sub-Committee is composed of councillors and meets in public) to the local magistrate court. The premises licence holder’s name is Tharmathevy Thanabalasingam (which is published in the report to that committee).

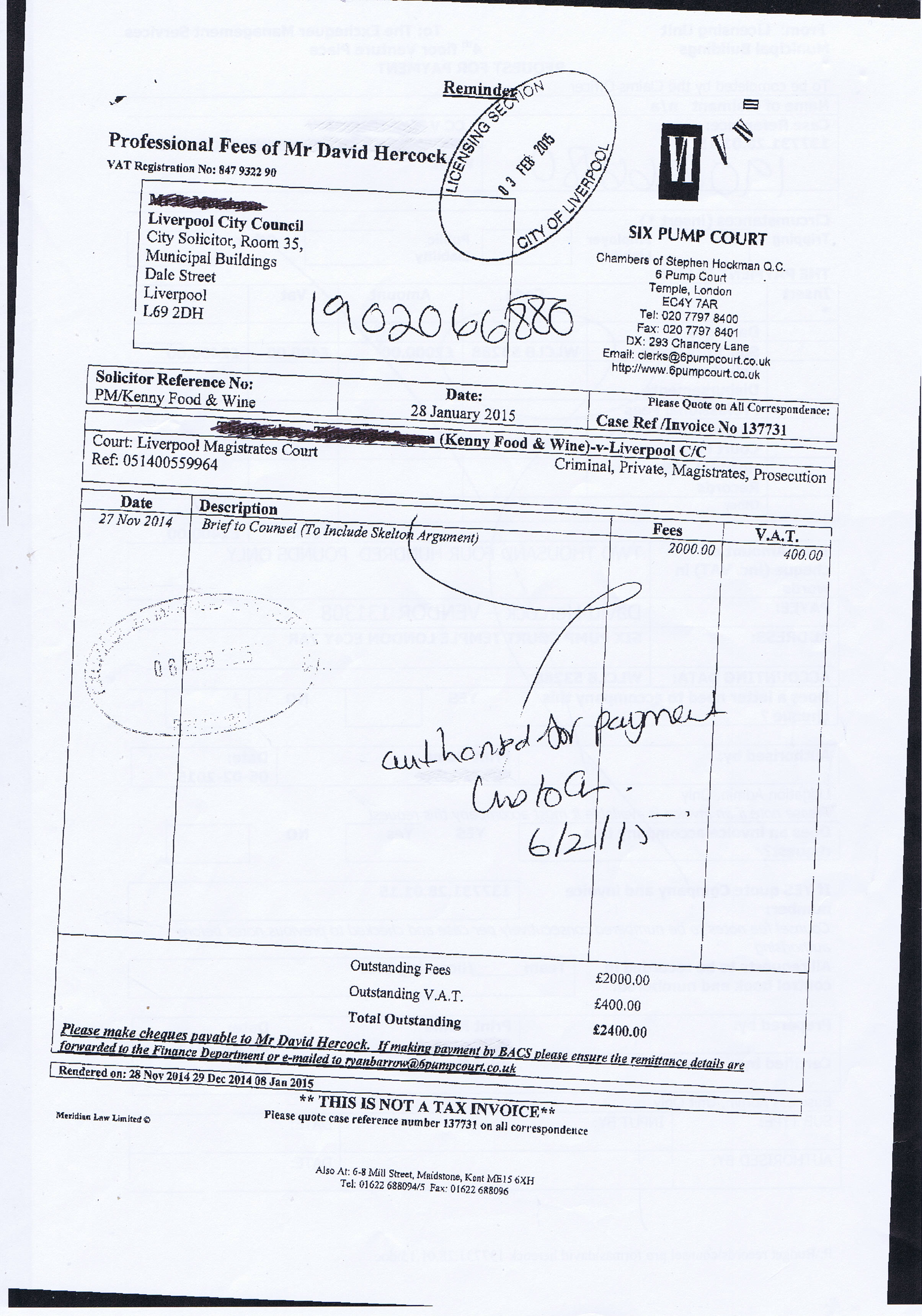

The Liverpool City Council solicitor this invoice went to is Mr. P Merriman. He’s the licensing, gaming and betting solicitor at Liverpool City Council.

Mr David Hercock of Six Pump Court is a barrister. The invoice is for £2,400 (£2000 + VAT).

Liverpool City Council invoice David Hercock Six Pump Court 28 January 2015 page 1 of 2 thumbnailLiverpool City Council invoice David Hercock Six Pump Court 28 January 2015 page 2 of 2 thumbnail

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.

Why did Wirral Council include Ian Coleman as a whistleblowing contact in the Passenger Transport Contract?

Why did Wirral Council include Ian Coleman as a whistleblowing contact in the Passenger Transport Contract?

Here is my first question to Wirral Council’s auditor (Grant Thornton) about the Passenger Transport Contract.

Wirral Council has a contract with Eye Cab Limited called the "Passenger Transport Contract". This contract started on the 1st September 2014 and runs to the 31st August 2015 and is for the provision of taxi services.

I requested to inspect a copy of the contract (see Audit Commission Act s.15(1)(a)) which was arranged for the 4th September 2015. As a local government elector for the Wirral area, I can question the auditor about the 2014/15 accounts from 9.30am on the 18th August 2015 until the accounts are closed (see Audit Commission Act 1998 s.15(2)).

Page 36 of the contract has a section titled "Section 5 CONFIDENTIAL COMPLAINTS PROCEDURE (Whistle-blowing) A Guide for Suppliers and Contractors (see attached page 36).

Passenger Transport Contract Wirral Council page 36 of 40

At the bottom of this page of the contract it details two people that a complaint under the whistleblowing procedure can be made to.

The second of these individuals is:

"Ian Coleman, Director of Finance, Wirral Borough Council, Finance Department, Treasury Building, Cleveland Street, Birkenhead, Merseyside, CH41 6BU"

Wirral Council’s Employment and Appointments Committee agreed early voluntary retirement for Ian Coleman on the 3rd October 2012 (see attached minutes).

Therefore as Ian Coleman was not an employee of Wirral Council at the time the Passenger Transport Contract was put out to tender (or when the contract was agreed) why was he included as a whistleblowing contact in the contract?

Yours sincerely,

John Brace

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.