What did a Government Internal Audit Agency draft report reveal about Wirral Council procurement processes and how a contractor spent public money?

What did a Government Internal Audit Agency draft report reveal about Wirral Council procurement processes and how a contractor spent public money?

Chris Whittingham (Grant Thornton) 29th January 2018 Audit and Risk Management Committee (Wirral Council)

“The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore, all progress depends on the unreasonable man.” – George Bernard Shaw

Whistleblowers assembled in Committee Room 1 to hear apologies from Wirral Council over a toxic whistleblowing saga involving secrecy, national, local and regional government, internal and external audit, the private sector, ££££s, senior managers, contracts and Wirral Council

Whistleblowers assembled in Committee Room 1 to hear apologies from Wirral Council over a toxic whistleblowing saga involving secrecy, national, local and regional government, internal and external audit, the private sector, ££££s, senior managers, contracts and Wirral Council

Nigel Hobro (standing) addresses the Audit and Risk Management Committee of Wirral Council 8th October 2014 L to R Cllr Adam Sykes, Cllr David Elderton, Andrew Mossop, Surjit Tour, Nigel Hobro (c) John Brace | still taken from video

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

Above is a playlist of all parts of the Audit and Risk Management Committee (Wirral Council) meeting of 8th October 2014 held in Committee Room 1, Wallasey Town Hall starting at 6.00pm (apologies for recording problems)

Audit and Risk Management Committee

Cllr Jim Crabtree (Chair, Labour)

Cllr Ron Abbey (Vice-Chair, Labour)

Cllr Paul Doughty (Labour)

Cllr Matthew Patrick (Labour)

Cllr John Hale (Conservative spokesperson)

Cllr Adam Sykes (Conservative)

Cllr David Elderton (Conservative)

Cllr Stuart Kelly (Lib Dem spokesperson)

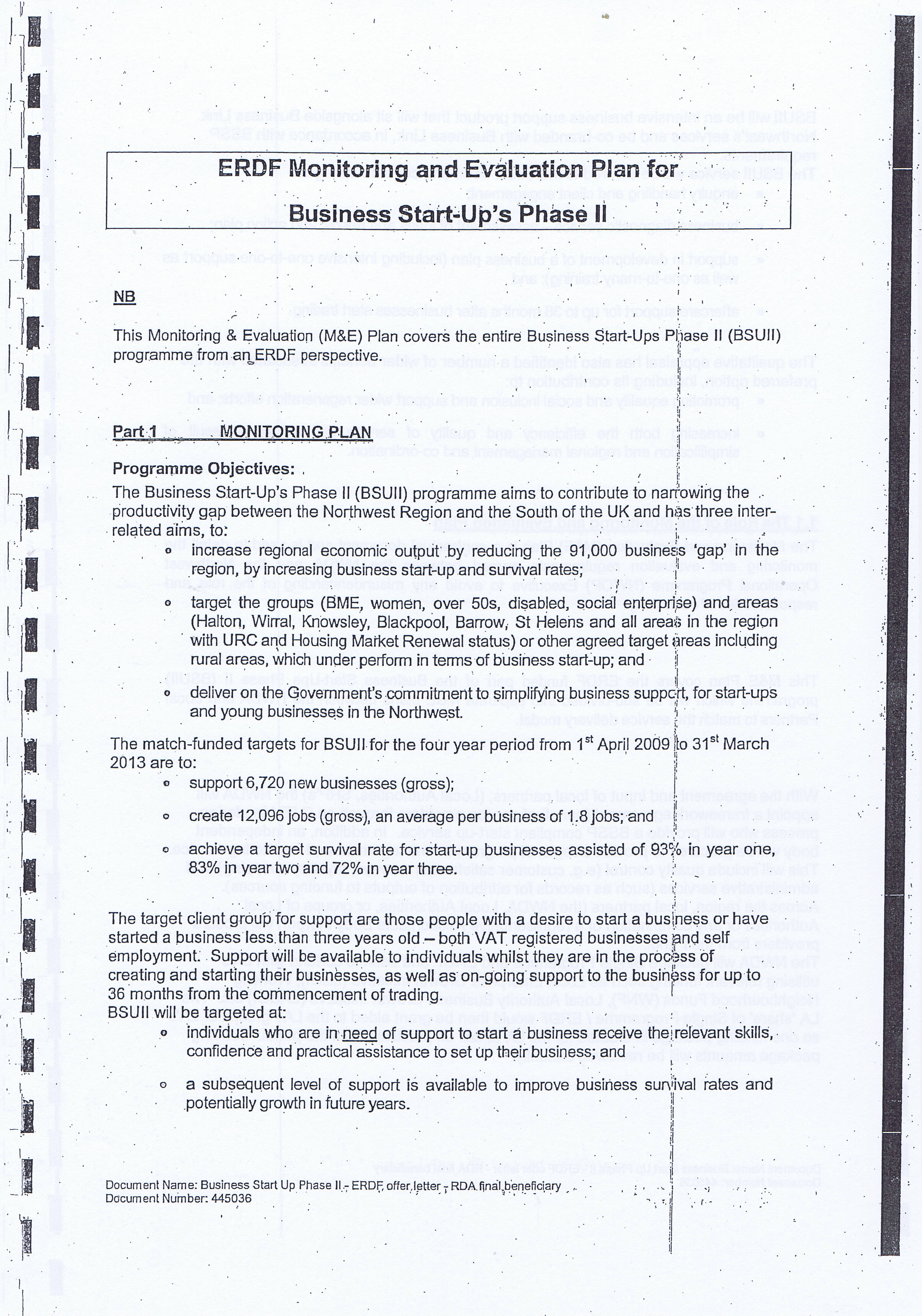

The Audit and Risk Management Committee of Wirral Council met for a special meeting about BIG/ISUS on the evening of 8th October 2014 whilst a thunderstorm raged outside Wallasey Town Hall. This was a continuing from its adjourned special meeting about the same topic on 22nd July 2014. For details of what happened at its meeting of the 22nd July 2014 see my earlier blog post Incredible first 5 minutes of Wirral Council councillors’ public meeting to discuss BIG & ISUS investigations.

The meeting started with a minute of silence for Mark Delap. Mark Delap was one of the Wirral Council employees that used to take minutes at its public meetings and had died recently.

After the minute of silence was over, the Chair asked for declarations of interest.

Cllr Matthew Patrick declared an interest due to a friendship with Nigel Hobro’s son (Nigel Hobro is one of the whistleblowers and spoke during the meeting itself).

Surjit Tour gave some brief advice to Cllr Matthew Patrick as to whether his interest was personal or prejudicial.

The Chair thanked Surjit Tour for the advice he had given to Cllr Matthew Patrick.

The Chair, Cllr Jim Crabtree then explained that there had been a lot of allegations since the issue had first been raised in 2011. There was a large volume of paperwork for the meeting, however details were redacted to protect businesses and companies. Also the names of officers and other people were blacked out. He also referred to commercial sensitivities and how they had gone to proper steps to protect identities.

He reminded people of the risk of legal challenge and Wirral Council’s liabilities. Cllr Crabtree asked everyone not to name names and continued by saying that any issues Wirral Council officers had addressed, they had done on behalf of the Council.

Cllr Stuart Kelly asked a question on the information that was redacted. He referred to a challenge to paragraph j, that was redacted in the papers to the July meeting, but was now provided. He wanted assurance from the legal officer Surjit Tour that the redactions were only in the categories as just outlined by the Chair.

Mr. Tour explained that the redactions had taken place to make sure that nobody by reasonable inquiry and information already in the public domain could piece together who or what the redacted information referred to and who the people redacted were. He added that in some cases it was unfortunately necessary to redact a lot of information mindful of what was already in the public domain, people could “fill in the gaps” which would expose Wirral Council to a liability.

The Chair invited Nigel Hobro to speak for at most fifteen minutes.

To be continued…

However below are some of my personal observations about this meeting I’ve started writing up above and a bit of a compare and contrast with two different special meetings of the Audit and Risk Management Committee held years apart (but both dealing with Wirral Council’s response to whistleblowers (one internal, one external).

It shows how history has a habit of endlessly repeating itself and is based on my opinion as one of the few people who was actually present at both meetings.

There are similarities between this public meeting and an earlier public meeting many years ago of the Audit and Risk Management Committee to decide on a response to the whistleblowing of former Wirral Council employee Martin Morton. Back then (years ago) there were arguments by politicians over a series of meetings over how much money should be paid back to those that were overcharged and to what year you go back to with the refunds.

Even when refunds were agreed by politicians, Wirral Council took so long that some of the people involved had died and in order cases (the ones that were still alive) the amounts were so large, that Wirral Council officers didn’t want to pay the people involved because they thought it would have a knock on effect on their benefits and officers doubted that some of the people had the capacity to be able to look after their own financial affairs.

Sadly the decision back then was fudged (which is partly what led to the problems later). Martin Morton’s concerns were also far, far wider than the overcharging issue, his concerns also involved allegations of the misuse of public money to fund organisations with links to serious and organised crime, serious allegations of serious crimes against vulnerable people who had apparently at the time not been investigated thoroughly enough, woefully poor corporate governance at Wirral Council, terribly weak political oversight due to put it frankly chaos back then and ultimately Mr Morton paid a personal price because people in Wirral Council tried to repeatedly punish him for daring to blow the whistle. Due to the large financial amounts involved, Cabinet had to sign off on the large expenditure that resulted.

One day before the AKA report was finally released to the public, the two middle managers involved in this matter were each paid a six figure sum each to leave Wirral Council.

At the earlier meeting (and at least one person on the Audit and Risk Management Committee is the same person as back then), the Chair back then accused one politician (Cllr Ron Abbey) of either not reading the papers for the meeting as they were asking questions that were already answered there or of completely misunderstanding what they had read (if they had read them). At this time the Chair was of a different political party to the Labour councillor (Cllr Ron Abbey) & in the interests of impartiality (with absolutely no offence meant towards one of my local councillors Cllr Jim Crabtree) many other local authorities have an unwritten rule that the Chair of the Audit and Risk Management Committee is not from the same political party as the ruling administration to ensure independence.

Knowing Cllr Crabtree as I do, I know that even if a councillor stepped out of line at a meeting he was chairing, even if the councillor was from the same political party as he was, Cllr Crabtree’s personality is such that he would frankly realise that it’s in the “public interest” to hold his fellow councillors to account even if he would have to be careful how he did this in public.

After it seems part of the reasons why Labour got a small majority on Wirral Council is because councillors from that party woke up the news that the Wirral public expected them to hold other politicians to account in public even if these were other councillors from the same political party.

Bill Norman (who left in somewhat mysterious circumstances in 2012) was the legal adviser to that earlier Audit and Risk Committee meeting years ago, not Surjit Tour as it is now. The issue of blacking out all the names (and other details) in the published papers was addressed by Bill Norman then with broadly similar reasons given to those given by Mr. Tour many years later. However I will point out that the culture of legal practice is such that confidentiality, especially when it comes to active proceedings is extremely important to maintain!

At the time this written material authored by Mr. Morton included in the papers for the meeting was also redacted, so this aspect of whistleblowing hasn’t changed much at all over the years at Wirral Council.

Wirral Council, back then and as it seems now has a fear of being sued. Although if they were open and transparent wouldn’t Wirral Council welcome judicial oversight of their decisions as it would give Wirral Council the chance for someone independent to look at it and the opportunity to defend themselves in court if they had done nothing wrong?

Perhaps it’s unfair to say a fear of being sued, it’s a fear at Wirral Council of being sued and losing and the results that flow from that which could be a combination of large financial penalties (or other things) as well as the fact that court reporters such as myself or the publications they publish in can’t actually be sued under British law for court reporting as long as we comply with the few rules that apply as court reporting attracts absolute privilege. All court hearings whether public or private are recorded by the court on tape anyway and in theory transcripts can be ordered.

Some may say for a large local Council (covering a population of ~320,000), whilst obviously they have their own organisational reputation to consider, that they seem unduly concerned at times at reputation management (although this is also a preoccupation of political parties) rather than dealing with matters in an entirely open and transparent way. There is a blurry line between the individual reputations of senior managers and politicians on one hand and the organisational reputation of the organisations they are either employed by or are elected to represent the views of the public at.

Some of the reports that went to the most meeting the day before yesterday, have been the subject of previous articles by me and FOI requests.

You can read my FOI request (25/8/13) for the report on ISUS here, which was refused on 23/9/13 and refused at internal review on 24/10/13. That external audit report can be read as part of the committee’s papers (see agenda item 2 and the links from this page on Wirral Council’s website if you wish to do.

Had the responses to those FOI requests been forthcoming and Wirral Council provided the information within weeks a lot more would have been in the public domain before the July and October meetings in 2014 of the Audit and Risk Management Committee meetings. Wirral Council instead chose to rely on exemptions to suppress the information and knew I was unlikely to appeal to ICO, as if I had I’d probably still be waiting for a decision!

Excessive secrecy just makes the public and press suspect that there’s a deliberate cover up or Wirral Council has done something it’s ashamed or embarrassed about. Usually the answer is a little more complicated than a conspiracy.

The Merseyside police investigation (which resulted in no charges) was used as an excuse by Wirral Council to deny FOI requests, not just about the one Grant Thornton recommended was referred to the police, but information in general about the other aspects too.

Wirral Council was recommended by the forensic arm of its external auditors to refer one very minor matter to the police. Wirral Council did and this was then used this as an excuse to delay and prevent further scrutiny. The police response (and I summarise) was that based on what they were told that there was insufficient evidence to charge somebody (or somebodies) with a crime. Remember criminal charges require basically two elements, proof that the alleged crime occurred and also generally for most criminal matters mens rea (proof of a “guilty mind” too). The latter is often harder to prove than the former, which is why defendants sometimes plead not guilty in order to get a jury trial! As Wirral Council actually carries out criminal prosecutions through the Wirral Magistrates Courts, I’m sure someone there who is actually aware of these matters!

This article is getting rather long and at the two thousand word mark I am somewhat digressing into related matters, although obviously it is not as long as the papers for that meeting which come in at the length of a medium-sized novel!

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

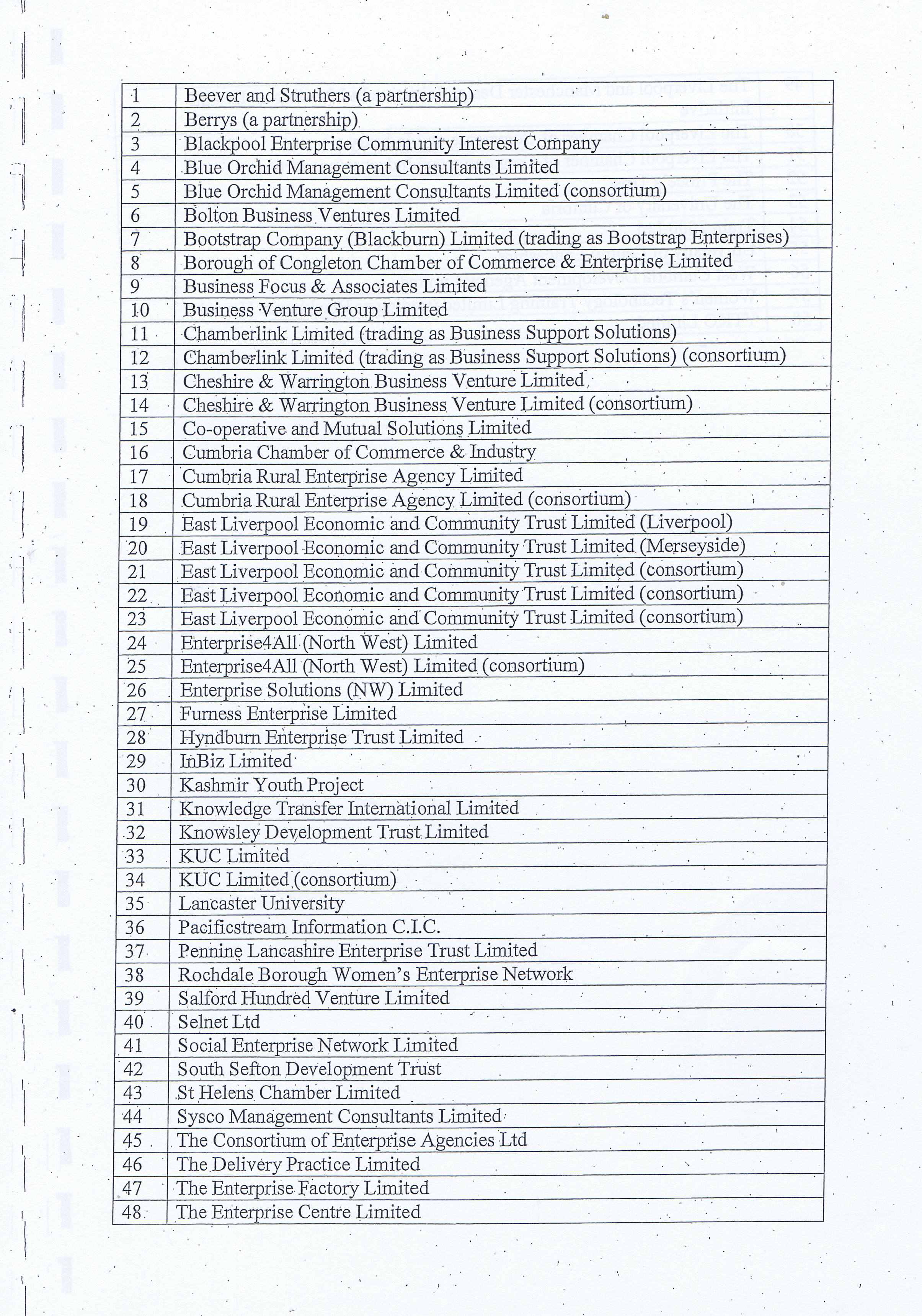

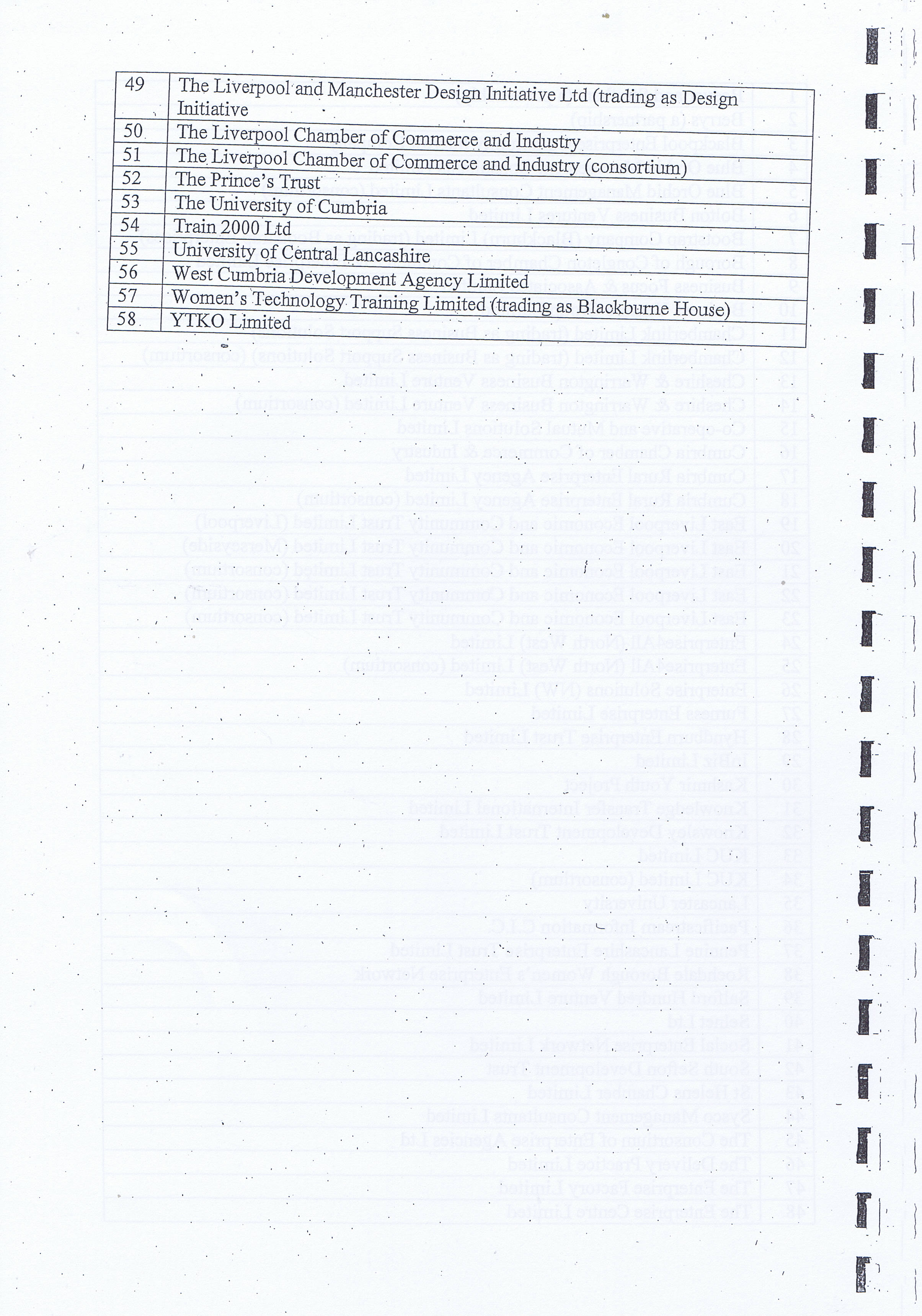

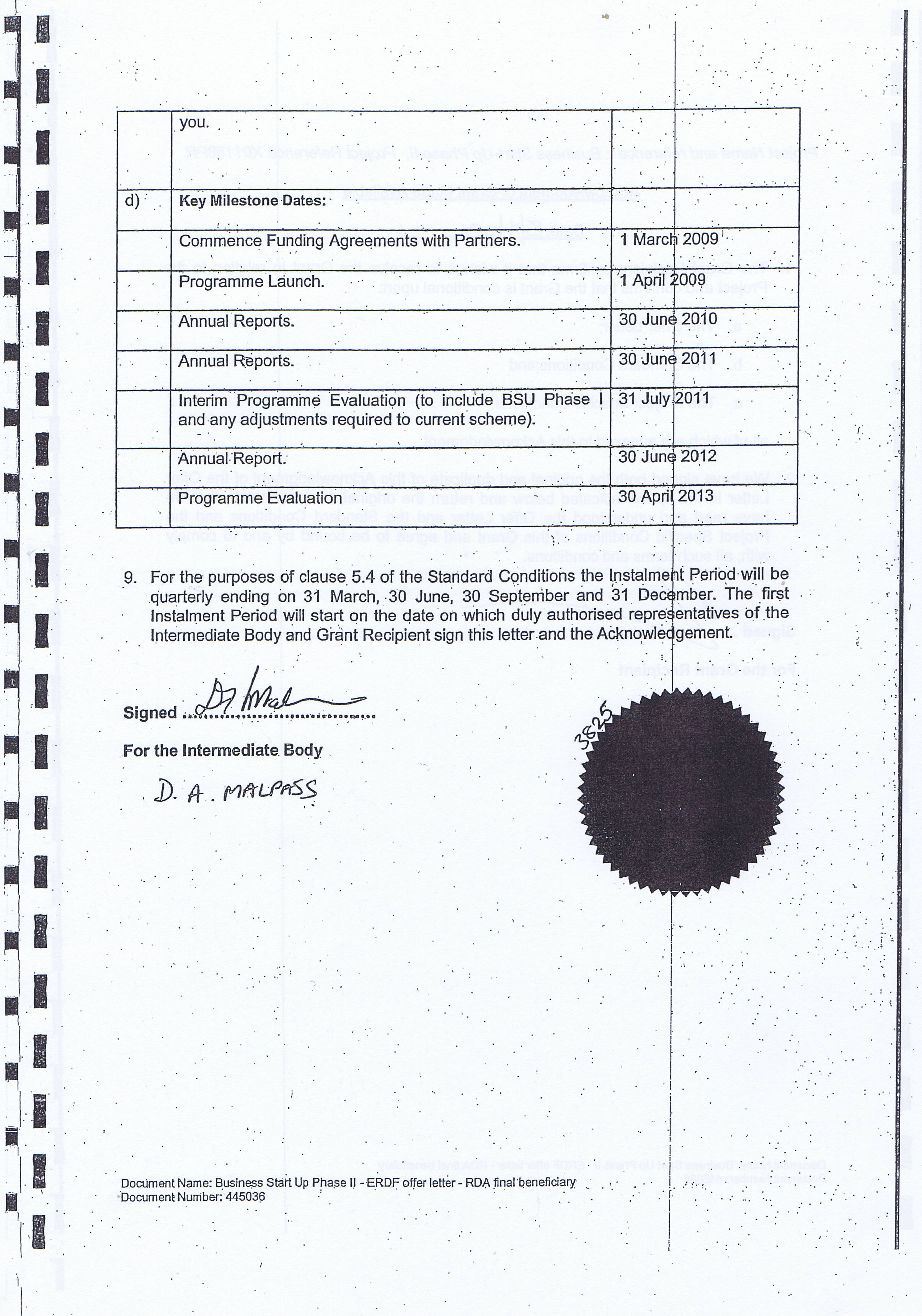

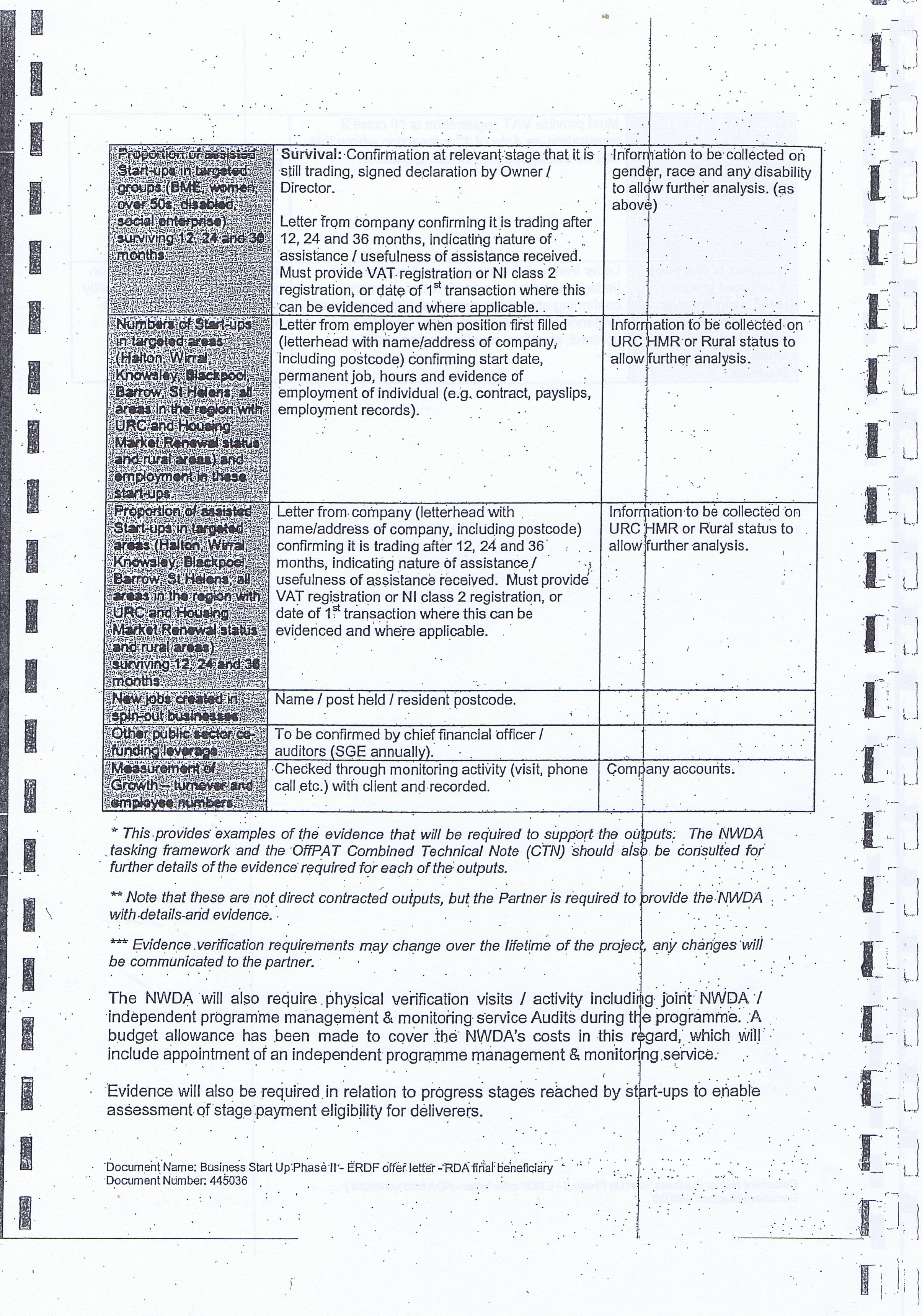

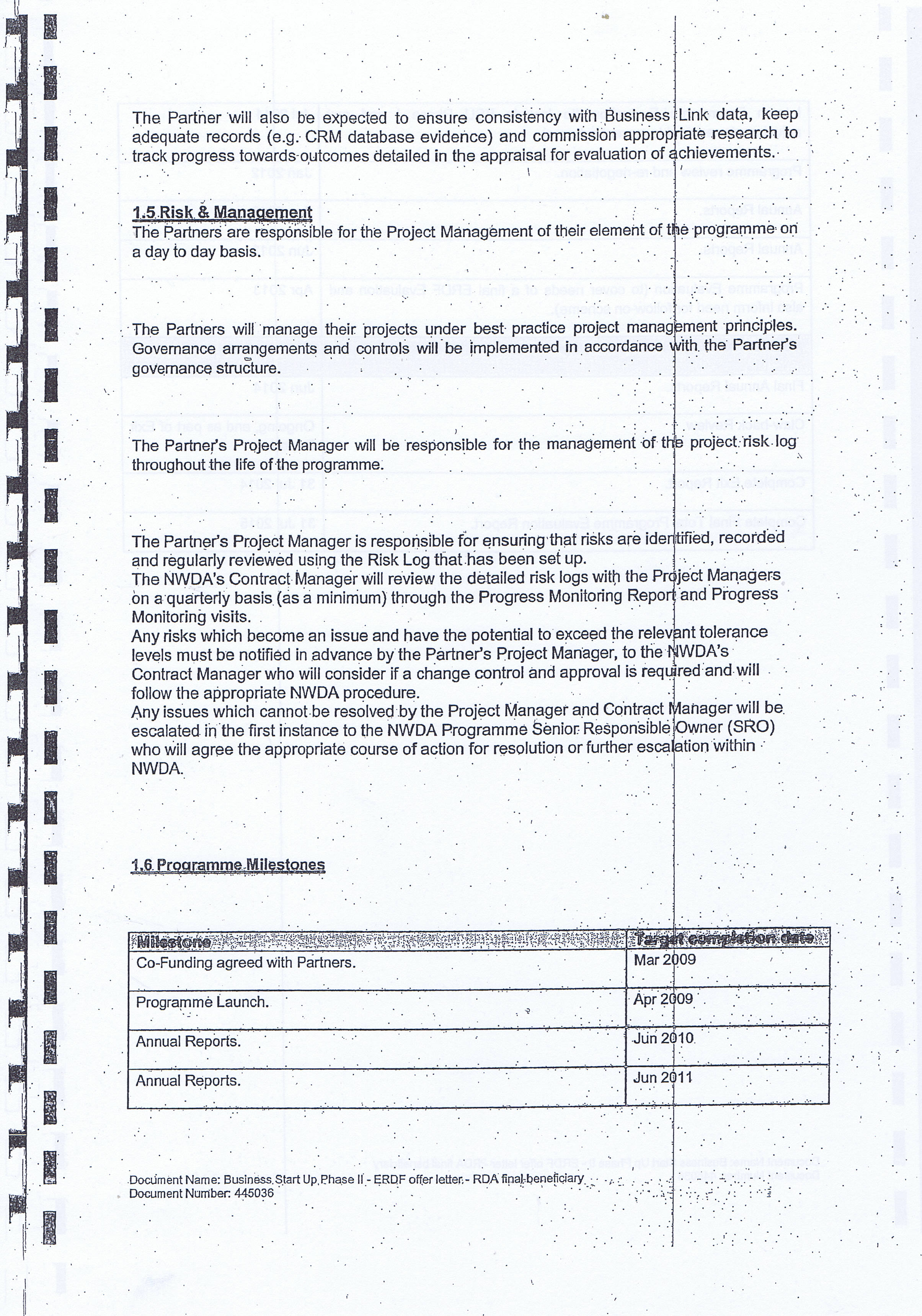

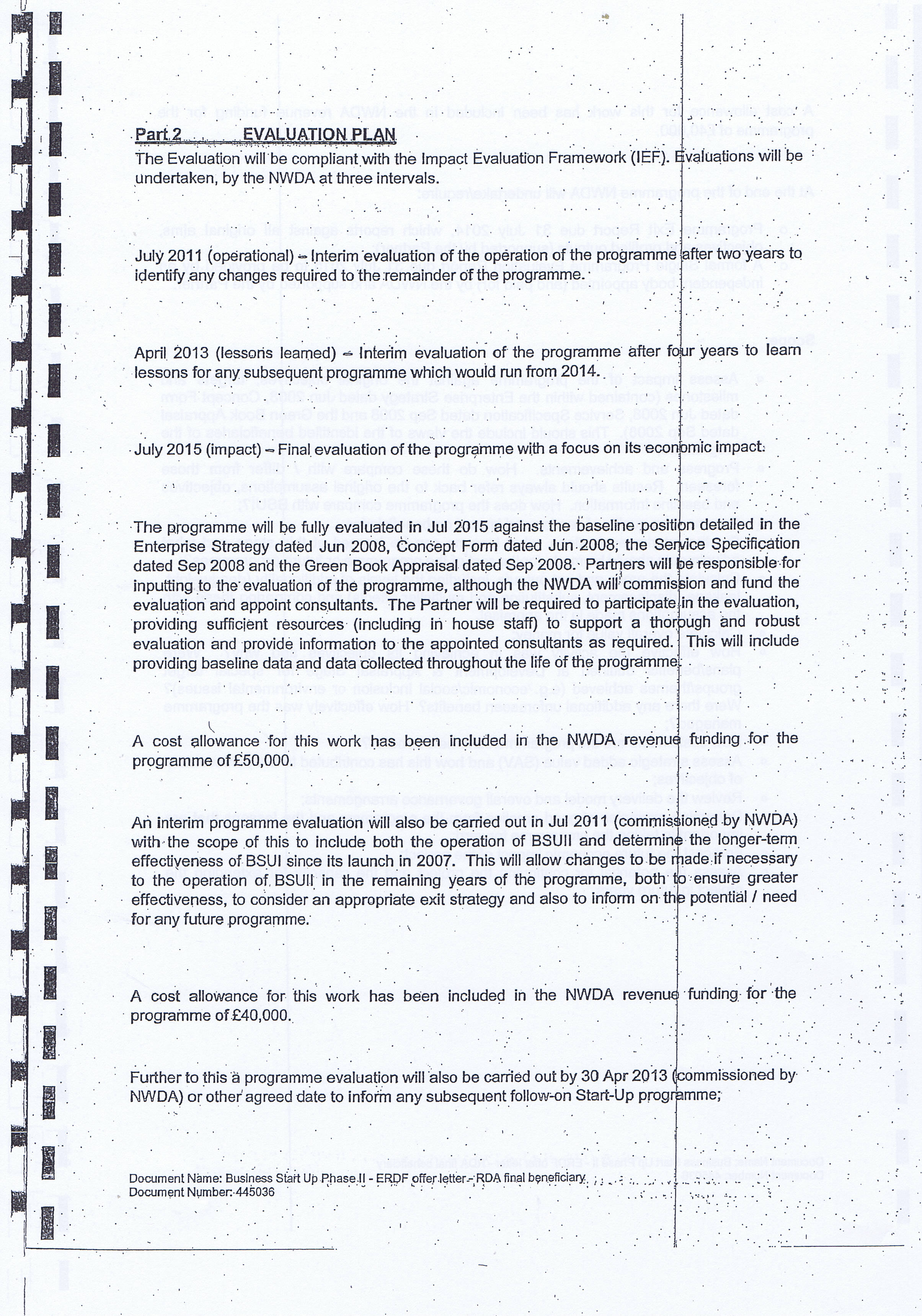

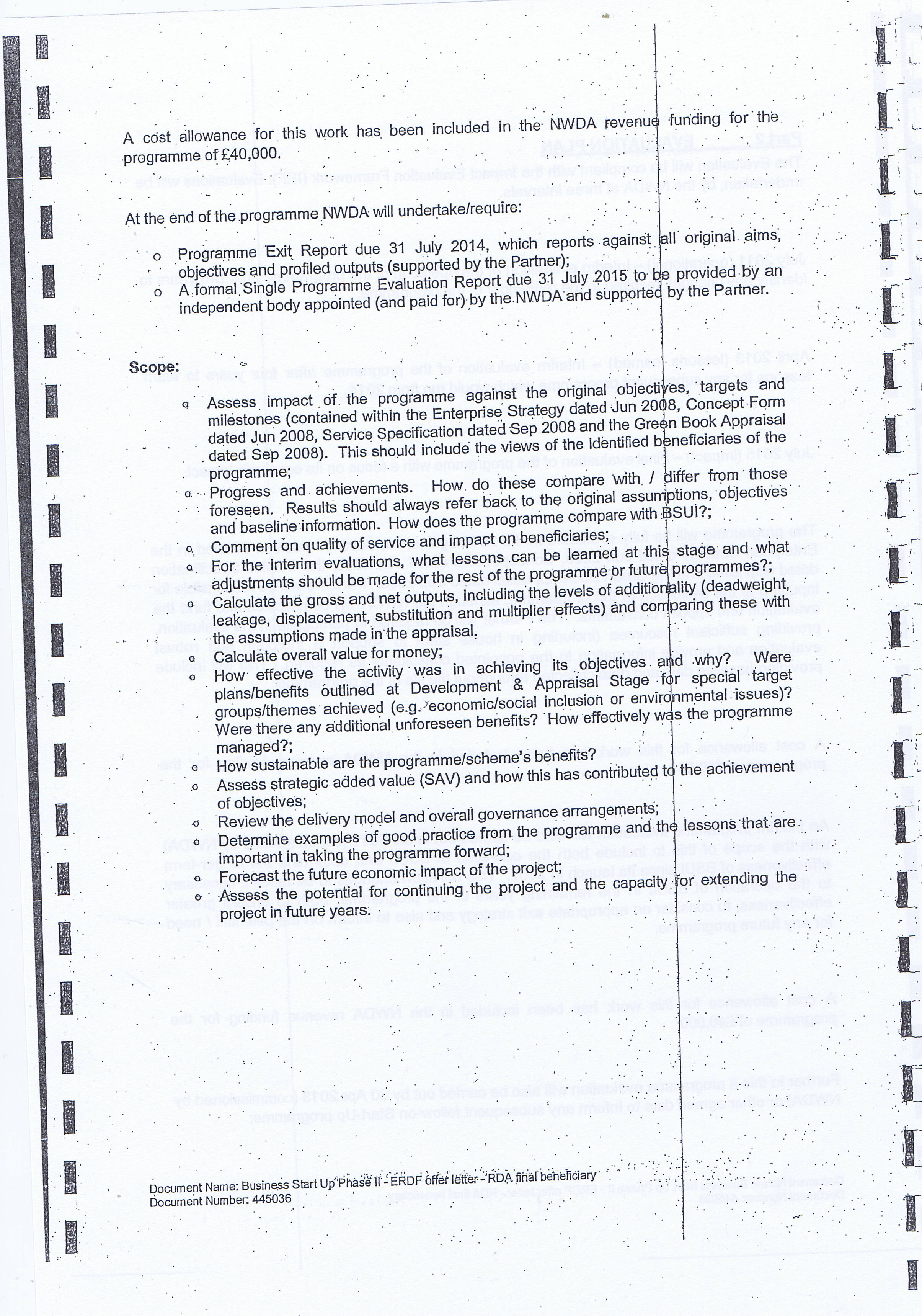

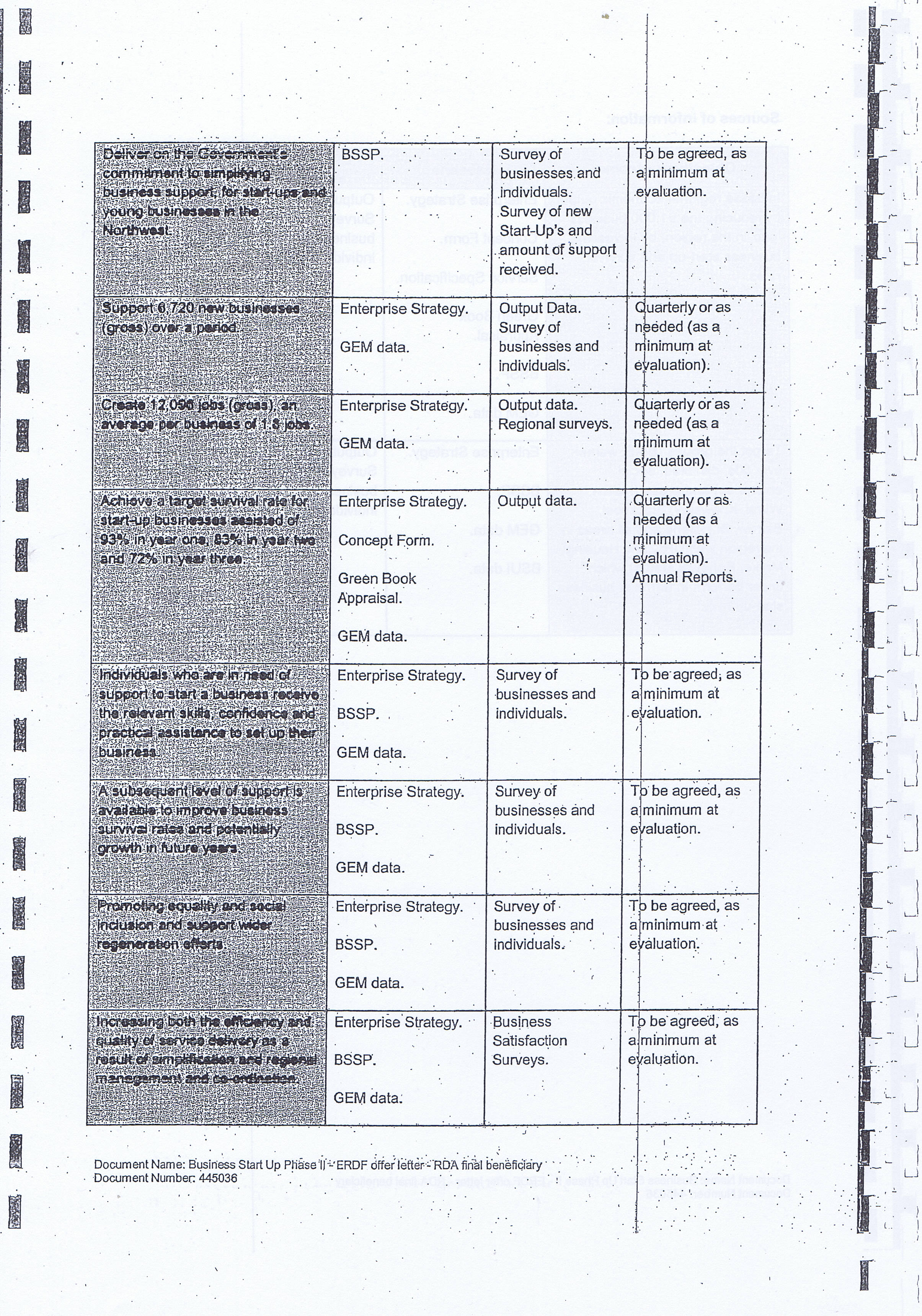

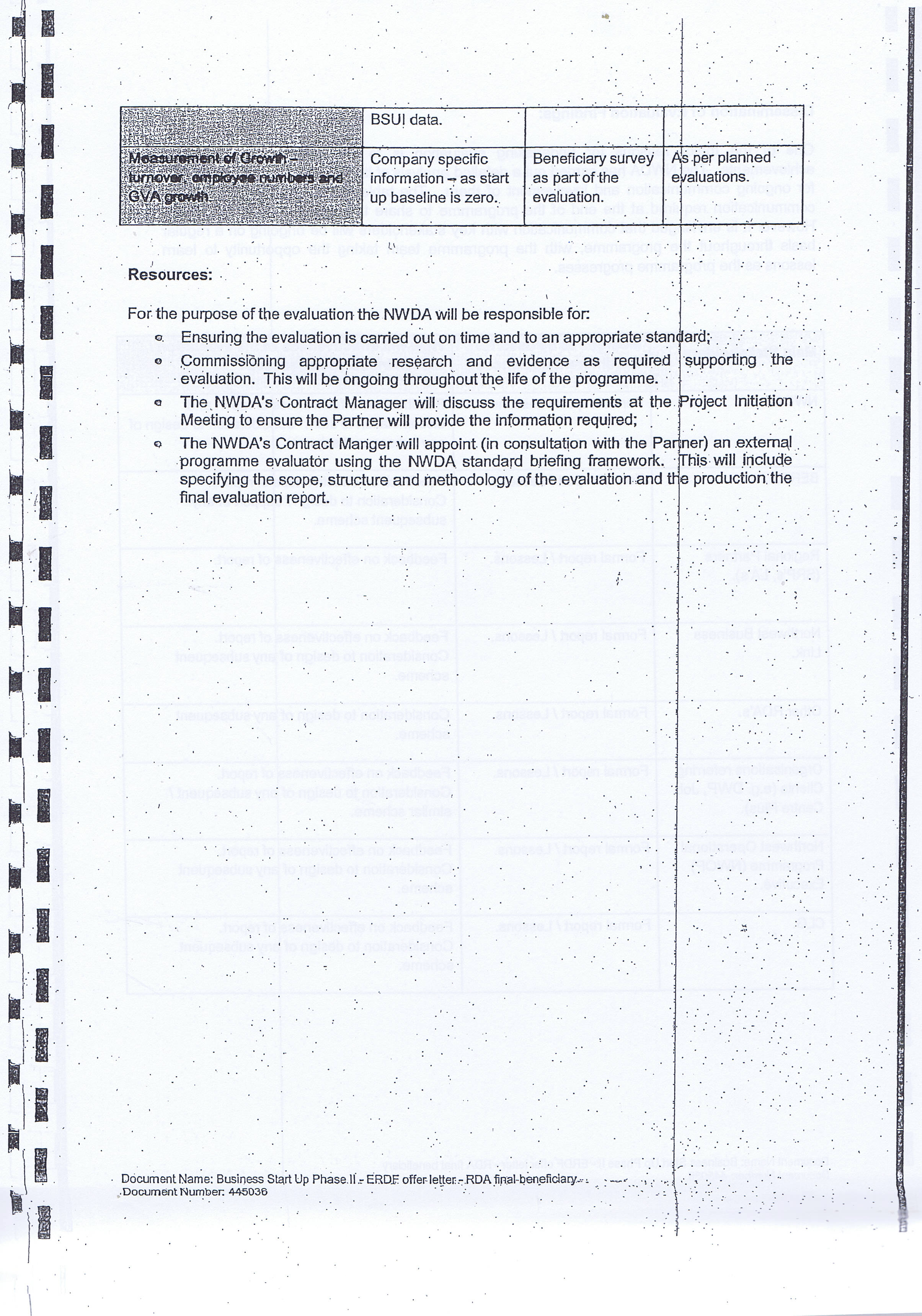

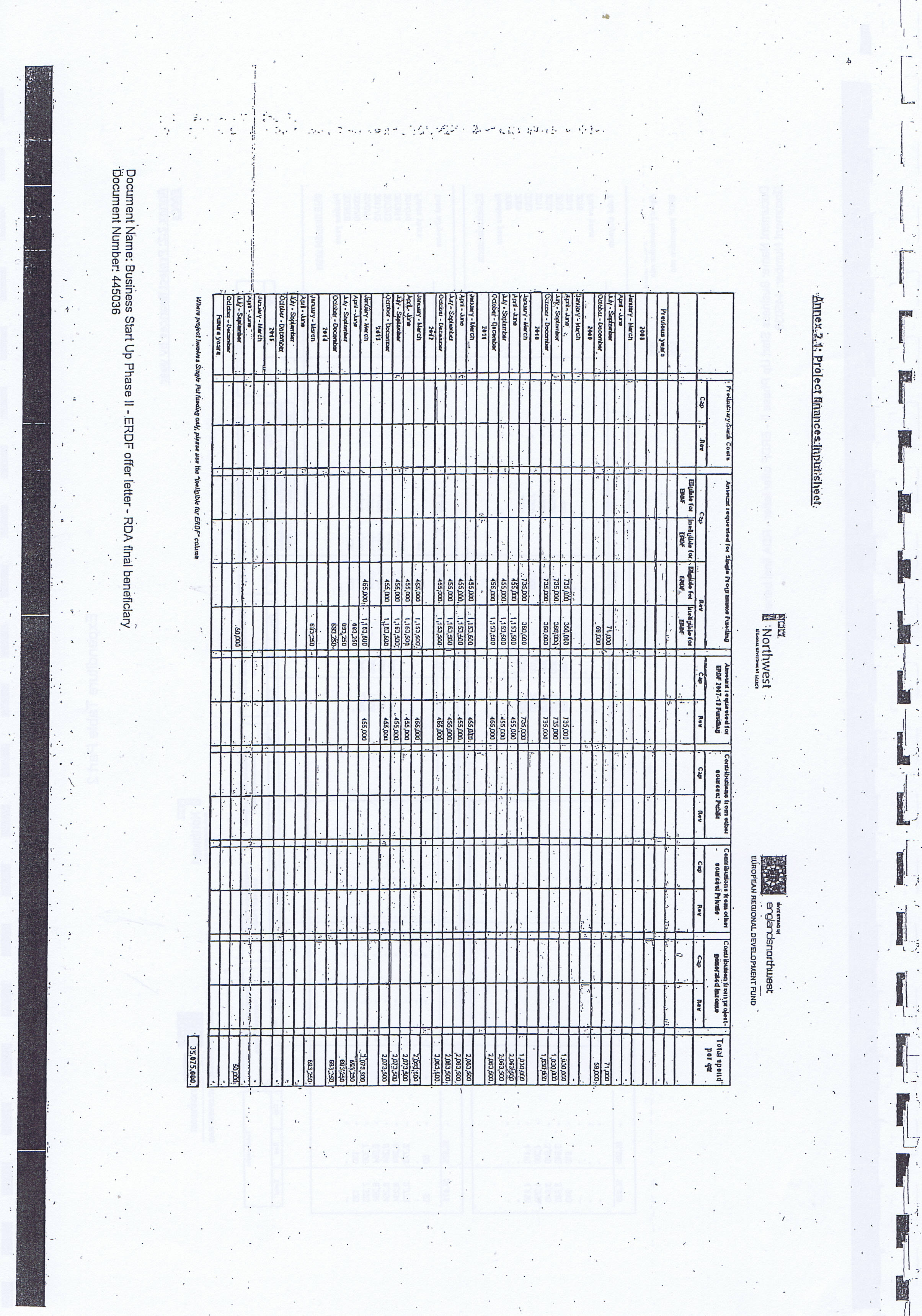

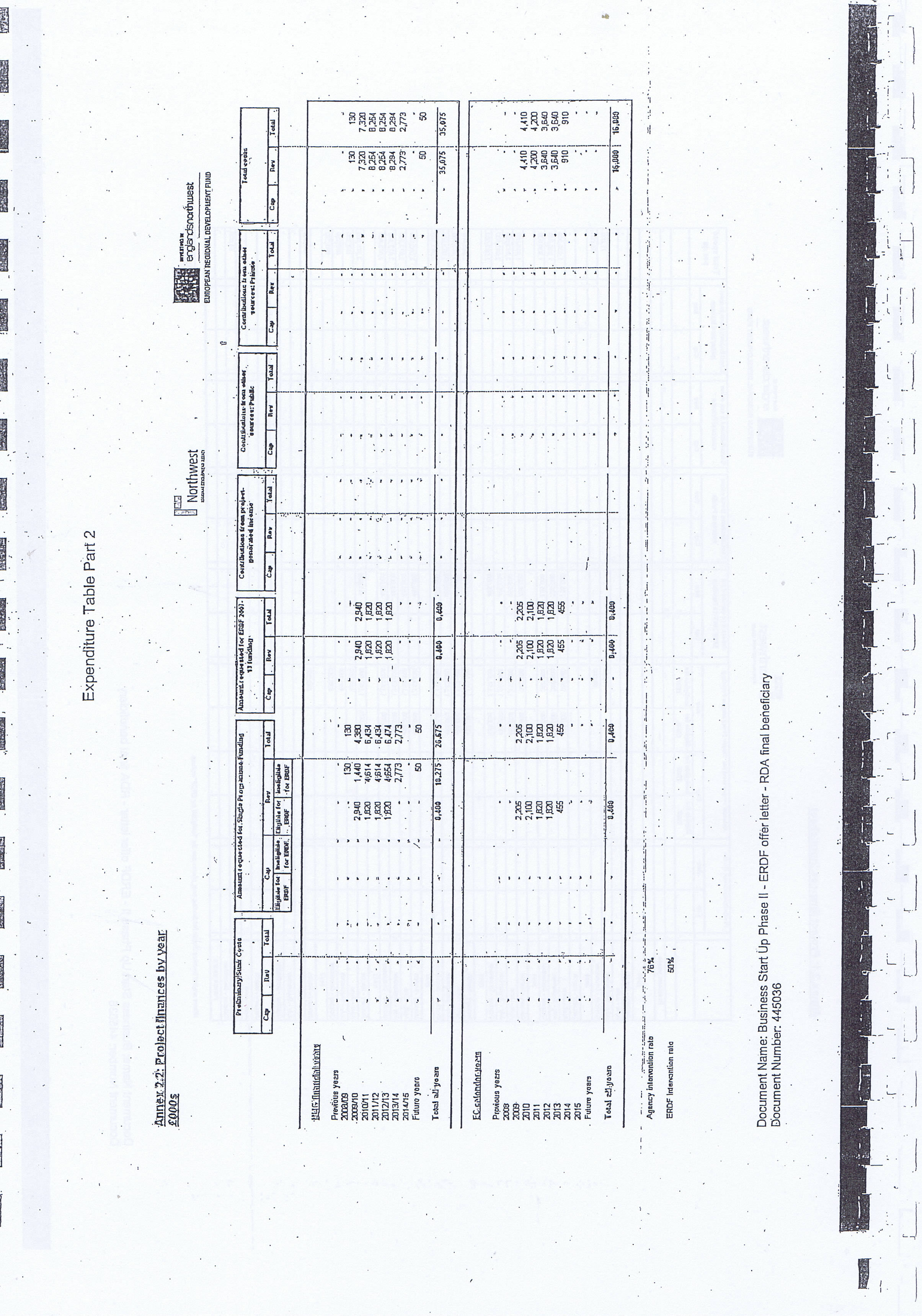

EXCLUSIVE: 90 Pages of North West Regional Development Agency’s Contract With Wirral Council for Business Grants Program

The astute among you will no doubt be aware that the North West Regional Development Agency was abolished last year, however I would guess that in its absence that its functions under the contract are now done by the Department of Business, Innovation and Skills.

There is more to the contract than the first ninety pages, although the other pages can wait for another day. The contract between the North West Regional Development Agency and Wirral Council was for business grants and has been the subject of recent whistle blowing concerns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}