EXCLUSIVE: Wirral Council continues its multi year battle to keep the 320,000+ Wirral people and press completely in the dark on councillors’ expense claims but in an exclusive you can now read 44 pages of the taxi contract for councillors

Updated: 16:56 7th October 2015: 3 minutes after this blog post was published Wirral Council got in touch about my request under the The Re-use of Public Sector Information Regulations 2015. Wirral Council asked for more time to reach a decision (which seems to be on line one page one of their big book of responses. 😉

However I have written back (and carbon copied in Surjit Tour) explaining that Regulation 5(5) excludes such documents because in order to access them I had to prove a legal interest (in this case being a local government elector for the Wirral area) during the 2014/15 audit.

This does mean that as this matter has been resolved, I will be publishing more information unearthed during the audit in the future, such as the Bam Nuttall contract.

Those who pay close attention to this blog will realise I haven’t published anything on this blog for a week. Apologies for that and here is an explanation. For some of that time I wasn’t well and the combination of nights of disrupted sleep due to dogs barking outside/helicopters/extremely noisy weather*(*take your pick as that’s just one night) resulted in severe lack of sleep that made me feel so ill that the last thing I wanted to do is write (and believe me I have to feel very ill not to want to write).

The closest I can describe it to is like suffering from something like jet lag from sleep deprivation (which didn’t help me get better as quickly as I should and had the opposite effect). So apologies if I have either been slow (or not responding at all) to emails and comments. I just haven’t been particularly up to the art of stringing together words into real sentences as typing and actually using my joints to type just made the pain worse. So if I’ve written any emails to you over the past week or so where I seem unusually cranky or cheesed off hopefully this explains why.

However I was better yesterday but was busy doing writing of a different sort, which forms part of what I’m going to write about today.

This blog post is a new chapter in a long running saga about taxis, Wirral Council and secret expenses system. However the story has got far wider than that.

First, before I get into fourth gear of what is a story that seems to now have more interesting angles than the Watergate affair and as this blog is read in many countries around the world I need to explain.

For reasons far too complex to go into here, Wirral Council tends to go in for similar types of high political drama that surrounded the Watergate affair, except people very, very rarely resign (resigning being a once in a blue moon event at Wirral Council that tends to really take people by surprise). This was summed up by the attitude of the former Improvement Board at a public meeting who I will paraphrase here, no one is ever held personally accountable and you mustn’t name names (as if you name names that’s blaming people)! My own personal political philosophy is there are always matters people are personally accountable for, but organisational failings of checks and balances and abuses of power have more serious outcomes for society as a whole than people (or even groups of people) behaving badly. However I digress and I need to briefly summarise the story so far as this is starting to have echoes of the MP expenses scandal. In fact not just echoes but marked similarities.

Wirral Council (official long name the Metropolitan Borough of Wirral) has sixty-six councillors (for foreign readers unfamiliar with the word councillor it’s a form of politician). Nearly every year the people who get to vote on the Wirral (Wirral’s population was estimated at 320,295 in mid-2013 according to the Office for National Statistics) get to choose a candidate. The candidate with the most votes (and I’ll leave out a long argument as to why the First Past the Post system that is used for this is unfair and the merits of STV [single transferable vote] for another day) becomes a politician called a councillor. The person who is elected (unless it’s in a by-election) is then elected and called a councillor generally for a four-year term of office.

During their term of office they receive allowances, but there is also an expenses system too. Under our "democracy" (although technically the United Kingdom is a constitutional monarchy) politicians such as councillors are answerable to the people.

Many politicians stand for re-election (there are no term limits for being a councillor so for some people it can become a "job for life" (however as councillors on Wirral Council are not employees and not MPs (Members of Parliament) they don’t get a gold-plated pension)) so if you’ve been a bad sort of politician and stand for re election (or if you’re a good politician but are very bad at actually communicating this to the public and/or your political party does bad things) you’ll lose your seat. This is the greatest form of accountability to the public.

During their term of office (on top of their generous allowances) councillors can claim expenses (or have expenses paid on their behalf) under a set of rules written into Wirral Council’s constitution called the Members Allowance Scheme (pages 329-338) of Wirral Council’s constitution. Members in local government jargon means councillors.

A law called The Local Authorities (Members’ Allowances) (England) Regulations 2003, SI 2003/1021 (later amended by the The Local Authorities (Members’ Allowances) (England) (Amendment) Regulations 2003, SI 2003/1692 and The Local Authorities (Members’ Allowances) (England) (Amendment) Regulations 2004 places various legal responsibilities on Wirral Council.

Wirral Council are legally required to keep a record of all payments made under the scheme (whether to councillors themselves or to third parties). These records are required to be "be available, at all reasonable times, for inspection and at no charge" to any local government elector for the Wirral area.

However the right to copies of such information is wider than that as under the regulations "any person" can request copies.

This is a bit of a laugh really, as it takes Wirral Council months merely to assemble such information on councillors (therefore strictly speaking the information isn’t available at all reasonable times for inspection breaching one of the regulations).

I am however taking about a thousand words so far and slightly digressing from the points I wanted to make (which wasn’t just about local government record keeping).

Another part of the regulations requires an annual list to be published by Wirral Council for each councillor for the total of allowances & expenses claimed by each councillor for the previous financial year. This way the public can see what councillors are personally receiving (or is being paid on their behalf to third parties) in relation to their duties. Some councillors chose to claim no expenses at all.

However it probably requires a certain amount of forensic accountancy to prove that the expenses lists as published by Wirral Council have been incorrect and they have been for many years.

I am now going to refer to why this happened and what Wirral Council needs to do to correct this and why despite it being pointed out to them they probably won’t bother as to Wirral Council getting things right seems to be too much effort and too expensive as the politicians decide on an annual revenue budget of hundreds of millions of pounds a year and large amounts of capital expenditure too.

At the moment the published expenses lists are only part of the story. Based on looking at a similar situation at Merseyside Fire and Rescue Authority, what the public are actually told about is probably only approximately 50% (or half for those who don’t understand percentages) of what is actually claimed in expenses.

It has become a party political issue which is illustrated by this quote from the Leader of Wirral Council Cllr Phil Davies in this Wirral Globe article earlier this year. Again members is referring to councillors (our members refers to the councillors who are part of the ruling Labour Group on Wirral Council).

Asked why only Labour councillors appeared on the list, Cllr Davies said: “The reality is that quite a lot of our members don’t have cars, so they need to use taxis to get to council meetings. If they had cars then they would be making a claim on council expenses for their car allowance, but they don’t. There are more Labour councillors who don’t have a car than those from other parties. These are legitimate claims within the budget of the council for elected members to allow them to do their jobs. Quite often taxis are the only form of transport they can use to get to their meetings.”

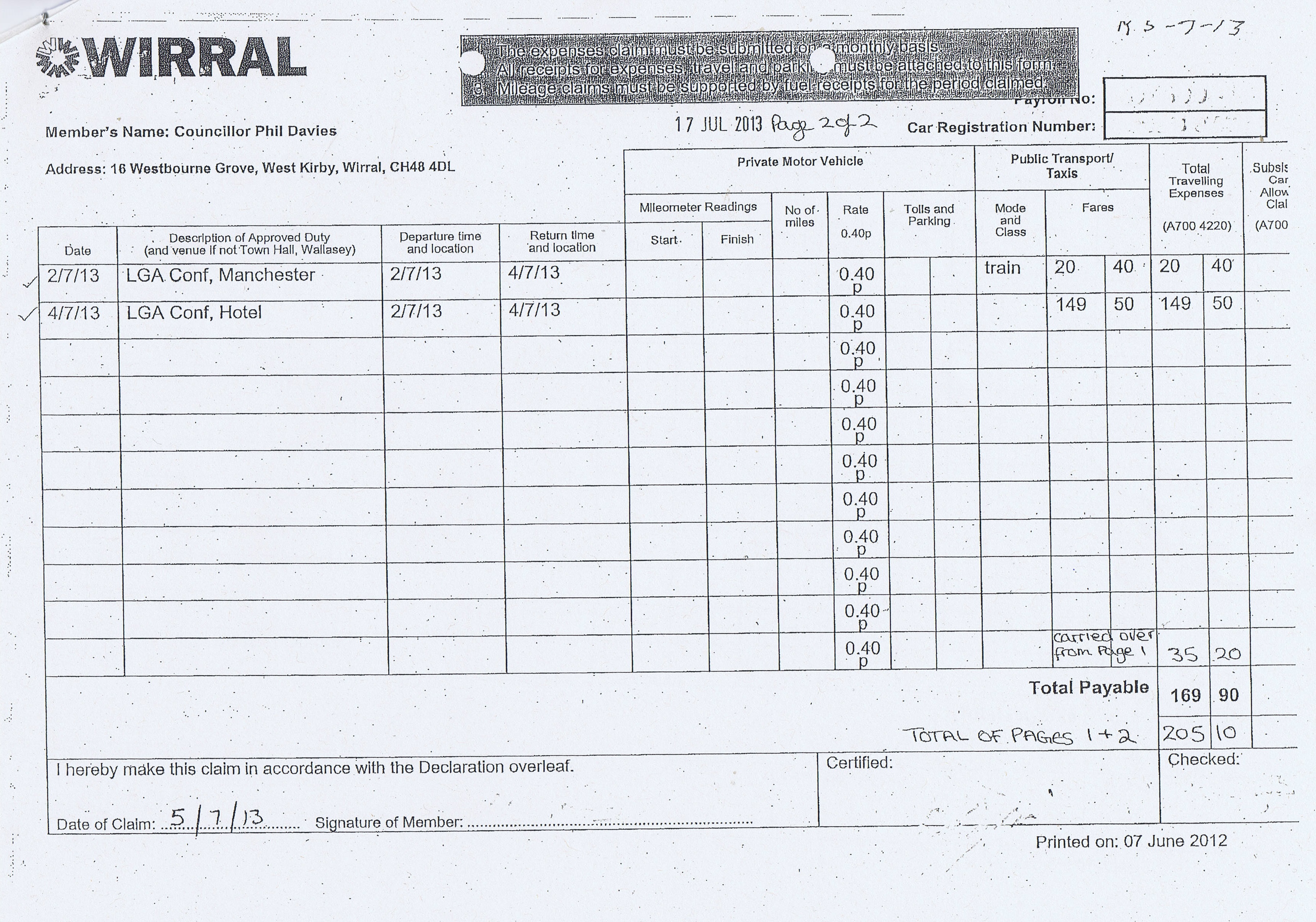

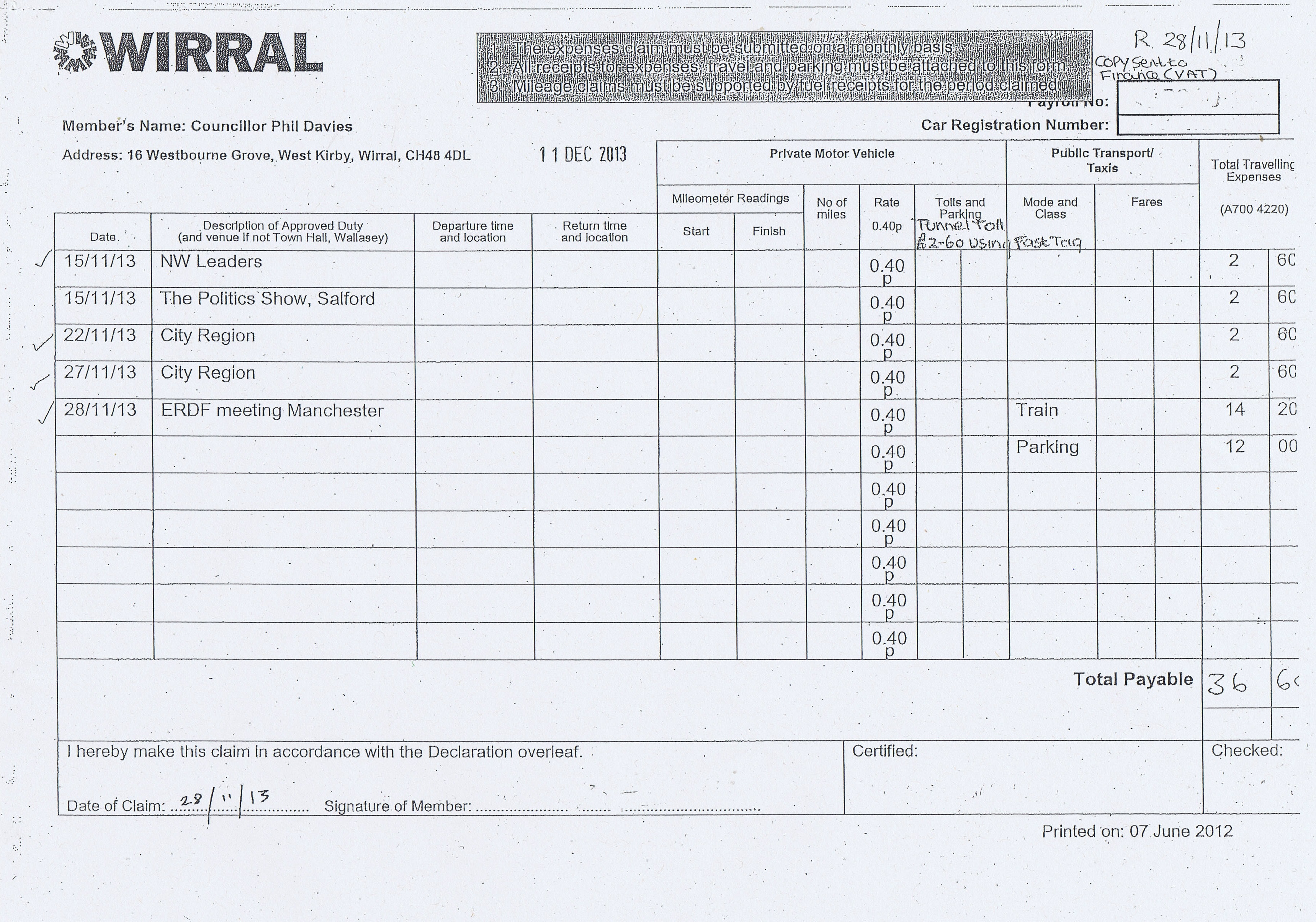

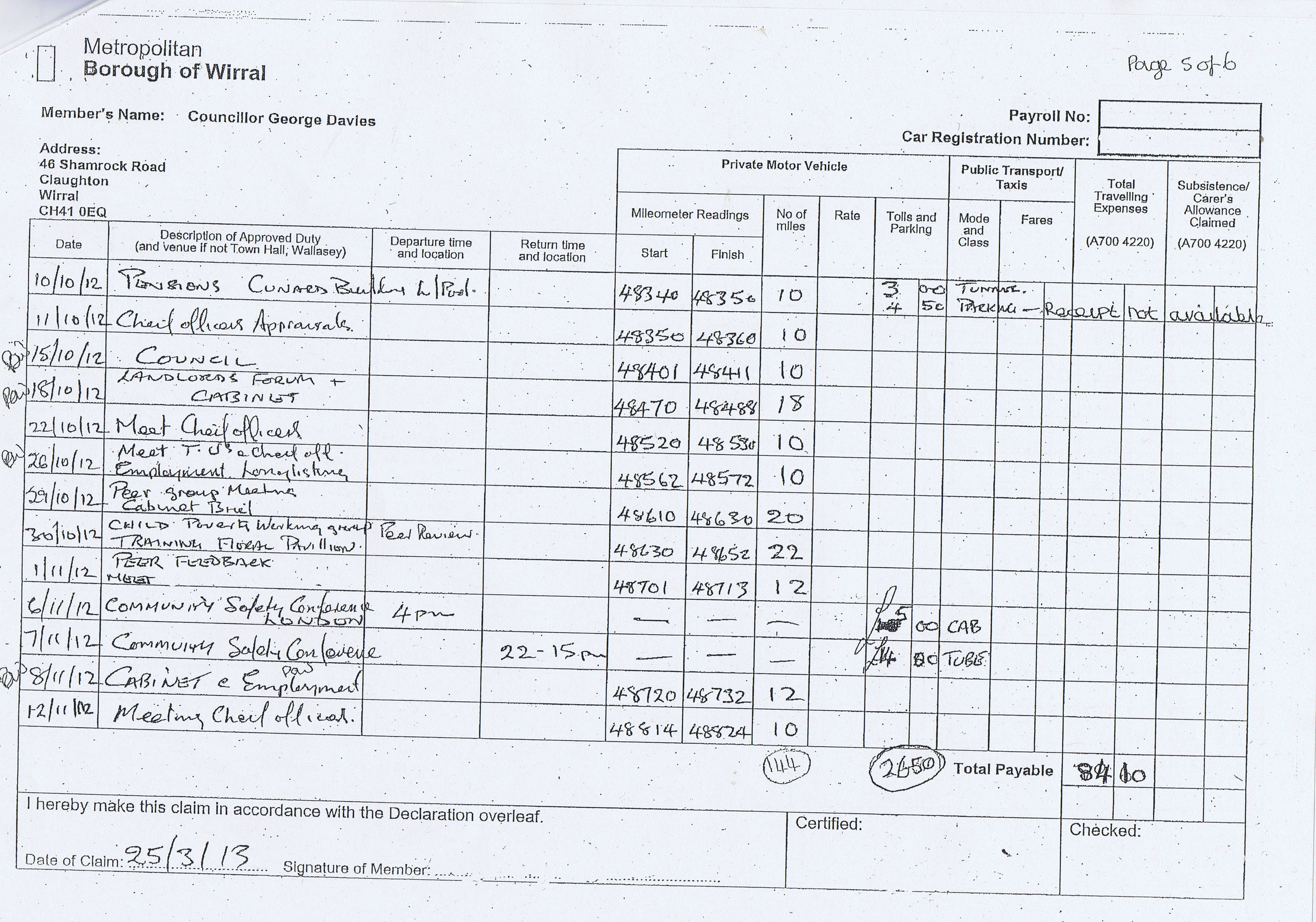

Apart from this having echoes of militant Labour delivering redundancy notices to all Liverpool City Council staff by taxi, basically this is a councillor (Leader of the Labour Group) somewhat begrudingly explaining about a secret expenses system for claiming taxis that the public and the press are presumably deliberately kept in the dark about. Wirral Council has known about this corporate governance matter about councillors expenses but despite claiming it would fix it has refused to do so. These figures for taxis (which come to £thousands) don’t appear in the annually published lists) and as detailed in the Wirral Globe article (based in part on my earlier story on the matter) that are used exclusively by one political party (Labour) are according to Cllr Phil Davies justified.

Cllr Phil Davies wears many hats, one as Leader of the Labour Group of councillors, one as Leader of Wirral Council (with the Cabinet portfolio for finance and corporate governance) and a third as a local councillor. The quote referred to above makes Cllr Phil Davies sound like a union rep for the other Labour councillors trying to keep hold of an expensive perk for his fellow politicians.

This has parallels with the approach by Michael Martin MP when he was Speaker of the House of Commons over the MP’s expenses scandal. Michael Martin MP saw himself as a representative of his fellow politicians and eventually had to resign because of the fallout over MP expenses when a national newspaper (in an example of chequebook journalism) bought and published the information. This ultimately led to a lot of embarrassment and prison sentences for some politicians (but ultimately reform of the system) whereas councillors at Wirral Council don’t even get the bare legal minimum of scrutiny of their expenses due to poor corporate governance (which is a matter that the person with democratic acccountability to the public is Cllr Phil Davies).

He compares Labour councillors’ use of taxis to a car mileage allowance used by other councillors. However the latter appears in the annual lists, but Labour’s use of taxis doesn’t. In order for the people to know what’s going on and compare one to the other they have to both appear.

I hope this doesn’t come across to people as an attack on Labour politicians or Labour Party, it’s not. If this was being done by Conservative, Lib Dem, Green Party or other sorts of politicians I would be writing this same sort of blog post.

However it reminds me of an email exchange I had before the General Election with a Labour Party member. They told me that they couldn’t campaign against their own party on an issue (I think it may have been about Lyndale School or possibly some other controversial issue) as instead their efforts were better put into getting Labour elected nationally into government in 2015.

Their view was once elected a Labour government in 2015 would have power and therefore be able to solve the policy problem. It was a stark example of how political parties may have individuals that care about policies, but ultimately as a group the Labour Party wasn’t interested in campaigning for something popular with the public (therefore winning votes and support) which may have ultimately led to them winning the 2015 General Election. This point was pointed out to them many times in the lead up to the election by the press and others.

Instead the Labour Party decided to pursue a strategy of ignoring public opinion, brazenly going for power at all costs, then got confused when the Conservatives got a majority and Labour lost seats.

I will point out that when I was a former member of the Lib Dems, there was a controversial joint Labour/Lib Dem policy decision to close half of Wirral’s libraries. I expressed my views against this in Lib Dem party meetings, stubborn councillors decided play brinkmanship, there was a public inquiry and the whole thing descended into farce and fiasco with a lot of people losing face over the whole matter. I even got ticked off by Sue Charteris as I unfortunately turned up about fifteen minutes late to the public inquiry (which was being filmed) and was told off for having the temerity to discreetly take a photo of what was going on (an omen of the later long running battles over filming public meetings).

At no point do I remember telling anyone within or outside the Lib Dem party (I decided to leave the Lib Dems in January 2012 and indeed sued the entire Liberal Democrat party for breaking the law, had my day in court and won), sorry I personally believe half of Wirral’s libraries shouldn’t close, but I refuse to campaign against the combined Labour & Lib Dem Parties as it’s important that I instead put my efforts into making sure the Lib Dems became the sole party of national government in 2015.

I think if I had made such claims fellow party members would’ve asked me if I was being sarcastic or not thinking straight. My position on the disastrous policy was well known, my views were dismissed partly because of my youth (one party member referred to me as a "baby" during a party meeting) although I doubt the full story about what happened internally within the Lib Dem Party over its politicians setting an unlawful budget will ever be told. The problem with that coalition is the buck could always be passed to Labour just as two halves of the recent 2010-2015 Coalition government could do with each other. The Lib Dem Party has always made it clear to me that they don’t care about the reputational consequences of its politicians or employees breaking the law. As obeying the "rule of law" is a part of democracy it makes me wonder how they have the gall to truthfully call themselves the Liberal Democrats.

However I am going off track in an explanation of the terrible policy failings of party politics and the errors of judgement of politicians (who seem to have a blind spot when it comes to abuses of power) that make unpopular decisions that are not only unlawful but not supported by their own political party either.

This article is going to be about the nuts and bolts of the Passenger Transport Contract issue though.

Last year, Wirral Council agreed to a one-year Passenger Transport Contract worth about £4.1 million. It’s possibly worth more than this as there’s an option in the contract for a one year extension. However I’m not sure if the £4.1 million figure relates to the one or two years of the contract.

This contract is with a company called Eyecab Limited based in Upton (Upton makes a lot of geographical sense for a taxi company to base itself as it’s in the middle of the Wirral).

The contract is divided up into four parts called lots. I’d better describe what each lot is about.

LOT 1

This lot is for transporting children with special educational needs and/or disability from home to school and school to home. It also covers transport for children in care. Children in care is a term that those involved in social work might be more familiar as looked after children. If you’re still not familiar with the term looked after children it refers to for example (but not exclusively) to those in foster care for whom Wirral Council is their "parent". It also covers transport for vulnerable adults to day centres.

LOT 2

Lot two is for ad hoc travel for children with special educational needs and/or disability, vulnerable adults and children in care by taxi, people carrier or hackney carriage (black cab).

LOT 3

The third lot is for journeys by taxi to work and training for Wirral residents (where journeys start or end in East Wirral) known as the "Maxi Taxi". This is to "support individuals travelling to locations not served by traditional public transport and too far or too unsafe to cycle to."

On that latter point, in my younger days I classed a 16 mile cycle ride as not too far and for many years regularly used to cycle a 7 mile round trip to work and back. I’m presuming the "too unsafe" comments are in relation to the rise in people killed and seriously injured on Wirral’s roads since that time. However as you can take the bike on a Merseyrail train (and most areas of Merseyside are within one mile of a train station). It is possible to use bike, train, bike as I did for many years as a university student and for work travelling all over Merseyside as the trains run from very early in the morning to very late in the evening.

LOT 4

I’ll just quote the official description for this lot. "This contract is for ad hoc journeys by taxi to allow Wirral Councillors to travel to various venues across Wirral.

This contract will allow Wirral Councillors to travel around Wirral on official Council business. The times will vary and may include evenings and weekends."

Much as I would happily write about the millions spent by Wirral Council on lots 1-3, effectively lot 4 is the focus of this piece.

During the audit I requested the contract with Eyecab Limited. I did this as I’m a local government elector for the Wirral area using Audit Commission Act 1998, s.15. I will add here that this is the last year I can do this as that right has now been repealed by the previous Tory/Lib Dem government.

It’s been replaced with a much more watered down right which has the following two major changes (amongst others).

(a) the safeguard of the independent auditor deciding what is personal information (not relating to officers) rather than the body itself and whether this can or can’t be redacted from information supplied has been removed,

(b) showing perhaps a Tory philosophy that will no doubt fill my Labour-leaning readers with glee as another example of government pandering to the sorts of commercial interests that make large donations to the Conservative Party, an extra category of withholding information on grounds of "commercial confidentiality" has been added.

I will point out that Wirral Council has withheld some information from the contract supplied to me. The phone number for Eyecab Limited is such a secret that presumably Wirral Council got permission from its auditors to withhold it.

When the phone number for Eyecab Limited is in the Yellow Pages as 0151 201 0000 (therefore hardly confidential after all please leave a comment if you ever heard of a taxi company that deliberately keeps its phone number a secret?), I do wonder why Wirral Council just make work for themselves (and me) in blacking such information out.

Other information that has been withheld has been pricing information and routes.

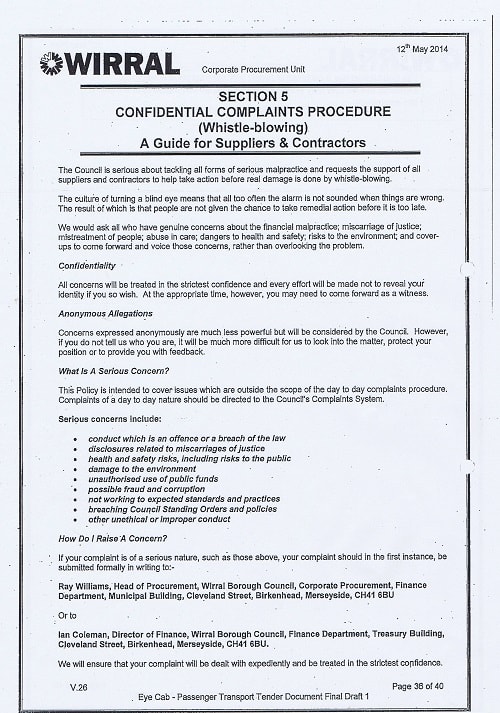

On the subject of Wirral Council and its well paid auditor Grant Thornton, when I complained to Grant Thornton about one of contacts to blow the whistle to (Ian Coleman on page 36) having received early retirement from Wirral Council two years before this contract even started, I got an email back stating that contracts weren’t to do with the accounts, therefore weren’t the auditors’ responsibility.

Auditors it seems such as Grant Thornton don’t know what they’re doing (maybe Wirral Council could ask for a refund of their fee when they get things wrong) so they just seem to spout nonsense like this in an attempt to fob people off.

As nobody is ever personally accountable in local government I will spare the particular auditor’s blushes by merely quoting from the email and my reply without naming names. It shows however that some auditors in my opinion are about as much use as a chocolate fireguard (a general point aimed at the entire accounting profession rather than this particular auditor).

I think the term is fobbing off as from other bloggers I know that auditors up and down the country are trying to evade their responsibilities in law by giving this sort of reply to local government electors. The likes of Cllr Ron Abbey (who I recently heard being critical of local government electors exercising their rights with auditors at a Merseytravel meeting because of the cost) would probably not approve of me teaching an auditor they’re wrong as the cost of this (in the form of increased external audit costs) is falling on the taxpayer (whereas sadly my advice and grumpiness is not something I can charge them for).

"Dear Mr Brace

I have now had an opportunity consider the contents of your email to me of 6 September 2015.

I understand from your email that you have exercised your rights under the Audit Commission Act to inspect certain documents associated with Wirral Council’s accounts for 2014/15, including a Passenger Transport Contract with a specific contractor named in your email. You highlight that page 36 of the contract identifies the individuals who should be written to in the event of a whistleblowing complaint. The second of these names is the former Director of Finance who left the council 2012. You have asked us to explain why someone who ‘was not an employee of Wirral Council at the time the Passenger Transport Contract was put out to tender (or when the contract was agreed) … was he included as a whistleblowing contact in the contract?’

I have carefully considered this matter and I am not sure this is a valid question that it is appropriate for us to answer. As you highlight the power to question the auditor is set in section 15(2) of the Audit Commission Act 1998. Although interested persons can ask questions of the auditor, the questions must be about items in the Council’s account. It seems to me that your question is not about an item of account and therefore we are not in a position to respond to your question. It seems to me that your question is more appropriately addressed to the Council.

In summary, I would suggest that you contact the Council with your specific request for information.

It is currently our intention to close the audit of the Council’s 2014/15 accounts by 30 September 2015.

I hope that is helpful in clarifying the position.

Yours sincerely"

I however have learnt the art of being concise in emails and played this game of re educating the external auditor in the trump suit of 3 High Court Judges. Here is one of my replies (which meant the auditor had to change their mind).

Dear all,

I would also like to point out that a Court of Appeal case established beyond a doubt that contracts are part of the accounts. See [2010] EWCA Civ 1214 .

So as three High Court Judges seem to agree with my interpretation, I would ask you to reconsider..

Thanks,

John Brace

As you would probably say in tennis, game, set and match to me (not that I’m competing with an auditor, it’s just well whether deliberately or by accident they don’t really seem to know what they’re actually doing or the legal framework within which they operate properly but what’s new eh?).

However if I wanted to blow the whistle on the contract about taxis for councillors (and there are many reasons why one should), the contract suggests I blow the whistle to a person who was granted early retirement by Wirral Council in 2012.

Bear in mind this contract isn’t just about councillors and their taxi journeys. It’s also about children with disabilities & vulnerable adults. It is possible a family member might have cause for concern that they wish to raise. If so they could be directed to a person who doesn’t even work for Wirral Council.

Back however to lot 4 and taxis for councillors. As a reward for having to read through nearly 3,000 words of my ranting about poor corporate governance, I have a reward for you dear reader but I want to first explain the price at which publication of this contract comes.

First I had to request it during the audit. Wirral Council exceeded the time limits set down in law for giving it to me so I had to wait a bit longer. I then had to travel for a meeting at a Wirral Council building just off Hamilton Square to inspect it and pick up a copy.

It comes to 43 pages (even after the information has been removed I referred to earlier). I then had to scan these pages in one at a time (because that’s the way my A3 scanner works). I made a request to Wirral Council under The Re-use of Public Sector Information Regulations 2015 to publish it.

Despite this request being made some time ago, I have not received a response back from Wirral Council. As my communications to Wirral Council often seem to disappear into if I was being charitable what must be a black hole operating in one of its departments that sucks up my emails, I’m having to use my editorial discretion to use the part of the Copyright, Designs and Patents Act 1998, s.30 that deals with criticism, review and news reporting. I’m also covered bythe Data Protection Act 1998, s.34 in that its been made available to the public (myself) therefore isn’t subject to the non-disclosure provisions of the data protection legislation.

The way I have digitised this contract was by taking the 73 image files, putting them in OpenOffice Writer one at a time and creating a PDF file. However this file (as each page is an image) comes to 124 megabytes. As Wirral Council raided a reserve for high speed internet access some time ago, not only would this use up a lot of space but peoples’ internet speeds would mean it would take a long time to download.

I therefore spent one work day (yesterday) initially typing up the contract only using images for those that needed it (a MaxiTaxi logo and some signatures). This is very boring and time consuming work, but part way through I found a way to speed things up dramatically by putting the multi-page pdf file through FreeOCR.

The problem was as you can see from my earlier post about page 36 is that the pages given to me by Wirral Council were in a very poor state with many artifacts (a technical term for blemishes on the page). The artifacts cause massive problems for OCR as OCR software can try and guess what they are (for example a full stop).

The versions of the contract I finally ended up with are far easier to read than the version provided to me by Wirral Council. For those with disabilities, the text can now be magnified without just blowing up the blemishes too. The file sizes of the new files (and I’m providing it in multiple versions because I’m trying to be helpful) are massively smaller.

I have not included the Wirral Council logos and replaced these with (Wirral Council logo). As you can see from the image above it’s the five Ws logo with WIRRAL in bold letters. The typographical errors in the contract (such as the many instances of Disclosure and Baring (rather than Barring) Service), missing full stops etc I’ve left in and not corrected. I hope people appreciate the work put into producing it and I realise it has probably been hard work reading through over 3,000 words to reach this point.

A bit like Schrödinger’s cat, although I requested this contract and the what must be about ~6 monthly invoices that relate to it during the audit, I can only at this point in time observe one (the contract).

Wirral Council are still stalling me on inspecting and receiving copies of the monthly invoices for councillors journeys by taxis. Anyone would think that Wirral Council hasn’t quite got the staff to deal with the sort of investigative journalism I tend to be good at. However as the taxi contract is used solely by the ruling Labour Group councillors I can see how it would be in no officers’ interests to actually comply with the legal deadline for this as no doubt I would publish them which would cause politicians to be embarrassed. Wirral Council are &improving& their website, the legal notice they’re required to publish on their website with the deadline on has also vanished at the time of writing.

Certainly I await to see what other corporate governance horrors Wirral Council get up to and will (hopefully) keep readers of this blog advised of what’s happening. In the meantime at the end are the pages of contract information.

This does raise a lot of questions but I will just concentrate on one which seems to demolish one of the reasons given for this contract. When Councillor Adrian Jones read out an answer to me prepared for him by officers at a public meeting as reported previously he stated, "The Council has negotiated competitive prices and entered into contracts with a local taxi company to provide transport for Members in accordance with the Members Allowances Scheme. The taxi company submits its invoices and the details of the Members that used the taxis each month directly to the Council for payment. The advantage of this arrangement is that the cost of transport by taxis is always at the negotiated rate and is a more efficient way to manage the service."

It does raise an interesting point though as the pricing information for councillors’ journeys by taxi are included. In the method statement that Eyecab Limited completed when bidding for lot 4 (councillors’ taxi journeys) Eyecab Limited stated on page 34 of 40 "Eye Cab is an all Hackney taxi firm vehicles range from five passenger seats to seven passenger seats at present we operate approximately twenty seven vehicles this number is increasing on a regular basis."

When I heard Cllr Jones’ answer about "competitive prices" anyone hearing it would think that it was stating that taxis through this contract are better value for money (in terms of the actual cost of the taxi ride) than a councillor paying for it themselves, then claiming the money back.

However having read the contract and that I know now that Eyecab Limited is an all hackney carriage company, I’m puzzled. That’s because the prices at which all hackney carriages on Wirral charge is set by Wirral Council. Therefore for the same journey surely all hackney carriages would charge the same amount and it wouldn’t be cheaper doing it through a contract. When you factor in the costs of putting this contract out to tender (yes I realise lot 4 is part of a wider contract however potential contractors had to bid on each lot separately), the costs of procurement will outweigh any efficiency saving from just having to pay a monthly invoice rather than when councillors claim on an ad hoc basis.

A small saving does occur because Wirral Council isn’t actually doing it legally and including these amounts in the annual lists but by small saving I’m talking about an employee cost time of maybe £50-£60.

However by not doing it that way it increases costs elsewhere at Wirral Council, for example the cost of processing FOI requests, providing me with a redacted copy of the contract during the audit, providing me (hopefully eventually) with the underlying invoices etc and of course the expensive cost in senior officer time (probably an employee on ~£80 an hour) in having to answer questions posed by me to Councillor Adrian Jones at a public meeting.

The point I will finish on is that Wirral Council doing things the right way and legal way saves money in the long run in the communications you get from people trying to persuade Wirral Council just to do things the right way.

However officers across local government (in fact some have even said this to my face) see this sort of press scrutiny as a drain on "scarce resources".

In other words, the kind of major embarrassing politically sensitive fiascos (politicians’ expenses just being the tip of an absolutely massive corporate governance iceberg) I write about on my blog probably cause no end of awkward questions behind the scenes from politicians to those on high 5 figure and 6 figure salaries as to why things aren’t right.

I’m sure some people paid by the taxpayer well above my pay grade don’t always see the sort of journalism as a good thing for their future career prospects. I’m pointing out things to the world that if the checks and balances that these employees are supposed to be were working properly would be spotted internally and corrected.

Some bureaucrats (while stating they welcome accountability) I’m sure don’t really feel it’s right that they should be under a legal requirement to hand over embarrassing information to me, that’ll then form stories that politicians will read (or in the case of video watch) and use to hold the bureaucrats to account.

It’s the way I’ve been trained though and the independence of the press is something that this country should value.

Please note, although I proofread the contract before publishing due to the poor quality of the original pages at times the OCR program has misidentified one character incorrectly such as the postcode CH44 8ED, the OCR program has outputted as CH44 BED (page 23 of 40). The other errors (typographical such as baring for barring & punctuation such as missing full stops) were made in the original document.

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks: