What’s happened on the 6th floor of Wirral Council’s Chamber of Secrets for it to sue for over £300,000?

What’s happened on the 6th floor of Wirral Council’s Chamber of Secrets for it to sue for over £300,000?

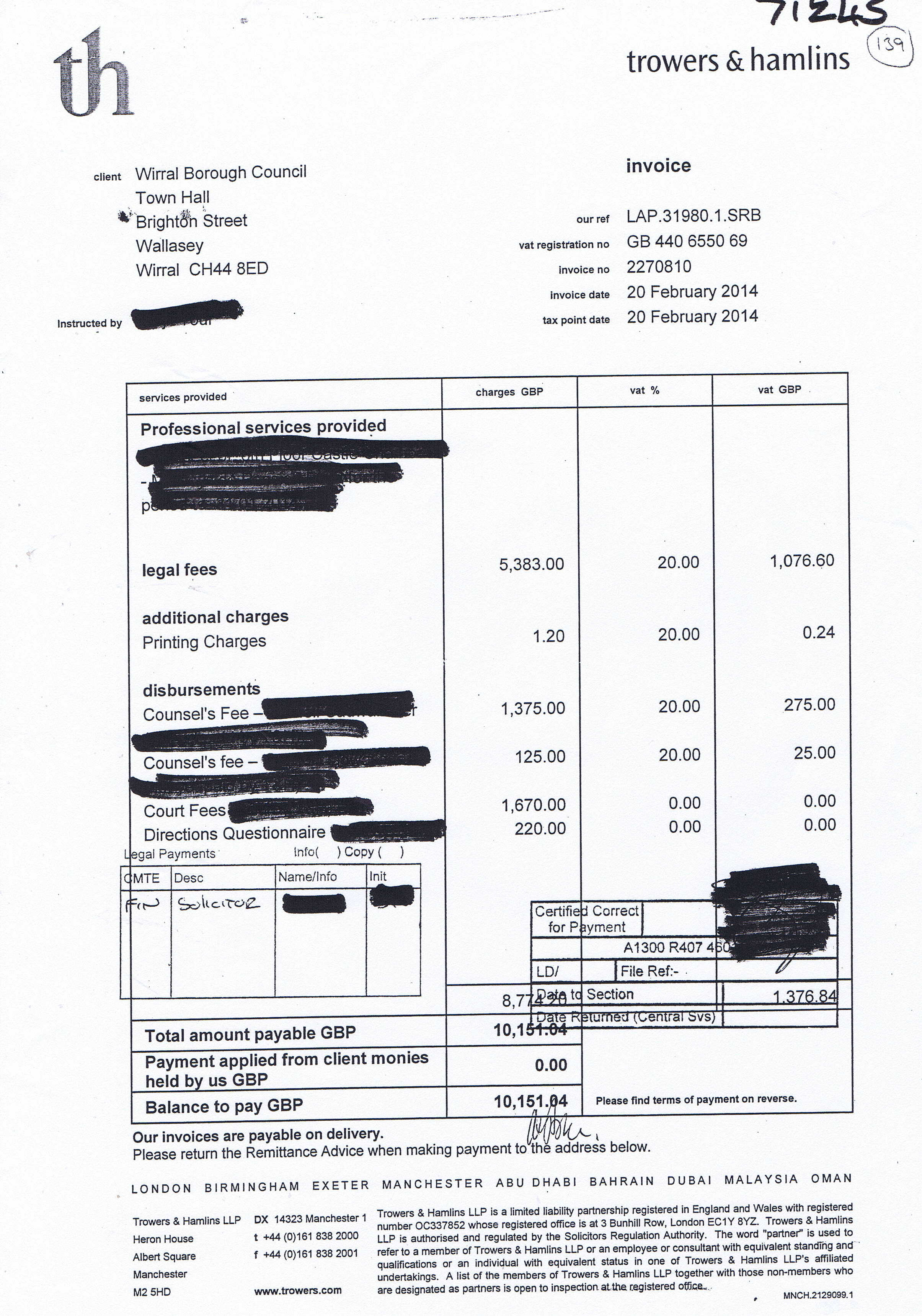

Last year I requested various legal invoices during the 2013/14 audit of Wirral Council. One of these is below:

Wirral Council invoice Trowers & Hamlins £10,151.04 20th February 2014

The invoice above is from Trowers & Hamlins and is for work connected to a court case to do with the 6th floor of Castle Chambers (a building owned and rented out by the Merseyside Pension Fund which is part of Wirral Council).

The court fee of £1,670 means this invoice is to do with to a civil court case in the High Court (in which Wirral Council is the claimant) to recover a sum of money where the amount exceeds £300,000 or an amount that is not limited.

What is blacked out under the heading Professional services provided appears to end in “6th floor Castle Chambers – Merseyside Pension Fund for the period to 31 01 2014”

So why all the secrecy surrounding the 6th floor at Castle Chambers? What was the outcome of the case and did the expenditure of £10,151.04 with Trowers & Hamlins lead to Wirral Council recovering any money?

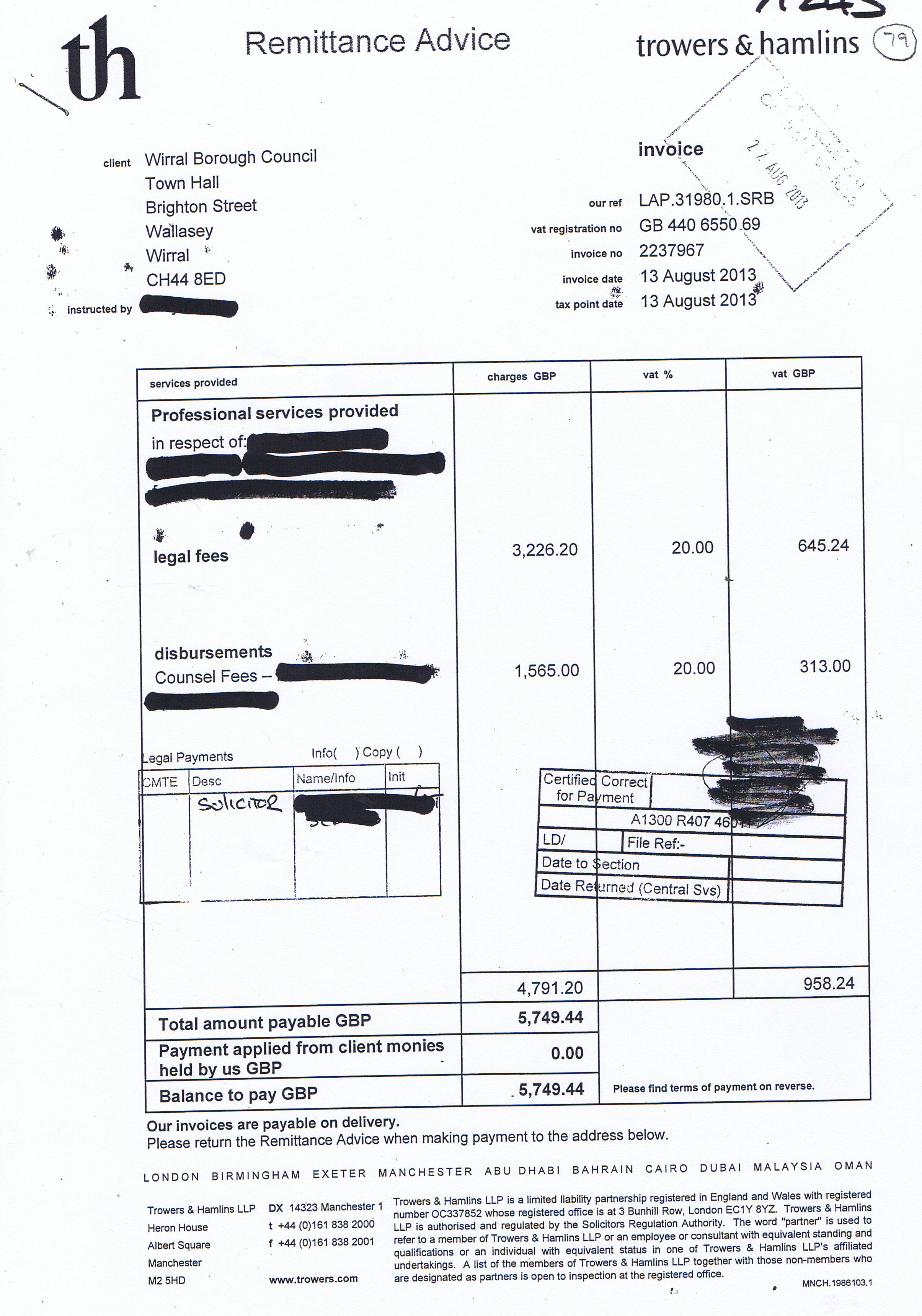

Below is an earlier invoice about the same matter for £5,749.44.

Wirral Council invoice Trowers and Hamlins £5,749.44 13th August 2013

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

What was my reply when Wirral Council’s “Ministry of Truth” asked for 2 invoices on this blog to be erased?

What was my reply when Wirral Council’s “Ministry of Truth” asked for 2 invoices on this blog to be erased?

Jenmaleo,

134 Boundary Road

Bidston

CH43 7PH

18th January 2015

by email to surjittour@wirral.gov.uk

CC: joeblott@wirral.gov.uk

Mr. Surjit Tour

Head of Legal and Member Services and Monitoring Officer

Department of Transformation and Resources

Wirral Metropolitan Borough Council

Town Hall

Brighton Street

Wallasey

Wirral

CH44 8ED

Dear Mr. Tour,

Thank you for your email of 15th January 2015 sent at 16:38 with the subject “Blog posting of invoices” which is attached for reference at appendix A. You also attached to your email ICO guidance to s.32 of the Data Protection Act 1998 titled “Social networking and online forums – when does the DPA apply?” which can be read on ICO’s website at https://ico.org.uk/media/for-organisations/documents/1600/social-networking-and-online-forums-dpa-guidance.pdf .

Please class this as a formal response to the issues you have raised in it. I have no problem with you sending a copy of this response to Dr Gareth Vincenti.

You state “You were provided with copies of certain invoices in compliance with Section 15 (a) of the 1998 Act, which entitles you to make copies of all or any part of the accounts and those other documents.”

The issue of copying of documents (as you can read for yourself in appendix B which is a copy of the legislation) is dealt with by the Audit Commission Act 1998 section 15(1)(b), as section 15(1)(a) deals with a right to inspect documents, not to copy documents. Therefore this sentence in your email should read Section 15(1)(b), not Section 15(a).

You go on to state “In redacting certain parts of those invoices, the Council relied on Section 15 (3A) of the Audit Commission Act 1998, as amended, which relates to personal information.”

If you read s.15(3A) of the Audit Commission Act 1998, as amended (attached as appendix B) you will find the definition of personal information in s.3A is “(3A) Information is personal information if–

(a) it identifies a particular individual or enables a particular individual to be identified; and

(b) the auditor considers that it should not be inspected or disclosed.”

It is important to note that the way the legislation is phrased it is not down to Wirral Council to make the ultimate decision as to whether information that may or may not fall within the definition of personal information as defined by section 3A should or shouldn’t be inspected or disclosed, but that decision is to be made by Wirral Council’s auditor who is for the financial year in question (2013-14) was Grant Thornton UK LLP.

It has not been determined yet whether Wirral Council asked its auditor Grant Thornton UK whether any of the information on the invoice in question should not be inspected or disclosed and if so what Grant Thornton UK LLP’s decision on this matter was.

Appendix C is a communication to Wirral Council’s external auditor in an attempt to clarify whether this took place.

On the 19th January 2015 I received a reply from Wirral Council audit Grant Thornton UK LLP. As you may or may not be aware the current engagement lead at Grant Thornton UK LLP is different to the engagement lead at Grant Thornton UK LLP for the 2013/14 audit. I can confirm that Grant Thornton UK LLP however are making enquiries and will respond as soon as they can.

If there has been an oversight and Wirral Council did not ask its external auditor to make a determination in relation to the many redactions it made to the hundreds of invoices I inspected and received copies of, I would hope that that arrangements could be made to inspect and copy the information I was incorrectly denied access to inspect and receive copies of last year.

You state later in your email:

“The Council considers that it may be necessary to report this matter to the Information Commissioner’s Office and Dr Vincenti may wish to take his own action in connection with your disclosing his personal data “

I will deal with the two interrelated matters raised here in relation to what you refer to as “personal data” of Dr Vincenti’s.

His surname “VINCENTI” is mentioned at the top of the invoice. Not redacted on the copy invoice supplied by Wirral Council is the phrase “Invoicing by Midex Pro for Dr Vincenti”. It is also stated that “cheques are to made payable to Dr. Vincenti”. Two addresses are also used on the invoice to send cheques to, one is a document exchange “DX 720874 Northallerton”, the sort code of 54-10-41 (which relates to a specific branch of a bank) is provided on the invoice for BACS payments and an email address of garethvincenti@btinternet.com is also given.

Dr Gareth Vincenti discloses his own email address, along with other contact details such as the address for correspondence on his website here [drvincenti.co.uk/contact.htm (at the time of writing this link worked however Dr Vincenti’s website is down as of 19th March 2015)]] . The document exchange address is published here http://www.expertsearch.co.uk/cgi-bin/find_expert?4052 and also elsewhere online.

Neither the sort code, nor the document exchange reference fall under s.3A as neither identify a particular individual or enable a particular individual to be identified as both would be used by multiple individuals.

34 Information available to the public by or under enactment.

Personal data are exempt from—

(a) the subject information provisions,

(b) the fourth data protection principle and section 14(1) to (3), and

(c) the non-disclosure provisions, if the data consist of information which the data controller is obliged by or under any enactment other than an enactment contained in the Freedom of Information Act 2000 to make available to the public, whether by publishing it, by making it available for inspection, or otherwise and whether gratuitously or on payment of a fee.

As to the invoice in question, the “personal data” of Dr Vincenti as you put it was available for inspection because of s.15 of the Audit Commission Act 1998, therefore s.34(c) of the Data Protection Act 1998 applies. It has not been established whether the auditor made a determination that any of it fell within the meaning of “personal information” in section 3A. Therefore at this stage, as you have not provided any evidence that the auditor made such a determination it means such “personal data” is exempt from the non-disclosure provisions that you refer to in your email.

You also state in your email that “which additions include the address of an employee/or former employee of the Council which is capable of amounting to personal data and in the context of the invoice capable of amounting to the processing of sensitive personal data.”

The address you refer to was a partial address. Had it been a complete address including house number, it could be argued that it would fall under the definition of personal information (as defined by s.15(4) of the Audit Commission Act 1998 see appendix B) which states that in order to qualify as personal information, the information “relates specifically to a particular individual”.

There are 60 different addresses in Forwood Road and 22 addresses that match that particular postcode. Wirral has a average household population of 2.17 per a household. Therefore the partial address could potentially relate to one of an estimated 48 individuals.

A partial address, without a house number does not therefore “relate specifically to a particular individual” nor does it enable a particular individual who may live at one of these addresses to be identified. It relates to a large group of individuals. Therefore it falls outside the definition of “personal information” as defined by s.4(1)(a) as it is not information that relates specifically to a particular individual.

Section 32 of the Data Protection Act 1998 on journalism, literature and art also applies here. I state my belief as data controller that I believe that having regard in particular to the special importance of the public interest in freedom of expression, publication of both the original invoice, a copy of the invoice with some of the text from the original invoice highlighted in green and this response including appendices to the response is in the public interest.

Finally you state “I do not consider that your right to inspect and the right to have copies made of relevant documents, then entitles you to disclose such documents to the public”.

I hope I have outlined (in much detail above) as to why you are incorrect in that assertion. This issue of the purposes to which information obtained by third parties using their rights to inspect and have copies of information held by local councils during the audit has already been dealt with at a previous judicial review case.

I refer you to R (HTV Ltd) v Bristol City Council [2004] 1 WLR 2717 which I have recently read. I quote from Elias J, the High Court Judge in that matter:

“55. The premise here is that the provision requires the information to be used for a limited purpose or purposes. As I have indicated, I accept that Parliament probably did envisage that the information would be primarily in order to enable electors to raise questions with the auditor and ultimately raise objections. But the fact that those who have access to this information extend beyond those who can make such a request, or raise such an objection, shows that it cannot be the only purpose.

56. In any event, there is no express limitation in the statute as to the use to which this information can be put. I see significant practical difficulties as to confining the use of the material once it has been acquired.”

Finally, my last two points are as Wirral Council is the data controller for the complaint made to it by Dr Gareth Vincenti which refers to me, please class this response as a request exercising my right under s.7 of the Data Protection Act 1998 for a copy of Dr Gareth Vincenti’s complaint.

I further point out that due to what is referred to above I am exercising my right under s.10 of the Data Protection Act 1998 and request that Wirral Council confirm it will immediately cease to process further any personal data about myself in relation to the complaint made by Dr Gareth Vincenti or your email for the reasons outlined above as raising this issue in the way it has been is causing distress.

Yours sincerely,

John Brace

Appendix A (email from Surjit Tour to John Brace dated 15th January 2015)

from:

Tour, Surjit <surjittour@wirral.gov.uk>

to:

john.brace@gmail.com

date:

15 January 2015 at 16:38

subject:

Blog Posting of Invoices

mailed-by:

wirral.gov.uk

Dear Mr Brace,

I refer to your inspection of documents under Section 15 of the Audit Commission Act 1998, in connection with the audit of the Council’s accounts for the financial year ending March 2014. You were provided with copies of certain invoices in compliance with Section 15 (a) of the 1998 Act, which entitles you to make copies of all or any part of the accounts and those other documents. In redacting certain parts of those invoices, the Council relied on Section 15 (3A) of the Audit Commission Act 1998, as amended, which relates to personal information.

I do not consider that your right to inspect and the right to have copies made of relevant documents, then entitles you to disclose such documents to the public nor does it entitle you to alter the Council’s redacted documents, which alteration constitutes processing of data. The Council has received a complaint from Dr Gareth Vincenti concerning a posting made on your blog on 1 December 2014 entitled:

“Do you want to know what 6 redacted legal invoices paid by Wirral Council on employment matters (including one from a consultant psychiatrist) state?

This posting included the copy of an invoice from Dr Vincenti which had been redacted by the Council. You had posted a second copy of the invoice, having altered part of the redactions to include information in green. You state on the blog posting:

“I’ve supplied both the original and a partly redacted copy of this as the original is heavily redacted. My additions are in green”.

I have had regard to the guidance of the Information Commissioner’s Office,“Social networking and online forums – when does the DPA apply?”

I consider that by altering the Council’s redactions to include additions in green, you have potentially processed personal data in breach of the Data Protection Act 1998, which additions include the address of an employee/or former employee of the Council which is capable of amounting to personal data and in the context of the invoice capable of amounting to the processing of sensitive personal data. I do not believe that you are entitled to rely on the exemption contained in section 36 of the Data Protection Act 1998, in that I consider you are using social media for non-domestic purposes. Section 36 contains an exemption for personal data that is processed by an individual for the purposes of their personal, family or household affairs. I am therefore requesting that you remove from your blog both copies of the invoice from Dr Vincenti immediately.

The Council considers that it may be necessary to report this matter to the Information Commissioner’s Office and Dr Vincenti may wish to take his own action in connection with your disclosing his personal data and the address referred to above.

Appendix B

Section 15 of the Audit Commission Act 1998 (as amended by s.160 of the Local Government and Public Involvement in Health Act 2007)

15 Inspection of documents and questions at audit

(1)At each audit under this Act, other than an audit of accounts of a health service body, any persons interested may—

(a)inspect the accounts to be audited and all books, deeds, contracts, bills, vouchers and receipts relating to them, and

(b)make copies of all or any part of the accounts and those other documents.

(2)At the request of a local government elector for any area to which the accounts relate, the auditor shall give the elector, or any representative of his, an opportunity to question the auditor about the accounts.

(3)Nothing in this section entitles a person—

(a)to inspect so much of any accounts or other document as contains personal information within the meaning of subsection (3A) or (4); or

(b)to require any such information to be disclosed in answer to any question.

(3A) Information is personal information if–

(a) it identifies a particular individual or enables a particular individual to be identified; and

(b) the auditor considers that it should not be inspected or disclosed.

(4) Information is personal information if it is information about a member of the staff of the body whose accounts are being audited which relates specifically to a particular individual and is available to the body for reasons connected with the fact—

(a)that that individual holds or has held an office or employment under that body; or

(b)that payments or other benefits in respect of an office or employment under any other person are or have been made or provided to that individual by that body.

(5)For the purposes of subsection (4)(b), payments made or benefits provided to an individual in respect of an office or employment include any payment made or benefit provided to him in respect of his ceasing to hold the office or employment.

Appendix C – Email to external auditor Grant Thornton

query about whether Grant Thornton gave permission to Wirral Council during the 2013/14 audit for personal information on invoices should not be inspected/disclosed

Dear Robin Baker & Chris Whittingham,

During the 2013/14 audit I exercised my inspection rights to inspectvarious invoices and receive copies of them for the 2013/14 financialyear under s.15 of the Audit Commission Act 1998.

Last Thursday I received an email from Wirral Council that stated “Inredacting certain parts of those invoices, the Council relied onSection 15 (3A) of the Audit Commission Act 1998, as amended, whichrelates to personal information.”

S.15 (3A) of the Audit Commission Act 1998 was amended in 2008 to state:

“(3A)Information is personal information if—

(a) it identifies a particular individual or enables a particularindividual to be identified; and

(b) the auditor considers that it should not be inspected or disclosed.”

Could you confirm that as Wirral Council’s auditor at the time whethera determination was made by the auditor that personal information onan invoice for £3,060 from a Dr Gareth Vincenti dated 31st December 2013 was made and if so which elements on the invoice the auditorconsidered should not be inspected or disclosed?

Could you also confirm as Wirral Council’s auditor at the time whetherany determination was made by the auditor about personal informationon any of the invoices I requested for the 2013/14 year was made and if so the particular invoices and particular information that theauditor considered should not be inspected or disclosed?

If the auditor was not asked to make any such a determination couldyou state this too?

Thanks,

John Brace

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

Councillors recommend that they chose who will receive £thousands for sitting on new Pensions Board

Councillors recommend that they chose who will receive £thousands for sitting on new Pensions Board

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

Above is video of the Pensions Committee meeting of 19th January 2015.

Pensions Committee Wirral Council Merseyside Pension Fund 19th January 2015 L to R Pat Phillips Cllr Geoffrey Watt Cllr Mike Hornby Cllr Chris Carubia Cllr Nick Crofts Cllr Harry Smith

I’ll start this piece by declaring an interest as my father is paid a pension by the Merseyside Pension Fund administered by Wirral Council.

Wirral Council’s Pensions Committee (which form part of the governance arrangements for the Merseyside Pension Fund worth billions of pounds) met yesterday evening. The agenda and reports for this meeting are on Wirral Council’s website.

The original recommendation in the report had been “That Members consider the proposals for the Wirral Pension Board set out in this report and the draft Terms of Reference and advise officers of any required amendments before submission for approval and implementation by Wirral Council.”

The Chair of the new Pensions Board will receive £2,751 a year (plus travel & subsistence expenses) and the employer/employee representatives will receive £1375.50 a year (plus travel & subsistence expenses). Just before the meeting started a much more detailed recommendation was handed out. This was agreed at the meeting and is now a recommendation to a future meeting of all Wirral Council councillors. One of the implications of the revised recommendation is that three councillors (who are not on the Pension Committee) will form a selection panel to choose who is on the new Pensions Board.

The complete revised recommendation is below:

“1. Pensions Committee agrees and recommends to Council:

a) the establishment of a Pension Board pursuant to regulations (The Local Government Pension Scheme (Amendment) Regulations 2014) in accordance with the Terms of Reference set out in appendix 1, subject to the membership being agreed by Council and the Terms of Reference being amended to confirm that the board shall be quorate providing a minimum of 4 members are present.

b) that the Pension Board shall have the authority to do anything which is calculated to facilitate, or is conducive or incidental to, the discharge of any of its functions.

c) the establishment of a selection panel by the Council in accordance with appendix 3 to consider and assess applications received and undertake interviews. The selection panel is to make recommendations to Council with regard to appointments to the Board.

d) that the Head of Pension Fund be authorised to implement the administrative arrangements required to undertake a recruitment exercise necessary for the selection and appointment of members to the Board.

e) that the definition of independent member for the purposes of the Board shall be agreed as:

not a current elected member or employee of a participating scheme employer

has not been an elected member or employee of a participating scheme employer in the past 5 years

f) that in respect of the two active member representatives, the initial appointment to the Board for one of the representatives shall be for a term of 6 years and the other for 4 years; that in respect of the two representatives of local authorities, police/fire/transport authorities and parish councils, the initial appointment to the Board for one of the representatives shall be for a term of 6 years and the other for 4 years.

g) that the Pensions Committee (and the Heads of the Pension Fund and of Legal and Member Services after consultation with the Chair of the Pensions Committee prior to the meeting of the Council in March 2015) may recommend to Council changes to the Board and its Terms of Reference having regard to the final form of regulations and statutory guidance.

2. that the Selection Panel’s Terms of Reference as set out in Appendix 3 shall be that:

it shall comprise 3 elected members

it shall not consist of current Pensions Committee members

There shall be two advisors to the selection panel: the Head of Pension Fund and a representative from the Fund’s external auditors.

3. That the following amendments be made to the Board’s terms of reference set out in appendix 1.

a) Section 3 “Members of the Board shall cease to be a member of the Board if they do not attend two consecutive meetings and fail to tender apologies which are accepted by the Board” be substituted for “Other than by ceasing to be eligible as set out above, a Board member may only be removed from office during a term of appointment by the majority agreement of all of the other members. The removal of the independent member requires the consent of the Scheme Manager”.

b) Section 3 the following shall be added: “In the event of the independent member not being available for a Board meeting, a Vice Chair for that meeting shall be determined by the Board members”.

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

4 Labour councillors agree salary for new Wirral Council Chief Executive at between £155,000 and £175,000

4 Labour councillors agree salary for new Wirral Council Chief Executive at between £155,000 and £175,000

Employment and Appointments Panel (Chief Executive) Committee Room 3, Wallasey Town Hall, 24th November 2014 L to R Martin Denny (LGA), David Slatter (Penna PLC), Cllr Jeff Green (Conservative), Cllr Lesley Rennie (Conservative) and Cllr Phil Gilchrist (Lib Dem)

Employment and Appointments Panel (Chief Executive) Committee Room 3, Wallasey Town Hall, 24th November 2014 L to R Martin Denny (LGA), David Slatter (Penna PLC), Cllr Jeff Green (Conservative councillor), Cllr Lesley Rennie (Conservative councillor) and Cllr Phil Gilchrist (Lib Dem councillor)

Please accept YouTube cookies to play this video. By accepting you will be accessing content from YouTube, a service provided by an external third party.

If you accept this notice, your choice will be saved and the page will refresh.

Video above is from the Employment and Appointments Panel (Chief Executive) public meeting held on the 24th November 2014 in Committee Room 3, Wallasey Town Hall, Seacombe . This write-up of the public meeting starts at 23:09 in the video above.

Wirral Council’s Employment and Appointments Panel (Chief Executive) met in Committee Room 3, Wallasey Town Hall, Seacombe on Monday afternoon at around 2.30pm. The councillors on the Employment and Appointments Panel (Chief Executive) which had previously been decided by the Employment and Appointments Committee on the 27th October 2014 are:

Cllr Phil Davies (Labour) Chair Cllr Ann McLachlan (Labour) Cllr George Davies (Labour) Cllr Adrian Jones (Labour) Cllr Jeff Green (Conservative) Cllr Lesley Rennie (Conservative) Cllr Phil Gilchrist (Lib Dem)

Cllr Adrian Jones said, “Yes Chair, I just want to make a number of comments on this and I do appreciate Jeff Green that you obviously want to make a big issue about this. I just want to understand and … , but the comments on the existing Chief Executive were way off the mark. He came here as a temp, he stayed a bit longer…. he now wants to retire and do whatever it is that retired chief executives do.

He oversaw transformation of what’s been described as a failed Council, I think it was still a failing Council in 2012 when he took over and he’s transformed that into a 1st class machine which is recognised elsewhere, simply by the National… as being a completely different and efficient Council from the failing one he inherited from you and from your predecessors including us Labour Parties.

Now I think that if we were to argue the price we aren’t going to get that again. That was a very lucky situation … but if Jeffrey [Green] was saying that he passed some moral indignation and objection to extremely high salaries.. then I would be the first to agree with him but this is the pond that we’re swimming in and we’ve got no other way to approach this other than to pay the going rate, if we want to get the best and it really doesn’t boil down to much other than that. I would have thought incidentally, it’s quite a good Conservative principle when you see it put like that.”

Cllr Jeff Green said that saving taxpayers’ money was his primary concern in principle.

Cllr Adrian Jones said he agreed with Cllr Jeff Green and then said something else to which Cllr Jeff Green responded.

Cllr Phil Davies asked if there were any other contributions and that he wished to move an amendment.

Cllr Phil Gilchrist said, “Still resting underneath the present Chief Executive there’s a whole raft and that’s another phrase as well, a series of strategic directors in post. Now they recruit and manage a slimmed down organisation and I’m not convinced everything’s beautiful in the garden and I’ve heard what Adrian [Jones] says and I haven’t got problems with the rest of it, but once the Administration attempts to bring in Superman in order to sort out the existing problems, but unfortunately you know we can’t even get anyone with errm Superman’s qualities.”

Cllr Phil Davies said, “or Superwoman!”

Cllr Phil Gilchrist continued “or Superwoman! … something with some kryptonite. Well probably Ghostbusters would be far…”

Cllr Adrian Jones interrupted, “Is that a proposition?”

Cllr Phil Davies said, “You’ve gone from Superman to Ghostbusters!”.

Cllr Phil Gilchrist said, “Well, all I thought was that the big lake of stuff under the Town Hall made everyone so bad-tempered in the film. I think it would be over the top to go with £155,000.”

Cllr Adrian Jones responded to the point.

The Chair (Cllr Phil Davies) said that Cllr Jeff Green have moved something but that he was going to move the following resolution:

“Given that we the 9th largest metropolitan authority in the country and given that the current salary of our Chief Executive I don’t believe is sufficiently competitive with the market as exists at the moment and given the external advice we’ve had from the Local Government Association and Penna, I’m going to recommend that the salary range for the Chief Executive be agreed between £155,000 and £175,000 an annum and I think as part of that, the second element of that should be that the final, the final salary for the Chief Executive would be within that range and be agreed by this Panel as part of the recruitment process.”

He continued, “Could I just make the other comments that you’re abs.. you know.”

Cllr Jeff Green said, “Were you going to say I was right?”

Cllr Phil Davies replied, “You are right that we do need to make substantial savings as a result of your government’s austerity policies and the Chief Executive, whoever we recruit, one of his or her principal tasks will be to make the £70 million that we need to make over the two years and a lot more than that as we’re told that we’re told that the austerity is only halfway through beyond that.

So, I believe that we can get the good, the best outcome we can if he or she would more than pay for their salary ideally and I think if again, if you look at the authorities in Merseyside and Cheshire, this is, this is comparable with the salaries that they’re charging and we’re talking about authorities run by both the Conservative and Labour parties in terms of Cheshire West and Cheshire East. ”

He moved that, Cllr Ann McLachlan seconded it.

The Chair sought legal advice because there was an amendment. The legal adviser said that they would have to vote on the amendment first.

Cllr Jeff Green said, “Could I just make a couple of points? First of all we are comparing all these across the scale across the North-West as far I’m concerned there aren’t all vacancies there. So we’re not really competing with people to fill those posts.

Number two, I you know wonder whether given we are talking about as I say a million pounds over five years if we go along with the proposal you make, wouldn’t it be better to actually test the market? So instead, you know, you as the Leader of the Council, would it be the administration determining what the leader mark to be, because the first thing to do is to test the market. Again you know get three quotes to test it, so will we be actually be better off actually testing to see if the sort of candidates we might want are available at £130,000 and only then if someone can provide evidence that those candidates aren’t available, would we then seek to look at that situation?

That’s the way you’d normally, I think you would normally do it as opposed to make a whole series of assumptions that there won’t be people ever at that level, the level stops here and therefore bump it to what I think is an astronomical figure and I just have to say one that I think the public will find it difficult to understand given some of the measures that you as an administration are currently taking.”

Cllr Phil Davies disagreed, “Well I would errm, I would disagree with that as a way forward for the two reasons. One is we’ve had, we’ve got our experts who know the, who know the market for chief executives and senior officers and their advice is that our current salary would not get a high quality candidate because we are literally at either at the bottom or at the very lowest quartile.

So you know, we’ve had our external advisers who’ve given us that information given the current state of the market and secondly what you’re suggesting Jeff [Green] would build in a delay in the process if we had to jump through that particular hoop and I believe the priority now is to recruit the very best candidate we can, as soon as we can, after the current Chief Executive departs.

So I think for those two reasons I wouldn’t be in agreement with that as a way forward. So I think we’ve got an amendment which I will move, it’s been seconded by Ann [McLachlan], can I see all those in favour?”

For (4): Cllr Phil Davies, Cllr Ann McLachlan, Cllr George Davies, Cllr Adrian Jones

Against (3): Cllr Jeff Green, Cllr Lesley Rennie, Cllr Phil Gilchrist

The amendment (passed on a 4:3 vote) became the substantive motion.

The vote on the motion was:

For (4): Cllr Phil Davies, Cllr Ann McLachlan, Cllr George Davies, Cllr Adrian Jones

Against (3): Cllr Jeff Green, Cllr Lesley Rennie, Cllr Phil Gilchrist

The Chair Cllr Phil Davies said that it would be a recommendation to a meeting of Council on the 8th December [2014] and moved onto the job description and person specification.

Cllr Jeff Green asked how much extra the Chief Executive would get for being the Electoral Registration Officer on top of the £155,000 to £175,000 salary?

Chris Hyams said it was outlined in the appendices, appendix ten, she then changed this answer to appendix nine, page thirty-three.

Cllr Jeff Green asked what exactly was there? Chris Hyams said that the election fees are determined by which elections take place each year which are outlined in the appendix on page forty-three.

Cllr Jeff Green asked on top of that next year, with the assumption that they’re in post by May, there will be a further £12,605 on top of that and asked if it was one or if it got totalled up. So if it was Parliamentary you get £12,605, if it’s a local election as well you get £5,297.16. Would that be £17,800?

Chris Hyams replied that they are a combination of which elections there are. Cllr Jeff Green said that in May they’d get an extra £18k on top of £170,000 that they’d been talking about but normally as there are local elections the Chief Executive would get an additional minimum of £5,000 on top is that right?

Chris Hyams said that it was and that you could see from the appendices who actually sets that fee. Cllr Jeff Green said that he wasn’t saying that they were being particularly generous, just in terms of the overall package, it is £175,000 plus £12,000 plus £5,000.

Chris Hyams replied, “Yes it is.” and pointed out that the chief executive salaries provided were exclusive of Returning Officer fees.

Cllr Phil Davies said that in Cheshire West for example, their Chief Executive makes £180,000 plus they get this in addition. Chris Hyams confirmed this. Cllr Phil Davies asked if it was the same in every local authority to which Chris Hyams answered “yes”.

Cllr Jeff Green commented that it brought the remuneration to round about £200,000. Cllr Phil Davies said it was paid for by central government. Chris Hyams confirmed this.

Cllr Jeff Green asked if the £5,297.16 was paid for by central government? Chris Hyams confirmed this. Cllr Jeff Green said “Are we genuinely saying we can’t get anyone for less than £200,000?” and “I’ll tell you what, all that money I’ve paid to my trade union over the years, I wish they’d had this crowd in.”

The following recommendation was agreed:

(3) That the proposed process and timescales for appointment of a new Chief Executive (who shall also be appointed as the Head of Paid Service, Returning Officer and Electoral Registration Officer) as outlined in appendices two and eleven to the report, be approved.

Cllr Phil Davies moved the following:

(4) That this Panel recommends to Council at its meeting on 8th December 2014 that David Armstrong be appointed to the position of Acting Chief Executive and Head of Paid Service, with effect from 1 January 2015 until the newly appointed Chief Executive takes up the position and also David Armstrong becomes the Deputy Chief Executive from the 8th December to the 31st December 2014.

Cllr Jeff Green said, “I would be very supportive of that, I think David has done the job before so it’s good experience in those terms and I think as we know David is a first class officer that performs incredibly well in this role whatever he’s been asked to do so. What was the final bit?”

Cllr Phil Davies said, “Well, in case he needed err between the. Explain why we have to have a Deputy Chief Executive Chris?”

Chris Hyams replied, “OK”

Cllr Jeff Green asked if he got two salaries to which Chris Hyams replied “Not at all. The proposal around a recommendation from the 8th December is to ensure continuity. The Chief Executive leaves on the 31st December, that’s his last day, however he has outstanding leave. Should he not be in the Borough, there is a continuous Deputy that will be Acting Chief Executive from the 1st January. So there are differing management arrangements, it’s for continuity.”

Cllr Phil Gilchrist said, “I can’t think of anyone else, that’s what’s troubling me. I’m trying to think better than that. I am worried that there are enough problems in CYPD [Children and Young People’s Department] and Asset Management and everything else that needs tremendous amounts of attention. So I don’t know how safe it is to move David up to this position when there are all these little things that need tackling as well?”

The Chair, Cllr Phil Davies replied, “Well, look I mean errm, he’s got, he’s got sort of excellent err officers in asset management errm and I’m I’ve spoken obviously you will have expected me to have had a conversation with him … and he is confident that he’ll be able to play this role but still do his, still have the asset management working in good hands going forward. So I have had that conversation with him and he was confident that those arrangements would be put in place.”

Cllr Jeff Green said, “A reasonable plea to start … knowing the sort of person David is and I think this is kind of … Phil [Davies] as the new council, is to make sure that he doesn’t try to do too much.”

Cllr Phil Davies replied, “Absolutely.”

Cllr Jeff Green continued, “Because he’s the sort of guy that … going so you know just to help him focus”

Cllr Phil Davies replied, “Yeah.”

Cllr Jeff Green continued, “on the actual job.”

Cllr Phil Davies asked them to agree recommendation 4.

Cllr Phil Davies then moved recommendation 5:

” That this Panel recommends to Council at its meeting on 8 December 2014, the appointment of Surjit Tour as Returning Officer and Electoral Registration Officer and that Joe Blott is appointed as Deputy Returning Officer and Electoral Registration Officer, both effective from 1 January 2015 until the newly appointed Chief Executive takes up the position.”

This was agreed. There was no other business so the meeting closed. However a few weeks later in December 2014 the Wirral Green Party issued a press release on this which contained the line “How can Labour claim a commitment to fairness having just voting through an eye-watering 30% increase in the chief executive’s salary. Not only is this an insult to the council employees facing redundancy and reduced pay, it shows a leadership out of touch with reality and missing a glorious opportunity to set an example to others and rein in excessive pay in the public sector.”

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

Wirral Council spent £284,925.60 on 6 tractors, £168,474.83 on solar panels and £115,394.72 on Jack and the Beanstalk

Wirral Council spent £284,925 on 6 tractors, £168,474.83 on solar panels and £115,394.72 on Jack and the Beanstalk

As it’ll be Christmas Eve tomorrow, I thought at least one Christmas related invoice would be a good idea. So below is an invoice for £115,394.72 for a production of Jack and the Beanstalk at the Floral Pavilion. Wirral Council of course will have made something from sales of programmes and tickets.

In case there are those who don’t remember what the story of Jack and the Beanstalk is about, it’s a story about Jack taking the cow to market to be sold. He accepts magic beans in exchange for the cow, his mother is furious, throws the beans to the ground and sends Jack to bed. In the end Jack steals from the giant, kills the giant and he and his mother live happily ever after.

However here in the invoice:

Wirral Council invoice UK Productions Jack and the Beanstalk Floral Pavilion £115,934.72

And when the giant looks down from his castle in the sky, he might see some of Wirral Council’s new solar panels. Foz Contract Services Limited sent in an invoice earlier this year to Surjit Tour for £108,638.51. This is only part of the amount to be paid however, the grand total comes to £168,474.83.

On the bright side (geddit, bright side?) Wirral Council can claim back the VAT of £28,079.14. Here you go with that invoice:

Wirral Council invoice Foz Contract Services Limited 13th February 2014 Installation of PV Panels £108,638.51

And just to round it off, here’s a Wirral Council invoice for an order for 6 tractors from Turner Landscape (of a total of eight ordered). Each tractor cost £39,573 + VAT (total £47,487.60 each). However each tractor comes with an “instruction book”, radio, wheel & tyres, mirrors, an engine et cetera. The total for all six comes to £284,925.60 (including VAT) . Here are the invoices.

Wirral Council invoice Turner Landscape page 1 of 4 £284,925.60 6 tractorsWirral Council invoice Turner Landscape page 2 of 4 £284,925.60 6 tractorsWirral Council invoice Turner Landscape page 3 of 4 £284,925.60 6 tractorsWirral Council invoice Turner Landscape page 4 of 4 £284,925.60 6 tractors

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks: