What are the changes to citizen audit for 2015/16?

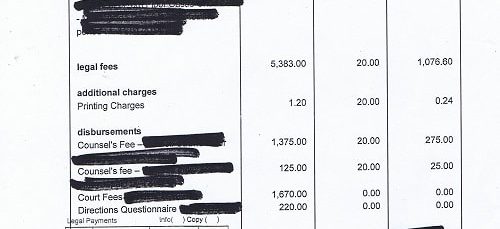

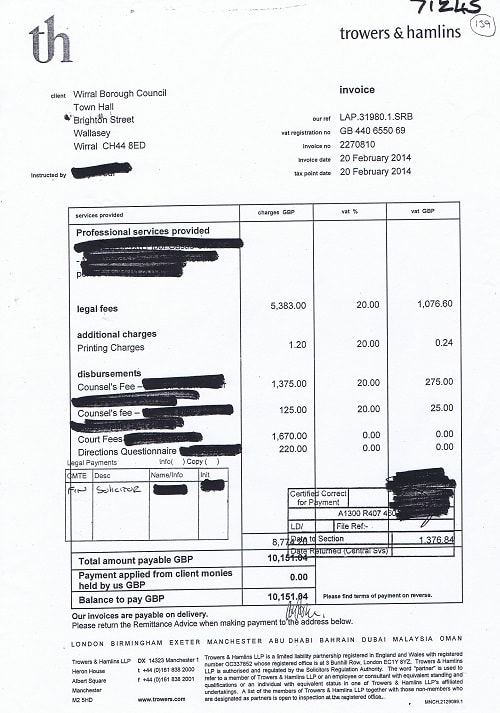

An example of an invoice supplied by Wirral Council during a previous audit

This year citizen audit changes. No longer are citizen audit rights covered by part II of the Audit Commission Act 1998 and the underlying regulations as this is no longer in force.

Previously during citizen audit, public bodies could redact information about the names of their own staff, but if it was information about anyone else they had to get their auditor’s approval.

Now, public bodies can redact parts of documents or whole documents on grounds of commercial confidentiality (although a public interest test has to be carried out) and information about the names of their own staff. They are also allowed to redact information that is the name of other individuals but not if it’s the name of a sole trader.

Previously the auditor had to consider all objections (as long as a copy was sent to the public body) made by local government electors for a declaration that an item of account is unlawful, recovery of an amount not accounted, a public interest report or an immediate report.

Now, an objection can only be about a matter that the auditor could write a public interest report about or declare that an item of account is unlawful but the auditor can decide not to consider the objection if:

(a) the auditor thinks it is frivolous or vexatious, or

(b) the cost to the auditor investigating is disproportionate to the sums involved or

(c) it repeats an objection already made and considered by the auditor whether in that financial year or a previous financial year.

However the auditor won’t be able to decide not to consider an objection if it is "an objection which the auditor thinks might disclose serious concerns about how the relevant authority is managed or led".

Even if the auditor rejects an objection for one or more of the reasons above the auditor can still make a recommendation to the public body.

Previously the Audit and Account Regulations 2011 required the inspection period was 20 working days regulation 9 and also that an advertisement was published (as well as a notice on its website) 14 days before this inspection period started regulation 10.

Under the new regime, this changes. There will be a longer inspection period of thirty working days, but this period will now also be the time during which objections and questions to the auditor must be made.

What’s in the 370 page whistleblowing report on Wirral Council’s grants to businesses?

What’s in the 370 page whistleblowing report on Wirral Council’s grants to businesses?

ICO Information Commissioner’s Office logo

The BIG/ISUS whistleblowing issues have been already covered in extensive detail by this blog over the past few years. However the latest twist in this story was yesterday’s release of a 370 page 2012 internal audit report into the matter following ICO decision notice FS50559883.

Wirral Council have finally released an internal audit report dated 13th January 2012 that went to Bill Norman (then Monitoring Officer/Director of Law, HR and Asset Management at Wirral Council). Those with long memories will remember that Bill Norman was suspended later that year over the Colas matter, then in September 2012 councillors agreed he should receive £146k plus £5k legal expenses to leave.

Back to the BIG/ISUS matters and let’s just quickly recap the blog posts I’ve written on the many aspects of this matter as they provide some background. I’m sure there are one or two I may have left out (I remember I republished some of my earlier blog posts which contained the agreements for BIG/ISUS in the lead up to the special meeting of the Audit and Risk Management Committee last October).

Million pound contract between Wirral Council and Enterprise Solutions (NW) Ltd for ISUS scheme was never signed (22/8/13) This blog post was about the contract between Wirral Council and Enterprise Solutions (NW) Ltd for the ISUS (Intensive Start Up Scheme) not having been signed. At the special meeting of the Audit and Risk Management Committee in October 2014 former Strategic Director for Regeneration and Environment Kevin Adderley did claim that a signed version had eventually been found and brought it to that meeting.

BIG/ISUS Reports: Wirral Council and Merseyside Police in “Alice in Wonderland” (4/10/13) Wirral Council and Merseyside Police respond to FOI requests for the reports for Grant Thornton’s (Wirral Council’s auditor) report into the ISUS matters. Wirral Council state they can’t release it because they’ve referred the matter to Merseyside Police, a Detective Chief Inspector for Merseyside Police states that "This matter is currently in the hands of Wirral Borough Council" and suggests that I make a FOI request to Wirral Council.

Or as I sum it up "Wirral Council won’t say anything because it’s in the hands of Merseyside Police, but Merseyside Police say it’s "currently in the hands of Wirral Borough Council".

So that’s a brief summary of developments so far? So what does the new information reveal? It’s a report by an auditor at Wirral Council which details the allegations the two whistleblowers made, the investigations into those allegations and the auditor’s opinion as to whether the whistleblowers were correct or not.

The executive summary runs from pages 9-16 and details the allegations made by the two whistleblowers and whether what was inspected during the investigation substantiated or refuted these claims. Pages 17-20 go through each of the allegations in detail as well as whether each allegation is correct or not and the implications that follow. Pages 21-45 are the main report which at the end contain 14 recommendations. Had some of these recommendations been implemented in 2012, some of the unanswered questions surrounding this matter would have been dealt with much earlier, such as the transfer of assets from Lockwood to Harbac.

At the special meeting of the Audit and Risk Management Committee in October 2014, councillors, officers and those speaking at the public meeting were warned not to refer to names of companies, yet the release of this 2012 audit report only removes the names of Wirral Council employees (and former employees). These matters are now out in the open (which should’ve happened before the Audit and Risk Management Committee met last year). Had this 2012 internal audit report been made available to councillors before that meeting the discussion may have been very different.

However it only came to light because of a FOI (Freedom of Information) request made by one of the whistleblowers and even then only after the Information Commissioner’s Office intervened with a decision notice. Certainly the whistleblowers must both feel vindicated by the conclusions reached in this detailed 2012 internal audit report.

The Liberal Democrat Group of councillors on Wirral Council plus the Green Party Councillor Pat Cleary have tabled the following Notice of Motion for the next Council meeting on the 12th October 2015 on the subject of FOI requests. It reads as follows:

OPEN GOVERNMENT ?

This Council recognises that the Information Commissioner’s Office, as the independent authority set up to uphold information rights in the public interest and to promote openness by public bodies, upheld 13 complaints against Wirral Council in the past year.

Of the 18 notices issued between 29 September 2014 and 24 August 2015, the majority (72%) of complaints were upheld.

Council believes that this is a matter for concern, requiring an explanation to its Members.

Council requests that lessons should be learned and applied from these decisions and questions whether Officers have been excessively cautious or defensive in their interpretation of the legislation.

Council, therefore, requests that the legislation is approached with greater regard to the ‘public interest test’ so that the risk of further reputational damage to Wirral can be reduced.

If you click on any of these buttons below, you’ll be doing me a favour by sharing this article with other people. Thanks:

Why did Wirral Council include Ian Coleman as a whistleblowing contact in the Passenger Transport Contract?

Why did Wirral Council include Ian Coleman as a whistleblowing contact in the Passenger Transport Contract?

Here is my first question to Wirral Council’s auditor (Grant Thornton) about the Passenger Transport Contract.

Wirral Council has a contract with Eye Cab Limited called the "Passenger Transport Contract". This contract started on the 1st September 2014 and runs to the 31st August 2015 and is for the provision of taxi services.

I requested to inspect a copy of the contract (see Audit Commission Act s.15(1)(a)) which was arranged for the 4th September 2015. As a local government elector for the Wirral area, I can question the auditor about the 2014/15 accounts from 9.30am on the 18th August 2015 until the accounts are closed (see Audit Commission Act 1998 s.15(2)).

Page 36 of the contract has a section titled "Section 5 CONFIDENTIAL COMPLAINTS PROCEDURE (Whistle-blowing) A Guide for Suppliers and Contractors (see attached page 36).

Passenger Transport Contract Wirral Council page 36 of 40

At the bottom of this page of the contract it details two people that a complaint under the whistleblowing procedure can be made to.

The second of these individuals is:

"Ian Coleman, Director of Finance, Wirral Borough Council, Finance Department, Treasury Building, Cleveland Street, Birkenhead, Merseyside, CH41 6BU"

Wirral Council’s Employment and Appointments Committee agreed early voluntary retirement for Ian Coleman on the 3rd October 2012 (see attached minutes).

Therefore as Ian Coleman was not an employee of Wirral Council at the time the Passenger Transport Contract was put out to tender (or when the contract was agreed) why was he included as a whistleblowing contact in the contract?

Yours sincerely,

John Brace

If you click on any of the buttons below, you’ll be doing me a favour by sharing this article with other people.