Wirral Council’s auditors Grant Thornton issue adverse value for money conclusion on 2019–20 accounts

Wirral Council’s auditors Grant Thornton issue adverse value for money conclusion on 2019–20 accounts

By John Brace (Editor) and Leonora Brace (Co-Editor)

First publication date: 11th January 2021, 11:51 (GMT)

A previous public meeting of Wirral Council’s Audit and Risk Management Committee held on 27th January 2020

Tonight (11th January 2021) Wirral Council’s Audit and Risk Management Committee meets to agree to both its own accounts for 2019–20 and that of the Merseyside Pension Fund (Wirral Council is the Administering Authority for the Merseyside Pension Fund). The legal deadline for final audited local council accounts for 2019-20 was put back to the end of November 2020 because of the pandemic but Wirral Council is set to approve its accounts for 2019-20 considerably later than this deadline. Continue reading “Wirral Council’s auditors Grant Thornton issue adverse value for money conclusion on 2019–20 accounts”

Yesterday, there was a public meeting of Wirral Council”s Local Pension Board scheduled to start at noon. The Local Pension Board is part of the governance of the Merseyside Pension Fund that Wirral Council administer and has hundreds of thousands of people in the pension fund (mainly public sector workers) and a £multi-billion Pension Fund.

I am making an educated guess that either Commerz Real Investmentgesellschaft mbH contract out (or Merseytravel does) the reception staff at the building the public meeting was to be held in, which is done by I think Carlisle Security Services Limited (which is a subsidiary company of Carlisle Support Services Group Limited).

If you are confused by reading that so far, then so am I!

We arrived first at reception at Mann Island and they had been told we were coming to the meeting. So we were issued with visitors passes.

However we were told we couldn’t go in because no-one from Wirral Council was there yet.

Reception told us that we couldn’t go in (although they knew we were there for the meeting) until someone from Wirral Council told them it was ok for reception to allow us into the building to attend a public meeting. So we waited.

First to arrive was Pat Phillips (the Committee Clerk and point of contact for the meeting). Standing in front of reception we asked her to confirm we were there for the meeting. She said she would have to go ask someone (despite nobody else but us being there for the meeting).

So they let her through (and she didn’t come back as there was no-one else but her).

Then Joe Blott arrived, who is at Deputy Chief Executive level at Wirral Metropolitan Borough Council and therefore part of the political element of his job such as dealing with people like myself.

Again, Joe Blott insisted he could not tell reception staff at Mann Island that we could come in through the gate as it wasn’t a “Wirral Council building” and he needed to first consult with the Chair of the Local Pensions Board (who actually hadn’t arrived in the building yet).

However, reception staff let Joe Blott through too.

Reception staff then told us they couldn’t let us in because of “terrorism” training and that they had “orders”. They pointed it wasn’t a “public building”.

Apparently now terrorism is used as a reason to avoid legal responsibilities!

The public meeting was scheduled to start at noon and we were still there at reception when more people arrived for the meeting, Peter Wallach, John Raisin, Mike Hornby, Kerry Beirne, Donna Ridland, Pat Maloney and Roger Irvine to name but seven.

I also briefly talked around this time to the Chair of the Liverpool City Region Combined Authority Merseytravel Committee Cllr Liam Robinson about the problem.

Reception staff are then busy handing out visitors passes and bizarrely trying to determine when the Local Pensions Board plus myself and Leonora should be allowed through the gate on the ground floor to room GA-25.

Finally (at the third time of asking) we found a Wirral Council employee (Peter Wallach) who was willing to tell reception we were allowed into the building!

Eventually by the time we’re all let in, I come through the door to the meeting room (GA-25 on the ground floor) at about 11:59:30, most of the rest of the people behind me came in late.

Then of course, the room needs to be set up and surprisingly the lights turned on (as neither Joe Blott or Pat Phillips had turned the lights on). One Wirral Council officer introducing one of the reports arrived even later even though there was a delayed start to the meeting (which caused a further delay).

Common sense means letting the press in at least fifteen minutes before so that a safe space to film can be determined, a tripod put up, seating arranged, agendas and reports requested etc.

But I feel that since this legal requirement came into effect in August 2014 various parts of Wirral Council have tried to try my patience over it at various public meetings.

Delayed starts to meetings cost the public sector money in lost time.

Terrorism can not be used as an excuse to delay or prevent democracy happening or the press reporting. The legal right to attend public meetings of local councils has been in its current form since 1972 and in another form since 1960. It’s not new legislation!

Nearly every other meeting of Wirral Council’s committees has one of their solicitors present but this one does not!

This is sadly a recurring problem when attending to report and film public meetings at Mann Island. There have been public meetings that have started before we’re allowed in.

Merseytravel’s own Head of Internal Audit (Merseytravel lease room GA-25) has stated at a public meeting in 2014 that people should not talk to the press about whistleblowing concerns.

However who do the press blow the whistle to when there’s no point in blowing it internally? Write an article about it? Embarrass people into changing? Or does it just end up being like the film Groundhog Day with a public sector seemingly unable to stick to its own policy, the legislation and just full of excuses?

What it has shown me, that is of wider concern is that at Wirral Council some senior managers are frightened to make decisions. The culture of not making a decision, just in case it’s the wrong one or the manager may be criticised can be just as damaging to Wirral Council’s reputation as the myriad of other scandals (on subjects ranging from child protection, complaints about councillors, how requests for information are handled and so on and so on).

So below is footage of the Local Pensions Board which turned out to be an interesting meeting (albeit hard to hear due to the lack of microphones).

I had to skip ten minutes of checks to film it and had no chair to sit on (there was literally no time to get a chair before it started).

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

EXCLUSIVE: Leaked minutes of Merseyside Pension Fund’s Investment Monitoring Working Party held on the 17th September 2015

I will start off by declaring an interest as I have a close relative paid a pension by the Merseyside Pension Fund (which Wirral Council administers). My second declaration of interest is that in the section 6. Notes Action Points or Discussion Points, the reason for the extraordinary meeting of the Pensions Committee held on the 28th September 2015 was to resolve my objection to the 2014/15 accounts.

These are leaked minutes as only the first page comprising a list of those present, apologies and declarations of interest was published by Wirral Council as an appendix to this report considered by the Pensions Committee at its meeting on the 16th October 2015.

Below are the minutes of Wirral Council’s Investment Monitoring Working Party meeting held on the 17th September 2015.

Minutes of Investment Monitoring Working Party,

17th September 2015

In attendance:

(Chair) Councillor Paul Doughty (WBC)

Peter Wallach (Head of MPF)

Councillor Geoffrey Watt (WBC)

Joe Blott (Strategic Director Transformation and Resources)

Councillor Cherry Povall (WBC)

Leyland Otter (Senior Investment Manager)

Councillor Pat Cleary (WBC)

Greg Campbell (Investment Manager)

Councillor Adrian Jones (WBC)

Susannah Friar (Property Manager)

Councillor Brian Kenny (WBC)

Adil Manzoor (Tax Accountant)

John Raisin (Chair of Pension Board)

Noel Mills

Donna Ridland (Pension Board)

Rohann Worrall (Independent Advisor)

Louise-Paul Hill (Aon Hewitt)

Emma Jones (PA to Head of Pension Fund)

Apologies were received from:

Councillor Ann McLachlan (WBC)

Councillor Paulette Lappin

Declarations of Interest

Councillor Paul Doughty declared an interest due to a relation being a beneficiary of Merseyside Pension Fund.

Councillor Geoffrey Watt declared an interest due to a relation being a beneficiary of Merseyside Pension Fund.

Introduction

1. Minutes of the meetings held on 16 April 2015.

Cllr Paul Doughty (PD) opened the meeting. There were no amendments to the minutes.

Action points

None.

2. External Manager Presentations part 1

2.1 Nomura

The Nomura Portfolio Review was presented by Masaaki Tezuka (MT) the Chief Portfolio Manager (Japan) and Andrew Whitaker (AW) Head of Relations (UK). AW introduced the themes of the presentation and MT gave the performance overview and answered questions from the panel.

A discussion ensued with regard to the investment performance and the market review of the year to June 2015. The profits among Japanese manufacturers were debated and it was expressed that it is concealing the weakness in exports. MT stated that exports have been reduced but this is expected to pick up. The competitiveness against the Asian markets was quite strong due to the exchange rate of the yen. It was further discussed that the Japanese market is lagging behind the US and European market.

Action points

None.

3. External Manager Presentations part 2

3.1 JP Morgan – European Equities

Patrick Vermulean (PV), Paul Shutes (PS) and Monique Stephens presented their European equities review and reported on performance and current portfolio positioning. PV explained that Paul Shutes is replacing Nick Wilcox and will assume the responsibility for the client management of the mandate.

A discussion ensued with regard to Ryanair and their outlook for the future. It was explained that Ryanair have changed their focus toward the customer and are addressing their business and website to improve the overall service to create a better business model akin to Easyjet.

PV discussed how they endeavour to ‘take the noise out of the market’ by monitoring earnings consensus and broker analysis; looking at normal distribution to find stocks between two extremes. PV asserted that they have good contacts with management and use a consensus to take companies out of the equation. However, when companies are all moving in the same direction the signal can be weak.

Action points

None.

4. Quarterly Review

4.1 Management Executive

PJW presented the Quarterly Review which covered themes such as the collapsing values of Chinese equities, sovereign bond markets and global monetary policy. PJW asserted that Greece was the dominant theme overall.

PJW reported on a number of issues including global government bond markets and the performance of risk assets. The value of the fund and the funding position was looked at and the performance of the Fund over the quarter and over 1 and 3 years. The asset allocation and MTAA including the MTAA panel meeting on 16 June 2015 were also reported on.

A discussion ensued with regard to the formulation of the benchmark and the strategy of the asset allocation. It was stated that the benchmark is reviewed on an annual basis and the Independent Advisors also offer guidance on this process.

Action points

None.

4.2 Market Commentary

Noel Mills (NM) gave a market commentary and reported on the market background which has been affected by the decline of the global equity market post the second quarter. This is largely a result of the Chinese equity bubble bursting and the renewed possibility of a Greek default which could see a postponement of the US economy moving to higher interest rates. The volatility of the markets continues and US monetary policy is set to tighten.

Action points

None.

4.3 Aon Hewitt Update

Louis-Paul Hill (LH) presented the Strategic Monitoring Report of Aon Hewitt to members. Within his report he gave a funding level update which looked at how the estimated funding level has progressed since the 2010 valuation. The risk analysis, asset allocation, investment outlook and ideas and current research were also reported on.

An extract from that report follows below:

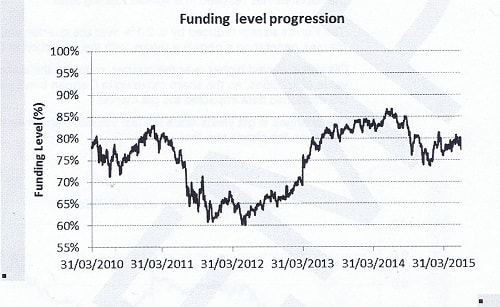

Funding Level Update

Introduction

The following section sets out an estimate of how the funding level has

progressed over the period from 31 March 2010 to 30 June 2015. lt also provides an attribution analysis of the changes in the funding level.

Mercer, the Fund’s actuary, has provided information regarding the Fund’s liabilities. The estimated funding level has been updated to account for the finalised valuation results from 31 March 2013.

Funding Level Progression (4.2 Market Commentary)

Notes:

Please note the funding level update and attribution analysis below do not constitute actuarial advice. They are instead our best estimate of how the funding level has evolved and the driving factors behind this. Further, we are not positioned to, nor do we, offer any comments on the appropriateness of the assumptions provided by the actuary.

The funding level fell between the actuarial valuation at 31 March 2010 and the actuarial valuation at 31 March 2013. Since the valuation at 31 March 2013, the funding level improved over the following 12 months to 85%, however the funding level deteriorated during the second half of 2014.

Using "like for like" assumptions (based on the assumptions from 31 March 2013) the funding level at 30 June 2015 remains broadly unchanged over the quarter at 77%.

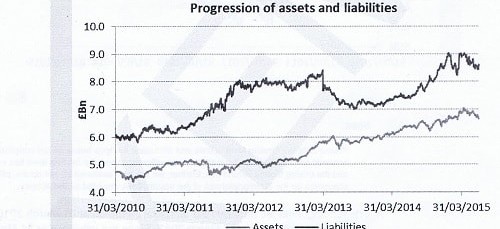

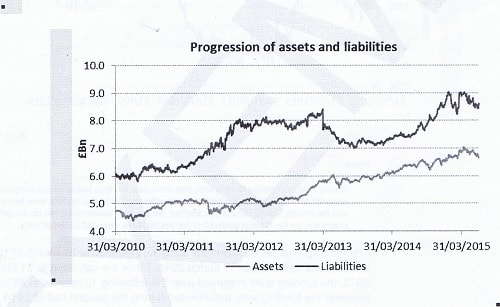

Asset and Liability progression

The chart below separates the estimated movement in the funding level from the 2010 and 2013 valuation dates into: the estimated liability value movements and the asset value movements.

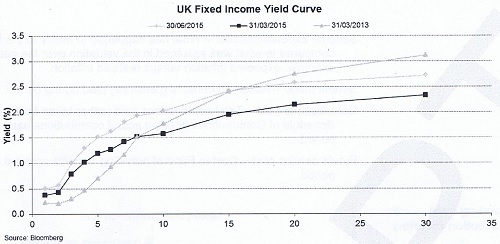

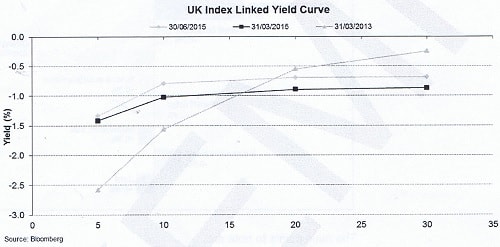

The liabilities increased in value significantly between 31 March 2011 and 31 December 2012, mainly due to falling gilt yields. For a year following the 31 March 2013 valuation, the present value of calculated liabilities reduced, when the prospect of tapering (a reduction of quantitative easing) caused gilt yields to rise. However, in the second half of 2014 this reversed, as gilt yields moved dramatically lower due to the falling oil price and uncertainty in Europe, resulting in the present value of liabilities rising above 31 March 2013 valuation levels.

While asset performance has been strong, the movement in the value of the liabilities has resulted in a volatile funding level.

The Fund’s assets reduced by c. 2.1% over the quarter, with all asset classes generating a negative return, with the exception of Property.

Gilt yields moved higher over the quarter, reducing the discounted present value of liabilities, as the sharp move up in German bond yields and mixed US economic data impacted the gilt market.

The changes in gilt yields since the last valuation and over the quarter are shown on the charts overleaf.

Progression of assets and liabilitiesUK Fixed Income Yield CurveUK Index Linked Yield Curve

Reasons behind the change in funding level

The chart overleaf decomposes the change in the funding level over the quarter across the various contributing factors. The contributing factors are:

Outperformance over benchmark — Approximate impact of any outperformance (underperformance) relative to the assets’ benchmark return.

Benchmark asset return – Approximate impact of the strategic benchmark return over period.

Interest on liabilities – Given that liabilities are due to be paid at fixed points in the future, as we move closer to the time of payment, these liabilities are discounted for one quarter less thus increasing their value (all other market conditions equal). The Fund must achieve this return to keep the funding level unchanged (everything else being equal).

Change in market conditions – Change in discount rate in this period due to changes in gilt yields and inflation expectations.

Scheme experience/other — What has happened in reality to the Fund compared to what was assumed in the valuation over the period. For example, expected inflation versus realised inflation.

Benefit outgo – Assumed benefits (pensions) paid during period.

Contributions paid – Total contributions paid (either taken from the Schedule of Contributions or using actual contributions paid) during period.

Future service cost — Cost to Fund of providing benefits accrued over period.

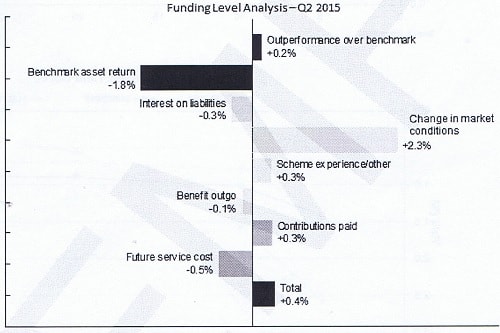

Funding level attribution (quarter)

Funding Level Analysis – Q2 2015

The main points to note are:

The overall effect of the strategic benchmark asset return was a negative impact on the funding level of 1.8%.

Outperformance by managers versus their benchmarks increased the funding level by 0.2%.

Interest accrued by rolling the liabilities forward over the quarter has reduced the funding level by 0.3%.

The majority of the liabilities are real (or index linked) in nature and therefore changes in the real yield will have a large effect. The result of a continued fall in yields over the quarter is shown by a 2.3% increase in the funding level. This is called the "change in market conditions".

Contributions paid resulted in an improvement of 0.3% in the funding level. Benefit payments and future service costs reduced the funding level over the period by a further 0.1% and 0.5% respectively.

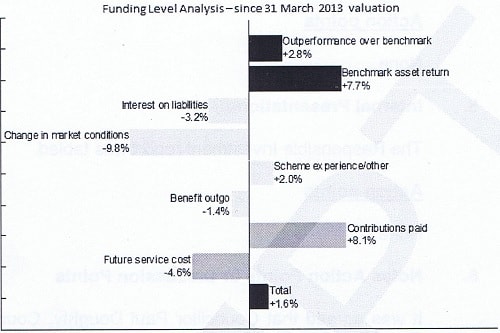

Funding level attribution (since 2013 valuation)

Funding Level Analysis – since 31 March 2013 valuation

The main points to note are:

The Fund’s assets and investment managers have performed strongly since the valuation.

Interest accrued by rolling the liabilities forward has reduced the funding level although the major negative impact on funding level has come from changes in the market conditions (falling gilt yields).

Contributions paid resulted in a large improvement including the lump sum paid in Q2 2014 with benefit payments and future service costs reducing the funding level.

Action points

None.

4.4 Valuation and Performance Summary including Monitoring Report

LO reported on the monitoring reported quarter 2 and noted there were some minor differences in figures produced due to reconciliation issues.

The valuation of the fund as at 30 June 2015 stood at £6.6bn and ahead of its benchmark by 0.19% returning -2.07% against the benchmark of -2.26%. The performance of the mandates was looked at to 30 June 2015. The performance of the majority of external managers has been good but M&G Recovery and M&G EM Equity continue to lag and are being monitored by the Fund.

Amundi and Legal & General Active Fixed Income continue to be on Watch status.

Action points

None.

5. Internal Presentations

The Responsible Investment report was tabled.

Action points

None.

6. Notes Action Points or Discussion Points

It was agreed that Councillor Paul Doughty, Councillor Treena Johnson, Councillor Pat Cleary and Councillor John Fulham would make up the Task & Finish Group to review the status of ethical investments and to coordinate a public message. EJ to arrange a suitable date.

An extraordinary meeting of Pensions Committee has been arranged for the 28 September 2015 to gain approval of the Annual Report.

Action points

None.

6.1 Noting items

Task & Finish Group to meet.

Extraordinary meeting of Pensions Committee 28 September 2015.

6.2 Action points

EJ to arrange suitable date of Task & Finish Group.

6.3 Summary of Recommendations

None.

6.4 Discussion Points (including any other business)

None.

5.1 Action Points

None.

Date of Next Meeting

Thursday 8 October 2015 at 10.00 am, 6th floor, Cunard Building.

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.

What’s happened on the 6th floor of Wirral Council’s Chamber of Secrets for it to sue for over £300,000?

What’s happened on the 6th floor of Wirral Council’s Chamber of Secrets for it to sue for over £300,000?

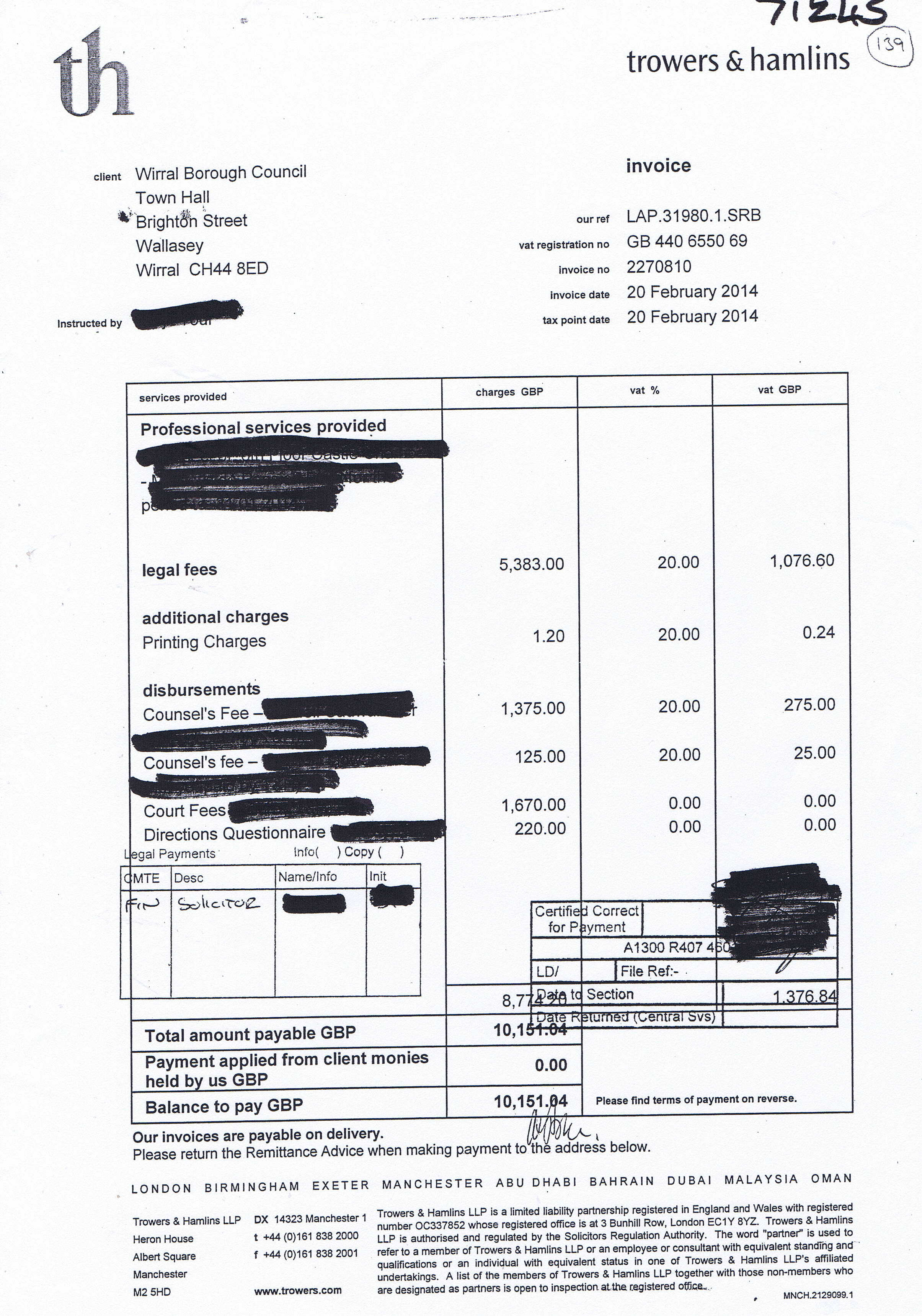

Last year I requested various legal invoices during the 2013/14 audit of Wirral Council. One of these is below:

Wirral Council invoice Trowers & Hamlins £10,151.04 20th February 2014

The invoice above is from Trowers & Hamlins and is for work connected to a court case to do with the 6th floor of Castle Chambers (a building owned and rented out by the Merseyside Pension Fund which is part of Wirral Council).

The court fee of £1,670 means this invoice is to do with to a civil court case in the High Court (in which Wirral Council is the claimant) to recover a sum of money where the amount exceeds £300,000 or an amount that is not limited.

What is blacked out under the heading Professional services provided appears to end in “6th floor Castle Chambers – Merseyside Pension Fund for the period to 31 01 2014”

So why all the secrecy surrounding the 6th floor at Castle Chambers? What was the outcome of the case and did the expenditure of £10,151.04 with Trowers & Hamlins lead to Wirral Council recovering any money?

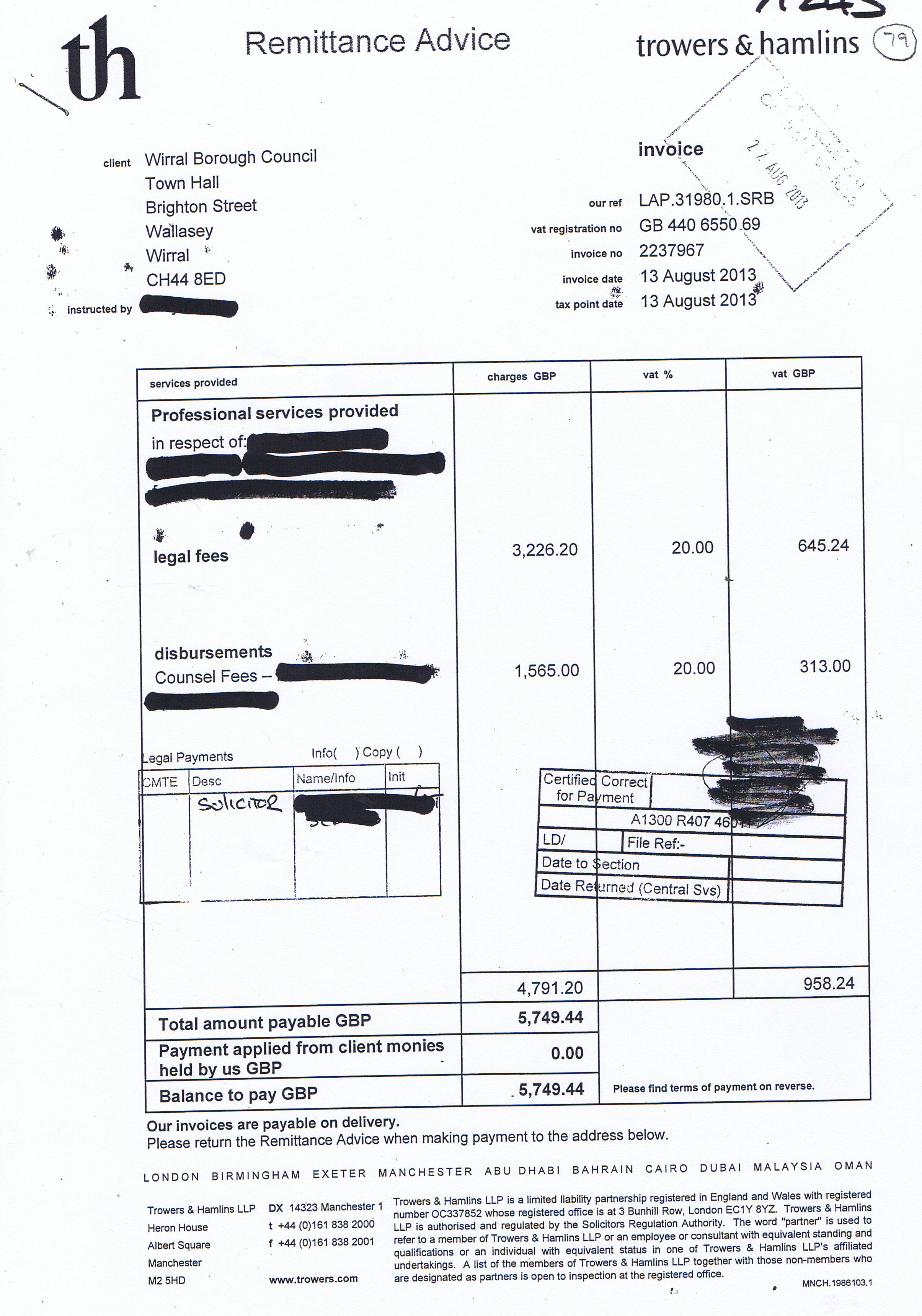

Below is an earlier invoice about the same matter for £5,749.44.

Wirral Council invoice Trowers and Hamlins £5,749.44 13th August 2013

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks: